Estrategia de seguimiento de tendencia con cruce de indicador de momentum y reversión

Resumen

Esta estrategia integra múltiples indicadores de momento técnico como MACD, RSI y ADX para identificar señales de reversión de precios, utilizando una estrategia inversa que ingresa en contra de la tendencia cuando se produce una reversión fuerte. La estrategia también establece stop loss y take profit para asegurar ganancias y controlar el riesgo.

Principio de la Estrategia

La estrategia primero combina el indicador MACD para determinar la tendencia de los precios mediante el cruce de sus medias rápidas y lentas (cruce dorado o de la muerte). Luego, utiliza el indicador RSI para filtrar falsas rupturas, asegurando que la señal de trading se genere solo después de que se haya producido una reversión real de precios. Finalmente, emplea el indicador ADX para verificar nuevamente si el precio ha entrado en un estado de tendencia. Solo cuando se cumplen simultáneamente varias de estas condiciones se genera una señal de compra o venta.

Específicamente, cuando la línea rápida del MACD cruza por encima de la línea lenta, el RSI está por encima de 50 y subiendo, y el ADX está por encima de 20, se genera una señal de compra. Cuando la línea rápida del MACD cruza por debajo de la línea lenta, el RSI está por debajo de 50 y bajando, y el ADX está por encima de 20, se genera una señal de venta.

Análisis de Ventajas

La mayor ventaja de esta estrategia es que utiliza la combinación de múltiples indicadores, lo que permite filtrar eficazmente los mercados laterales y las señales erróneas, identificando con precisión los puntos de reversión de tendencia, logrando así una alta tasa de aciertos. Además, el establecimiento de stop loss y take profit asegura las ganancias y controla el riesgo, protegiendo eficazmente contra el impacto de eventos inesperados.

Análisis de Riesgos

El mayor riesgo de esta estrategia radica en un posible error en la identificación de la reversión de tendencia, por ejemplo, cuando se produce una corrección profunda de precios que genera una señal falsa. Además, la nueva tendencia después de la reversión puede no tener la suficiente persistencia para generar ganancias adecuadas.

La solución consiste en optimizar aún más los parámetros, ajustar el margen del stop loss o incorporar más indicadores auxiliares para filtrar señales.

Direcciones de Optimización

Esta estrategia se puede optimizar aún más en los siguientes aspectos:

- Optimizar la combinación de parámetros de MACD y RSI para mejorar la precisión en la identificación de reversiones de precios.

- Agregar más filtros de indicadores, como KD, BOLL, etc., creando un efecto envolvente de indicadores.

- Ajustar dinámicamente el margen del stop loss según las diferentes condiciones del mercado.

- Modificar el nivel de take profit en tiempo real según la evolución real después de la reversión.

Resumen

Esta estrategia integra múltiples indicadores de momento para identificar oportunidades potenciales de reversión de precios. Mediante la optimización de parámetros, la combinación de más indicadores auxiliares y el ajuste dinámico de las estrategias de stop loss y take profit, se puede mejorar aún más la estabilidad y fiabilidad de la estrategia, aprovechando las diversas oportunidades de trading que ofrece el mercado.

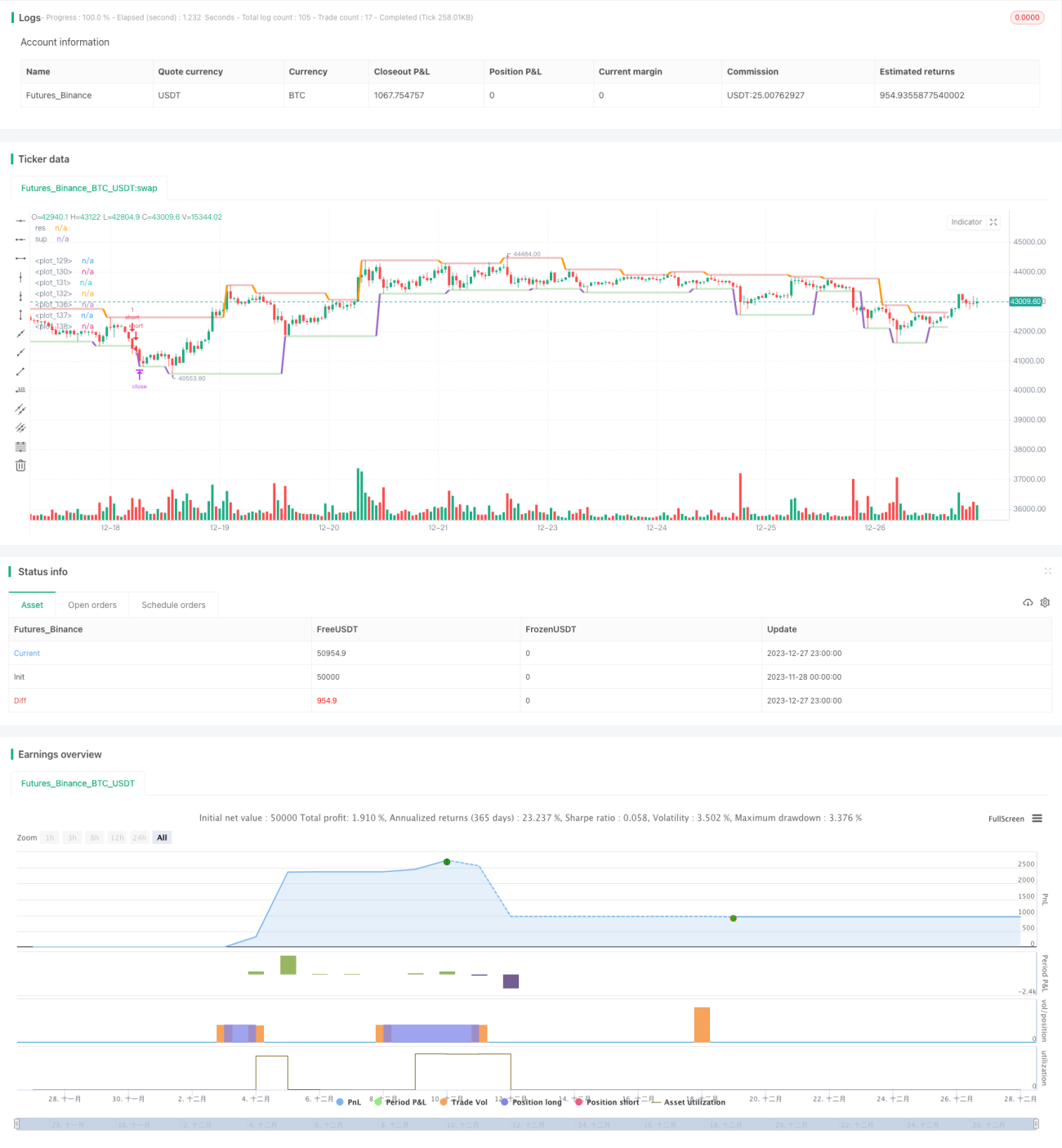

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © AHMEDABDELAZIZZIZO

//@version=5- 1