This strategy is a bidirectional adaptive range filtering momentum tracking strategy

Overview

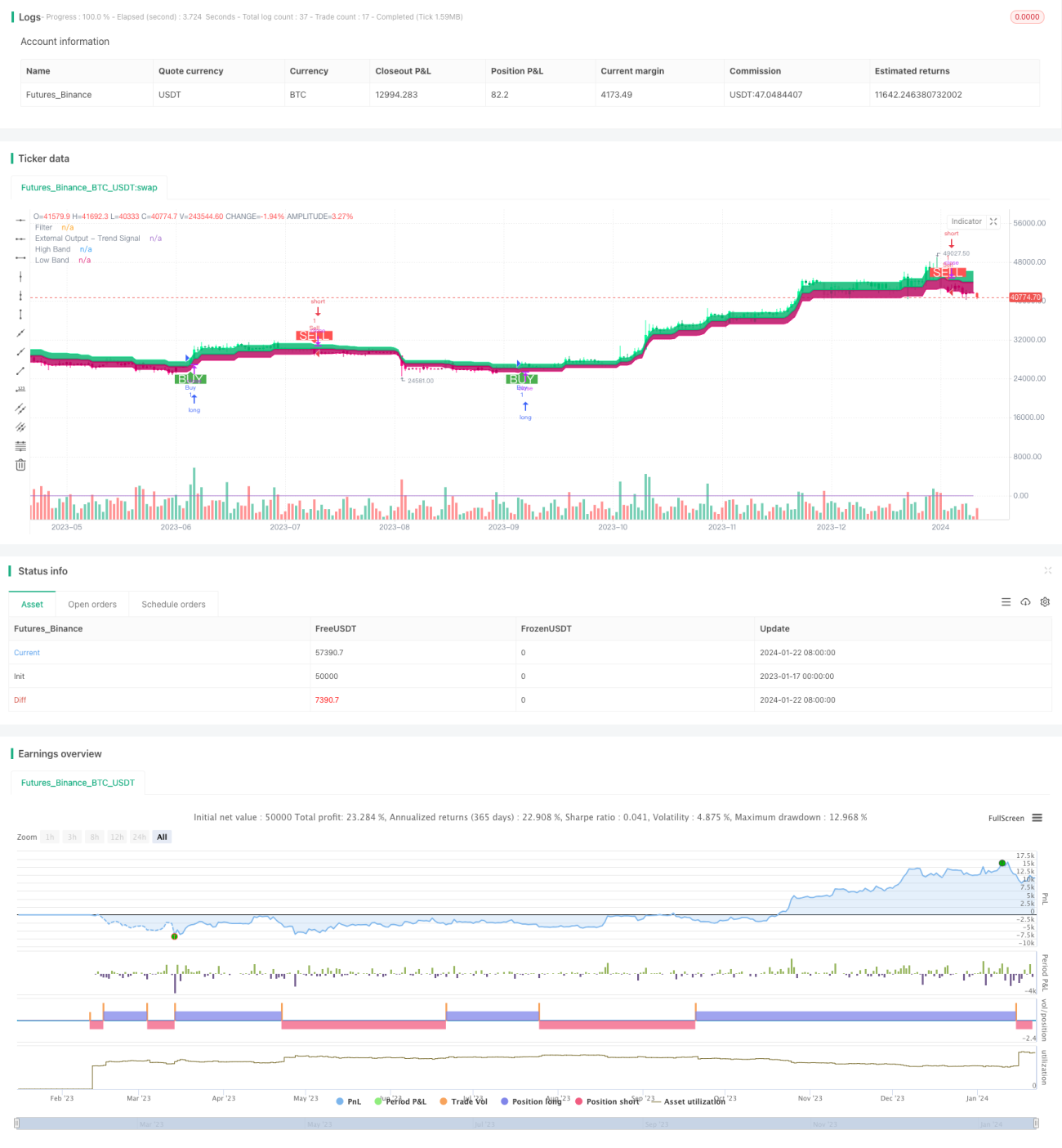

This strategy is a bidirectional adaptive range filtering momentum tracking strategy. It uses an adaptive range filter to track price fluctuations and combines volume indicators to determine the direction of value, in order to implement low buying and high selling.

Strategy Principles

-

Use an adaptive range filter to track price fluctuations. The size of the filter is adjusted adaptively according to the user-defined range period, quantity and scale.

-

There are two types of filters: Type 1 and Type 2. Type 1 is a standard range tracking type, and Type 2 is a stepped rounding type.

-

Determine the direction of price fluctuation based on the relationship between the filter and the closing price. Above the upper rail is bullish, and below the lower rail is bearish.

-

Combined with the rise and fall of the closing price compared to the previous day, determine the direction of value. Value rising is bullish and value falling is bearish.

-

Issue a buy signal when the price breaks through the upper track and the value rises; Issue a sell signal when the price breaks through the lower track and the value falls.

Advantage Analysis

-

The adaptive range filter can accurately capture market fluctuations.

-

Two types of filters can meet different trading preferences.

-

Combining volume indicators can effectively identify value direction.

-

The strategy is flexible and parameters can be adjusted according to market conditions.

-

Customizable trading condition logic.

Risk Analysis

-

Improper parameter settings may lead to overtrading or missing trades.

-

Breakout signals have a certain lag.

-

Volume indicators have a certain risk of stalling.

-

Range breaks are prone to being trapped.

Risk Prevention:

-

Choose appropriate parameter combinations and adjust them in a timely manner.

-

Combine other indicators to identify trends.

-

Trade cautiously around key levels and trend reversals.

Optimization Directions

-

Test different combinations of range sizes and smoothing cycles to find the optimal combination.

-

Try different types of filters and choose your preferred type.

-

Experiment with other volume indicators or auxiliary technical indicators.

-

Optimize and adjust trading condition logic to reduce irrational trading.

-

Incorporate market theorems to set adaptive position sizing.

- 1