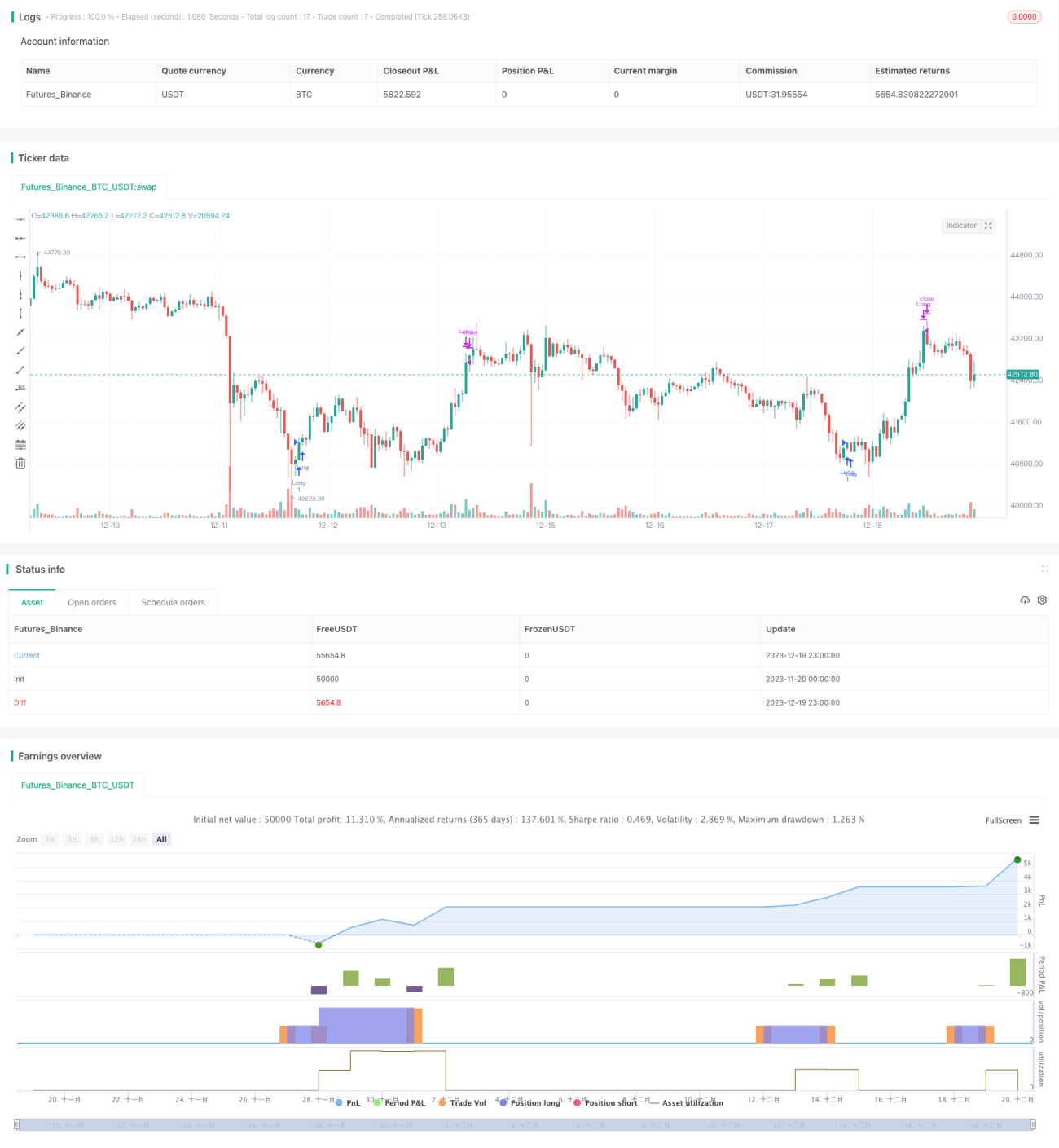

Estrategia de trading multi-timeframe basada en indicadores de volatilidad y estocástico

Resumen

Esta estrategia combina el índice de volatilidad VIX y el indicador estocástico RSI, mediante la combinación de indicadores de diferentes marcos temporales, logrando una eficiente compra en rupturas y un cierre de posiciones basado en condiciones de sobrecompra/sobreventa. El espacio de optimización de la estrategia es amplio, lo que permite adaptarse a diferentes entornos de mercado.

Principio de la estrategia

-

Cálculo del índice de volatilidad VIX: se toma el máximo y mínimo de los últimos 20 días para calcular la volatilidad. Cuando la volatilidad supera la banda superior, indica pánico en el mercado; cuando está por debajo de la banda inferior, indica complacencia del mercado.

-

Cálculo del RSI: se calcula con la ganancia/pérdida de los últimos 14 días. Cuando el RSI supera 70, se considera zona de sobrecompra; por debajo de 30, zona de sobreventa.

-

Combinación de ambos indicadores: se abre posición larga cuando la volatilidad está por encima de la banda superior o en el percentil más alto; se cierra la posición cuando el RSI supera 70.

Ventajas de la estrategia

- Integra múltiples indicadores para evaluar el momento del mercado de forma integral.

- Indicadores de diferentes marcos temporales se validan mutuamente, mejorando la precisión de las decisiones.

- Parámetros ajustables para adaptarse a diferentes instrumentos de trading.

Análisis de riesgos

- Una configuración inadecuada de parámetros puede generar múltiples señales falsas.

- Depender de un solo indicador de cierre puede omitir reversiones de precio.

Recomendaciones de optimización

- Agregar más indicadores de validación, como medias móviles o bandas de Bollinger, para determinar los puntos de entrada.

- Incluir más indicadores de cierre, como patrones de velas de reversión.

Resumen

Esta estrategia utiliza el índice VIX para evaluar el momento y el nivel de riesgo del mercado, combinado con el RSI para filtrar puntos de trading desfavorables de sobrecompra/sobreventa, logrando así comprar en momentos eficientes y realizar stop-loss oportunos. El espacio de optimización es amplio, permitiendo adaptarse a una gama más amplia de entornos de mercado.

- 1