Estrategia de captura dinámica de volatilidad con RSI y Bandas de Bollinger

Resumen

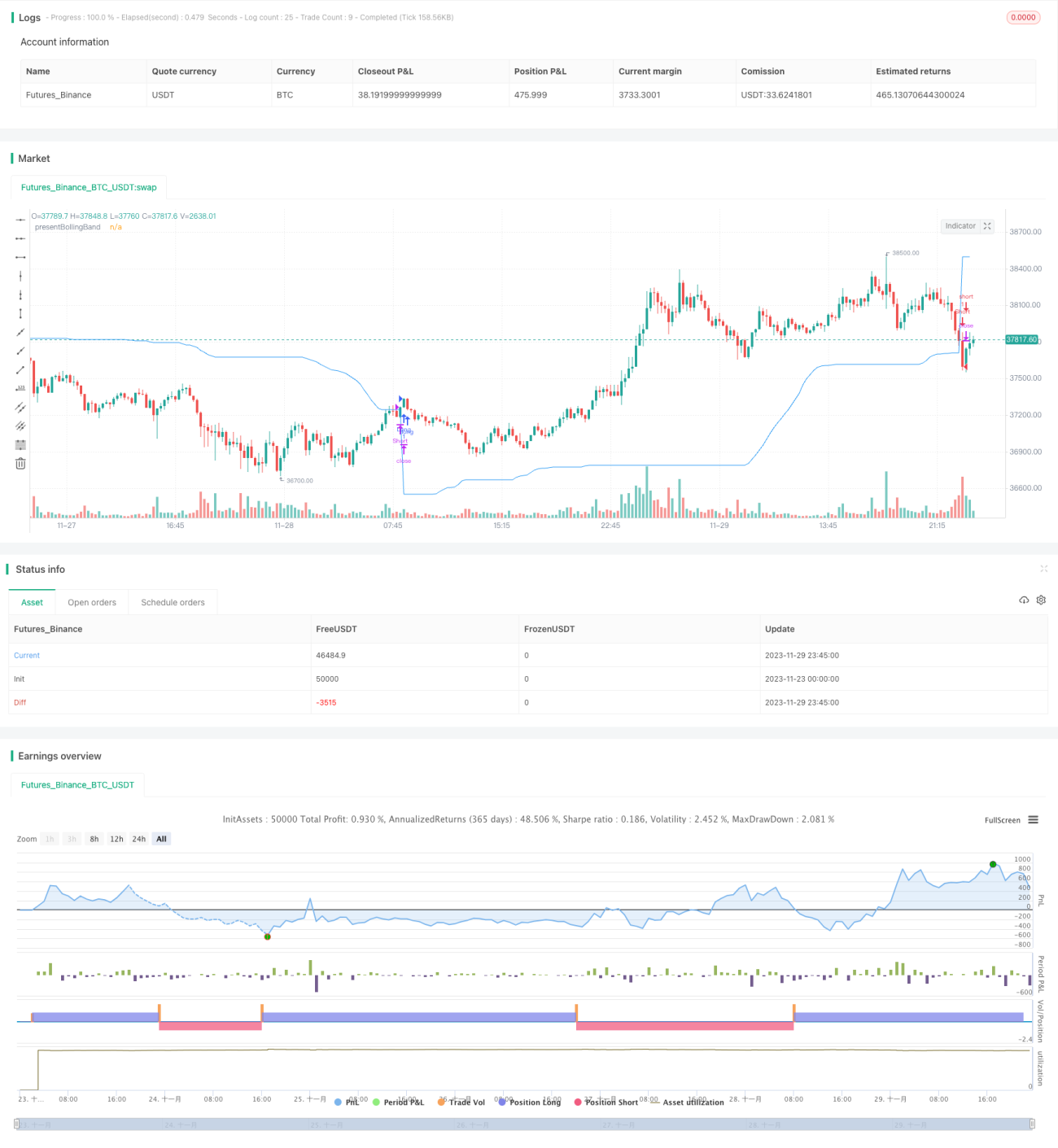

La estrategia de Captura Dinámica de Amplitud con RSI y Bandas de Bollinger es una estrategia de trading que integra los conceptos de Bandas de Bollinger (BB), Índice de Fuerza Relativa (RSI) y Media Móvil Simple (SMA). Su singularidad radica en que calcula un nivel dinámico entre las bandas superior e inferior en función del precio de cierre. Esta característica única permite que la estrategia se adapte a la volatilidad del mercado y a los movimientos de precios.

Los mercados de criptomonedas y acciones son altamente volátiles, lo que los hace ideales para aplicar estrategias con Bandas de Bollinger. El RSI ayuda a identificar condiciones de sobrecompra y sobreventa, comunes en estos mercados a menudo especulativos.

Principio de la Estrategia

Bandas de Bollinger Dinámicas: La estrategia primero calcula las bandas superior e inferior de Bollinger según una longitud y un multiplicador definidos por el usuario. Luego combina las Bandas de Bollinger y el precio de cierre para ajustar dinámicamente el valor de presentBollingBand. Finalmente, cuando el precio cruza la presentBollingBand hacia arriba, se genera una señal de compra; cuando cruza hacia abajo, se genera una señal de venta.

RSI: Si el usuario elige usar el RSI para generar señales, la estrategia también calcula el RSI y su SMA, y los utiliza para generar señales adicionales de compra y venta. Las señales basadas en el RSI solo se utilizan cuando la opción "Usar RSI para generar señales" está configurada como true.

Luego, la estrategia verifica la dirección de trading seleccionada y entra en posiciones largas o cortas según corresponda. Si la dirección de trading se establece como "Ambos sentidos", la estrategia puede abrir posiciones tanto largas como cortas.

Finalmente, cuando el precio de cierre cruza la presentBollingBand hacia abajo, se cierran las posiciones largas; cuando el precio de cierre cruza la presentBollingBand hacia arriba, se cierran las posiciones cortas.

Análisis de Ventajas

La estrategia combina las ventajas de las Bandas de Bollinger, el RSI y la SMA, lo que le permite adaptarse a la volatilidad del mercado, capturar dinámicamente las fluctuaciones y generar señales de trading en condiciones de sobrecompra y sobreventa.

El indicador RSI complementa las señales de las Bandas de Bollinger, evitando entradas erróneas en mercados laterales. Permite seleccionar solo operaciones largas, solo cortas o ambos sentidos, adaptándose a diferentes condiciones del mercado.

Los parámetros son personalizables, lo que permite ajustarlos según la tolerancia al riesgo individual.

Análisis de Riesgos

La estrategia depende de indicadores técnicos y no puede hacer frente a cambios fundamentales importantes.

Una configuración inadecuada de los parámetros de las Bandas de Bollinger puede generar señales de trading demasiado frecuentes o demasiado escasas.

El riesgo de operar en ambos sentidos es mayor, por lo que se debe tener precaución ante las pérdidas en posiciones cortas.

Se recomienda combinar con un stop-loss para controlar el riesgo.

Direcciones de Optimización

-

Combinar con otros indicadores para filtrar señales, por ejemplo, MACD.

-

Agregar una estrategia de stop-loss.

-

Optimizar los parámetros de las Bandas de Bollinger y el RSI.

-

Ajustar los parámetros según diferentes instrumentos y marcos temporales.

-

Considerar la optimización en trading real para ajustar los parámetros a las condiciones reales.

Resumen

La estrategia de Captura Dinámica de Amplitud con RSI y Bandas de Bollinger es una estrategia impulsada por indicadores técnicos que combina las ventajas de las Bandas de Bollinger, el RSI y la SMA, ajustando dinámicamente las Bandas de Bollinger para capturar la volatilidad del mercado. Esta estrategia ofrece un amplio margen de personalización y optimización, pero no puede predecir cambios fundamentales. Se recomienda probar su efectividad en trading real y, si es necesario, ajustar los parámetros o agregar otros indicadores para reducir el riesgo.

- 1