Estrategia de seguimiento de tendencias basada en medias móviles

Resumen

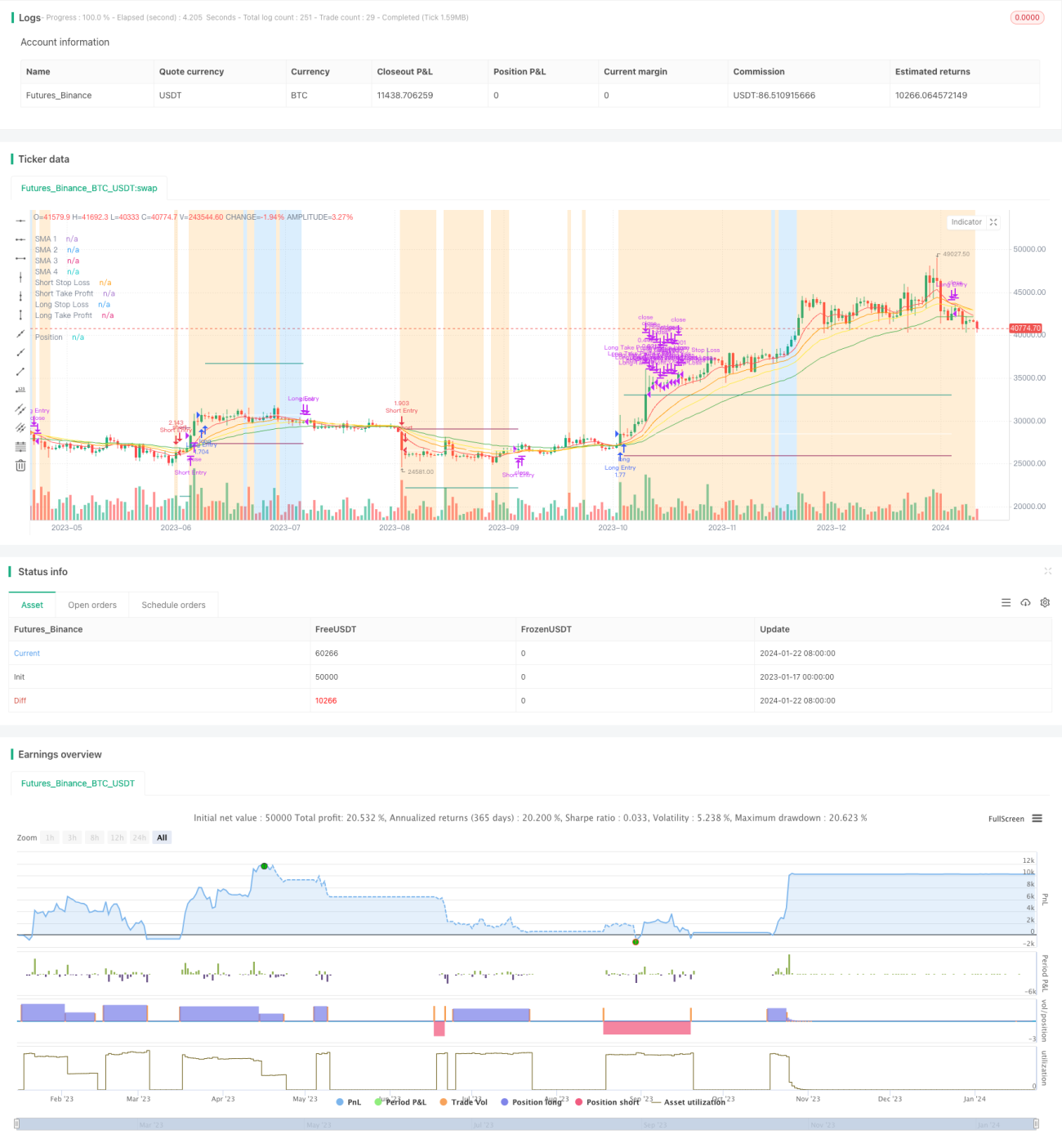

Esta estrategia es una estrategia simple de seguimiento de tendencias basada en medias móviles. Determina la dirección actual de la tendencia y su duración comparando la relación de tamaño entre medias móviles de diferentes períodos. Cuando la media móvil de corto plazo cruza al alza la media móvil de largo plazo, se abre una posición larga; cuando la cruza a la baja, se abre una posición corta. Además, la estrategia establece puntos de stop loss y take profit para controlar el riesgo.

Principio de la estrategia

La estrategia utiliza 4 medias móviles de diferentes períodos: de 5 días, 10 días, 15 días y 25 días. Estas cuatro medias se denominan MA1, MA2, MA3 y MA4. MA1 es la más corta y MA4 la más larga.

Cuando MA1 > MA2 > MA3 > MA4, indica que el precio está en una tendencia alcista, por lo que se abre una posición larga. Cuando MA1 < MA2 < MA3 < MA4, indica que el precio está en una tendencia bajista, por lo que se abre una posición corta.

Las condiciones de apertura de posiciones largas y cortas también deben cumplir simultáneamente el filtro de stop loss basado en ATR, es decir, el valor del ATR debe ser mayor que su media móvil simple de 40 períodos. Esto evita que se generen señales falsas cuando la volatilidad del precio es demasiado baja.

Ventajas de la estrategia

La estrategia tiene las siguientes ventajas:

- El concepto es simple y fácil de entender, y fácil de implementar.

- El uso de múltiples medias móviles para determinar la dirección de la tendencia es confiable.

- El establecimiento de puntos de take profit y stop loss permite controlar eficazmente la pérdida máxima por operación.

- El filtro de stop loss basado en ATR evita señales falsas cuando la volatilidad del precio es demasiado baja.

Análisis de riesgos

Esta estrategia también presenta los siguientes riesgos:

- En mercados con fuertes oscilaciones puede generar señales falsas con facilidad.

- Una configuración inadecuada de parámetros (períodos de medias móviles, etc.) puede resultar en un rendimiento deficiente de la estrategia.

- No se consideran los fundamentos ni el impacto de noticias importantes en el precio.

Para reducir estos riesgos, se pueden optimizar los parámetros adecuadamente o agregar otros filtros para mejorar la estabilidad de la estrategia.

Direcciones de optimización

Las direcciones de optimización de esta estrategia son:

- Probar diferentes combinaciones de períodos de medias móviles para encontrar los parámetros óptimos.

- Agregar filtros de otros indicadores técnicos, como MACD, KDJ, etc., para evaluar la fiabilidad de las señales.

- Incorporar un filtro de volumen de operaciones, realizando transacciones solo cuando el volumen aumente.

- Realizar una optimización detallada de parámetros por instrumento, según las diferencias en cada activo.

- Agregar algoritmos de aprendizaje automático para evaluar las señales.

Resumen

En general, esta estrategia es una estrategia simple de seguimiento de tendencias que utiliza medias móviles para determinar la dirección de la tendencia y establece niveles razonables de take profit y stop loss para controlar el riesgo. El margen de optimización es amplio; mediante ajustes de parámetros y la adición de filtros, se puede mejorar aún más la estabilidad y rentabilidad de la estrategia.

- 1