Estrategia de seguimiento de momentum con filtro de rango adaptativo bidireccional

1

Follow

1802

Followers

Resumen

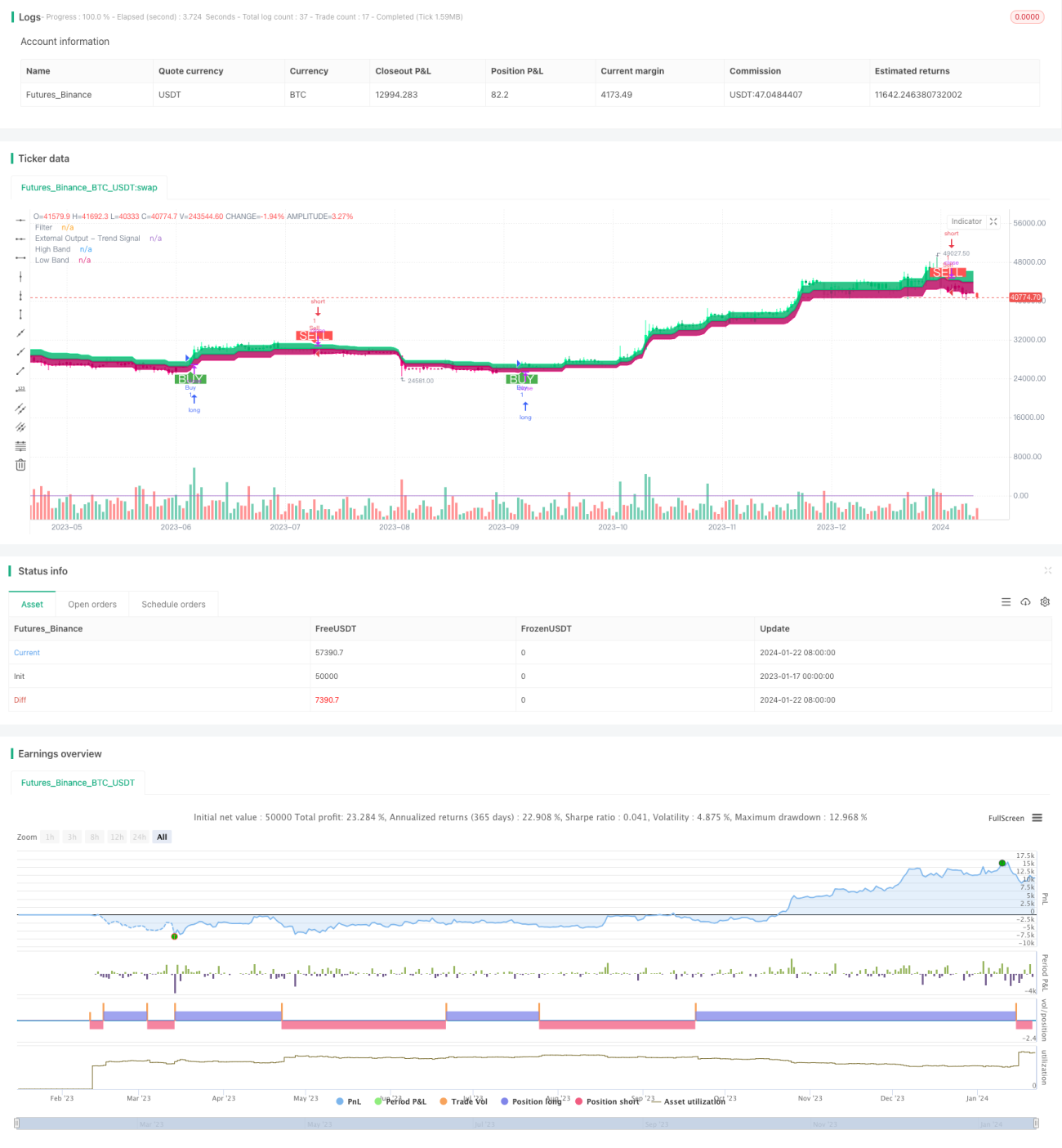

Esta estrategia es una estrategia de seguimiento de momentum con filtro de rango adaptativo bidireccional. Utiliza un filtro de rango adaptativo para rastrear las fluctuaciones de precios y combina indicadores de volumen para determinar la dirección del valor, logrando comprar barato y vender caro.

Principio de la estrategia

- Utiliza un filtro de rango adaptativo para rastrear las fluctuaciones de precios. El tamaño del filtro se ajusta adaptativamente según el período de rango, la cantidad y la escala definidos por el usuario.

- El filtro se divide en dos tipos: Tipo 1 y Tipo 2. El Tipo 1 es de seguimiento de rango estándar, y el Tipo 2 es de redondeo escalonado.

- Basándose en la relación entre el filtro y el precio de cierre, se determina la dirección de la fluctuación del precio. Cuando el precio está por encima de la banda superior, es alcista; por debajo de la banda inferior, es bajista.

- Combinando el cambio del precio de cierre en relación con el día anterior, se determina la dirección del valor. Un aumento del valor indica una tendencia alcista, y una disminución indica una tendencia bajista.

- Cuando el precio supera la banda superior y el valor aumenta, se genera una señal de compra; cuando el precio cae por debajo de la banda inferior y el valor disminuye, se genera una señal de venta.

Análisis de ventajas

- El filtro de rango adaptativo puede capturar con precisión las fluctuaciones del mercado.

- Los dos tipos de filtros satisfacen diferentes preferencias de trading.

- La combinación con indicadores de volumen permite identificar eficazmente la dirección del valor.

- La estrategia es flexible y permite ajustar parámetros según el mercado.

- Es posible personalizar la lógica de condiciones de trading adecuadas.

Análisis de riesgos

- Una configuración inadecuada de parámetros puede provocar exceso de trading o pérdida de señales.

- Las señales de ruptura tienen cierto retraso.

- Los indicadores de volumen pueden presentar cierto riesgo de retraso.

- Las rupturas de rango pueden generar trampas.

Prevención de riesgos:

- Seleccionar la combinación adecuada de parámetros y ajustarla oportunamente.

- Combinar con otros indicadores para identificar la tendencia.

- Operar con cautela cerca de niveles clave y en puntos de reversión de tendencia.

Direcciones de optimización

- Probar diferentes combinaciones de tamaño de rango y períodos de suavizado para encontrar la combinación óptima.

- Probar diferentes tipos de filtros y elegir el tipo preferido.

- Experimentar con otros indicadores de volumen o indicadores técnicos auxiliares.

- Optimizar y ajustar la lógica de condiciones de trading para reducir operaciones irracionales.

- Combinar con la teoría de patrones de mercado para establecer una proporción de ajuste adaptativo de posiciones.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1