Estrategia de cruce de medias móviles dobles

Resumen

Esta estrategia se basa en el seguimiento de tendencias mediante el cruce de medias móviles dobles. Combina una media móvil simple rápida (SMA) y una media móvil ponderada lenta (VWMA), utilizando los cruces de ambas medias para generar señales de compra y venta.

Cuando la SMA rápida cruza hacia arriba la VWMA lenta, se genera una señal de compra; cuando la SMA rápida cruza hacia abajo la VWMA lenta, se genera una señal de venta. La estrategia incorpora un mecanismo de stop loss para controlar el riesgo.

Principio de la estrategia

La lógica central de esta estrategia se basa en un sistema de cruce de medias móviles dobles. Específicamente, utiliza los siguientes indicadores técnicos:

- Media Móvil Simple (SMA): Calcula la media aritmética de los precios de cierre de los últimos n días, reflejando el precio promedio del período reciente.

- Media Móvil Ponderada (VWMA): Calcula un promedio ponderado de los precios de cierre de los últimos n días, otorgando mayor peso a los precios más recientes, lo que permite una respuesta más rápida a los cambios de precios.

En el sistema de medias dobles, la SMA rápida tiene un período corto, lo que permite reaccionar rápidamente a los cambios de precio; la VWMA lenta tiene un período más largo y actúa como filtro. Cuando las tendencias de corto y largo plazo se mueven en la misma dirección, el cruce hacia arriba de la SMA rápida sobre la VWMA lenta genera una señal de compra; el cruce hacia abajo genera una señal de venta.

La estrategia también incorpora un mecanismo de stop loss. Cuando el precio se mueve en dirección desfavorable, se detiene la pérdida a tiempo para controlar el riesgo.

Ventajas

- Respuesta rápida, siguiendo los cambios de tendencia del mercado.

- Buen control de retrocesos, el mecanismo de stop loss gestiona eficazmente el riesgo.

- Simple e intuitiva, fácil de entender e implementar.

- Se puede optimizar ajustando los parámetros para adaptarse a diferentes entornos de mercado.

Análisis de riesgos

- Las estrategias de medias móviles dobles tienden a generar señales falsas en mercados laterales.

- Es necesario seleccionar parámetros adecuados; una configuración incorrecta puede provocar pérdidas.

- Ocasionalmente, eventos imprevistos del mercado pueden causar pérdidas.

Métodos de control de riesgos:

- Utilizar indicadores de filtro de tendencia para confirmar las señales.

- Optimizar la configuración de parámetros.

- Aplicar estrategias de stop loss para controlar razonablemente las pérdidas por operación.

Direcciones de optimización

Esta estrategia se puede optimizar en los siguientes aspectos:

- Combinar con otros indicadores técnicos para confirmación, como RSI, Bandas de Bollinger, etc., mejorando la precisión de las señales.

- Ajustar la longitud de los parámetros de las medias móviles según diferentes períodos de tiempo.

- Incorporar indicadores de volumen, operando en puntos con alta entrada de energía.

- Ajustar los parámetros según los resultados del backtesting para seleccionar los valores óptimos.

- Utilizar stop loss dinámico, ajustando el nivel de stop según la volatilidad del mercado.

Resumen

En general, esta estrategia es una estrategia de seguimiento de tendencias muy práctica. Utiliza un cruce de medias móviles dobles simple e intuitivo para generar señales de trading. Mediante la combinación de una media rápida y una media lenta, puede capturar eficazmente los cambios de tendencia del mercado. El mecanismo de stop loss también proporciona un buen control de riesgos. Al combinarla con otros indicadores y optimizar los parámetros, se puede mejorar aún más el rendimiento de la estrategia.

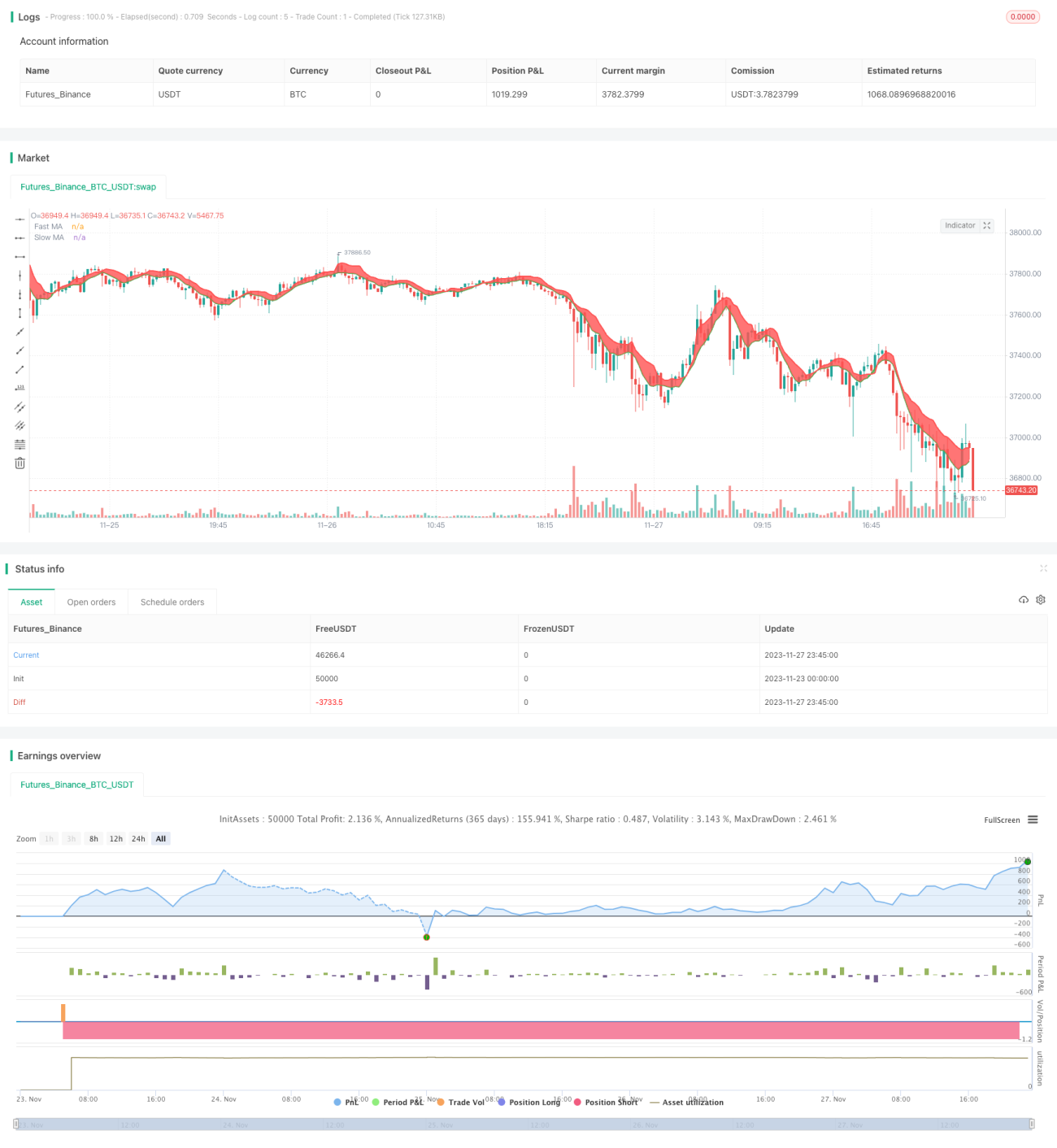

/*backtest

start: 2023-11-23 00:00:00

end: 2023-11-28 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//strategy(title="Bitlinc Entry v0.1 VWMA / SMA / MRSI SQQQ 94M", overlay=true, initial_capital=10000, currency='USD')

strategy(title="Bitlinc Entry v0.1 VWMA / SMA / MRSI SQQQ 94M", overlay=true)- 1