Estrategia de reversión de RSI del indicador MACD

Resumen

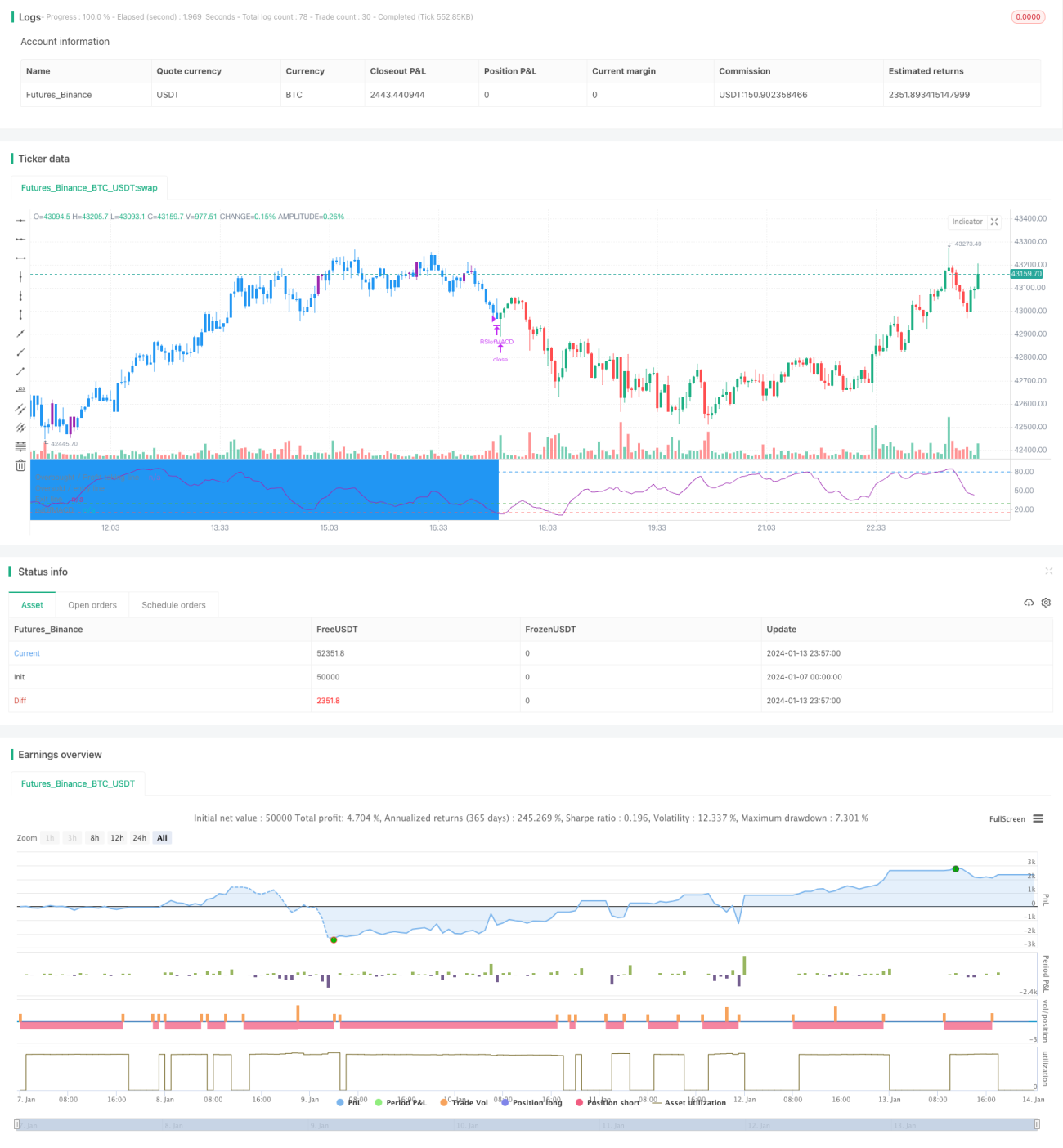

Esta estrategia utiliza el valor RSI del indicador MACD para determinar señales de compra y venta. Se genera una señal de compra cuando el RSI supera la línea de sobrecompra o la zona de sobreventa, y se cierra la posición (stop-loss o take-profit) cuando el RSI cae por debajo de la zona de sobreventa.

Principio de la estrategia

La estrategia combina las ventajas del indicador MACD y el RSI.

Primero se calculan las tres líneas del MACD: la línea DIF, la línea DEA y la línea MACD. Luego se calcula el RSI sobre la línea MACD, formando el RSI of MACD.

Cuando el RSI of MACD supera la zona de sobreventa de 30 o 35, se genera una señal de compra, indicando que la línea MACD ha entrado en zona de sobreventa y la tendencia del precio comienza a revertirse al alza. Cuando el RSI of MACD vuelve a caer por debajo de la zona de sobreventa de 15, se genera una señal de venta, indicando el fin de la reversión de tendencia.

La estrategia también establece un take-profit parcial: cuando el RSI of MACD supera la zona de sobrecompra de 80, se puede vender una parte de la posición para asegurar ganancias parciales.

Análisis de ventajas

- Utiliza el MACD para identificar puntos de reversión de tendencia.

- Utiliza el RSI para identificar zonas de sobrecompra/sobreventa y filtrar señales falsas.

- La combinación de ambos indicadores permite localizar con precisión puntos de entrada y salida.

- Establece un take-profit parcial para evitar que las pérdidas se amplíen.

Análisis de riesgos

- Una parametrización inadecuada del MACD impide identificar correctamente la tendencia.

- Una parametrización inadecuada del RSI impide identificar correctamente sobrecompra/sobreventa.

- Un take-profit parcial demasiado agresivo puede hacer que se pierdan subidas mayores.

Soluciones:

- Optimizar los parámetros del MACD para encontrar la mejor combinación.

- Optimizar los parámetros del RSI para mejorar la precisión.

- Relajar adecuadamente las condiciones del take-profit parcial para buscar mayores ganancias.

Direcciones de optimización

La estrategia también se puede optimizar en los siguientes aspectos:

- Añadir una estrategia de stop-loss para controlar aún más el riesgo a la baja.

- Incorporar un módulo de gestión de posición que permita aumentar el tamaño de la posición gradualmente conforme se mueve el precio.

- Integrar modelos de machine learning entrenados con datos históricos para mejorar aún más la precisión en la identificación de puntos de compra/venta.

- Probar en periodos más cortos, como gráficos de 15 o 5 minutos, para aumentar la frecuencia de la estrategia.

Resumen

El diseño general de la estrategia es claro, con la idea central de utilizar la reversión del MACD combinada con el filtro del RSI para determinar puntos de entrada y salida. Mediante la optimización de parámetros, la gestión de stop-loss y el control de riesgos, se puede convertir en una estrategia de trading cuantitativo muy práctica.

- 1