Estrategia de doble media móvil combinada con el oscilador estocástico

Resumen

Este artículo presenta una estrategia de trading cuantitativa que combina una estrategia de doble media móvil y el indicador estocástico. La estrategia utiliza conjuntamente la capacidad de seguimiento de tendencia de las medias móviles y las características de sobrecompra/sobreventa del indicador estocástico para generar señales de trading.

Principio de la Estrategia

La estrategia consta de dos partes:

-

Estrategia de doble media móvil

Utiliza una media móvil rápida y una media móvil lenta para generar señales de compra (cruce dorado) y señales de venta (cruce de la muerte). La media rápida captura más rápidamente los cambios de precio, mientras que la media lenta filtra señales falsas. -

Indicador estocástico

Aprovecha las características oscilantes del estocástico para identificar situaciones de sobrecompra y sobreventa. Cuando el estocástico está por encima de su línea lenta, es señal de sobrecompra; cuando está por debajo, es señal de sobreventa.

Las señales de ambas partes se combinan para formar la señal final de trading. La estrategia de doble media móvil sigue la tendencia principal, mientras que el estocástico ayuda a evitar condiciones de mercado desfavorables.

Ventajas de la Estrategia

- Combina las fortalezas de la doble media móvil y el estocástico, resultando más estable.

- El seguimiento de tendencia de las medias móviles, confirmado por el estocástico, ofrece buenos resultados.

- Permite personalizar parámetros para adaptarse a diferentes condiciones del mercado.

Riesgos de la Estrategia

- La doble media móvil puede generar señales falsas.

- Una mala configuración de los parámetros del estocástico puede hacer que se pierda la tendencia.

- Se requiere ajustar los parámetros para adaptarse a los cambios del mercado.

Se puede reducir el riesgo optimizando la combinación de parámetros, o incorporando un stop loss para limitar pérdidas.

Direcciones de Optimización

La estrategia se puede optimizar en los siguientes aspectos:

- Probar el impacto de diferentes parámetros de medias móviles en el rendimiento de la estrategia.

- Probar el impacto de diferentes parámetros del estocástico en la estabilidad de la estrategia.

- Añadir filtros de tendencia para mejorar la tasa de acierto.

- Establecer un mecanismo de stop loss dinámico para controlar las pérdidas.

Conclusión

Esta estrategia aprovecha las ventajas de la doble media móvil y el indicador estocástico. Sigue la tendencia principal del mercado mientras evita reversiones en condiciones desfavorables. Se puede obtener un mejor rendimiento optimizando la combinación de parámetros. Incorporar stop loss y filtros de tendencia hace que la estrategia sea más sólida.

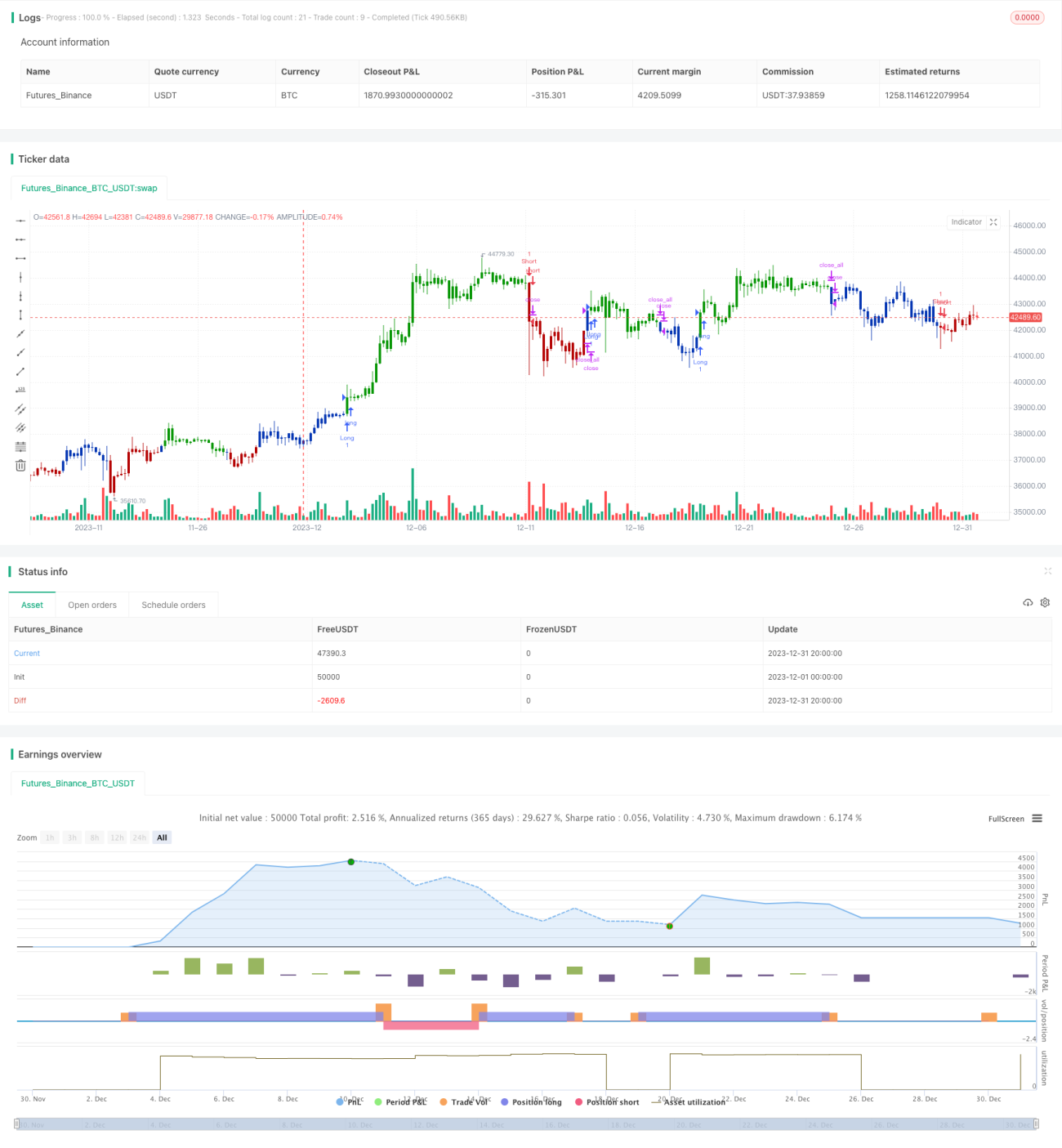

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 24/11/2020

// This is combo strategies for get a cumulative signal. - 1