Estrategia de trading multi-timeframe basada en RSI y medias móviles

Resumen

Esta estrategia combina el indicador estocástico RSI, la media móvil simple (SMA) y la media móvil ponderada (WMA) para encontrar señales de compra y venta. Al mismo tiempo, determina la dirección de la tendencia en los marcos temporales de 5 minutos y 1 hora. Cuando el RSI de la línea rápida cruza por encima o por debajo de la línea lenta dentro de una tendencia estabilizada, se genera una señal de trading.

Principio de la estrategia

Primero, la estrategia calcula la media móvil ponderada (WMA) de 144 periodos y la media móvil simple (SMA) de 5 periodos en los dos marcos temporales de 1 hora y 5 minutos. Solo cuando la SMA de 5 minutos está por encima de la WMA se considera un mercado alcista. Luego, la estrategia calcula el indicador de RSI para largo y corto, así como las correspondientes líneas K y D. Cuando la línea K cruza por debajo de la línea D desde una zona de sobrecompra, se genera una señal de venta; cuando la línea K cruza por encima de la línea D desde una zona de sobreventa, se genera una señal de compra.

Análisis de ventajas

Esta es una estrategia de seguimiento de tendencia muy efectiva. Al combinar dos marcos temporales para juzgar la tendencia, reduce de manera muy eficaz las señales falsas. Además, incorpora múltiples indicadores para filtrar, incluyendo RSI, SMA y WMA, lo que hace que las señales sean más fiables. Al hacer que el RSI impulse el KDJ, también mitiga el problema de señales falsas que suelen aparecer en las estrategias convencionales de KDJ. Asimismo, la estrategia incorpora ajustes de stop loss y take profit para asegurar ganancias y controlar el riesgo de manera efectiva.

Análisis de riesgos

El mayor riesgo de esta estrategia radica en un juicio erróneo de la tendencia. En los puntos de inflexión del mercado, las medias móviles de corto y largo plazo pueden cruzar simultáneamente al alza o a la baja, generando señales falsas. Además, en mercados laterales, el RSI también puede producir numerosas señales de trading contradictorias. Sin embargo, estos riesgos pueden mitigarse ajustando adecuadamente los periodos de la SMA, la WMA y los parámetros del RSI.

Direcciones de optimización

La estrategia se puede optimizar desde los siguientes aspectos:

- Probar diferentes longitudes de SMA, WMA y RSI para encontrar la combinación óptima de parámetros.

- Agregar otros indicadores de juicio, como MACD, Bandas de Bollinger, etc., para verificar la fiabilidad de las señales.

- Optimizar las estrategias de stop loss y take profit, probando métodos como stop loss de porcentaje fijo, stop loss por deslizamiento de saldo, stop loss dinámico, etc.

- Incorporar un módulo de gestión de capital para controlar el tamaño de la inversión por operación y la exposición total al riesgo.

- Añadir algoritmos de aprendizaje automático para encontrar los parámetros con mejor rendimiento mediante un gran número de backtests.

Resumen

Esta estrategia aprovecha plenamente las ventajas de las medias móviles y los indicadores estocásticos para construir un sistema de seguimiento de tendencias bastante fiable. Mediante la verificación con múltiples marcos temporales e indicadores, es capaz de capturar con fluidez la dirección de las tendencias de medio y largo plazo. Al mismo tiempo, la configuración de stop loss y take profit le permite soportar cierto grado de volatilidad del mercado. No obstante, todavía hay margen de mejora, como probar la combinación de más indicadores o introducir métodos de aprendizaje automático para encontrar los parámetros óptimos. En general, es una estrategia de trading muy prometedora.

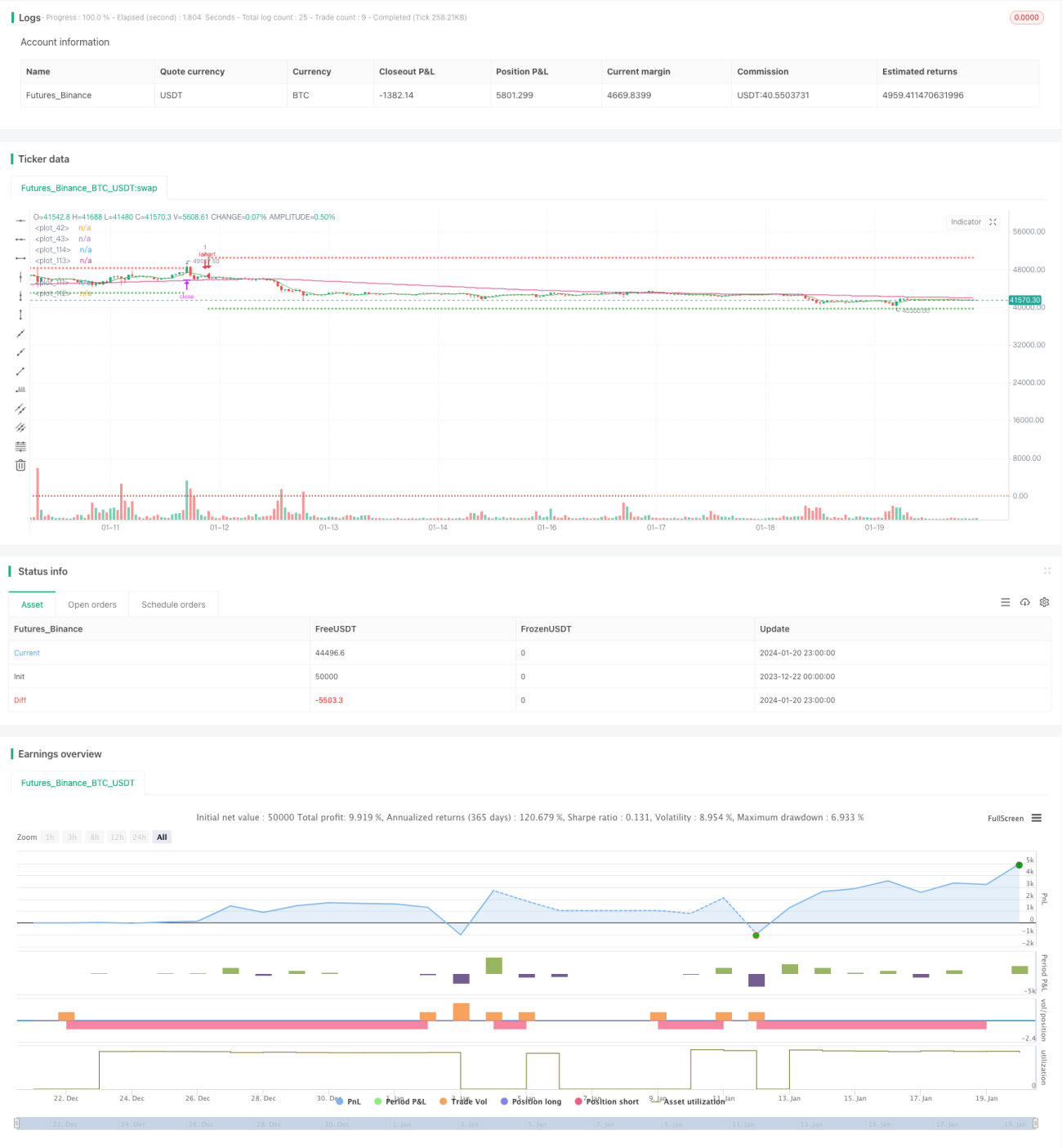

/*backtest

start: 2023-12-22 00:00:00

end: 2024-01-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © bufirolas

// Works well with a wide stop with 20 bars lookback- 1