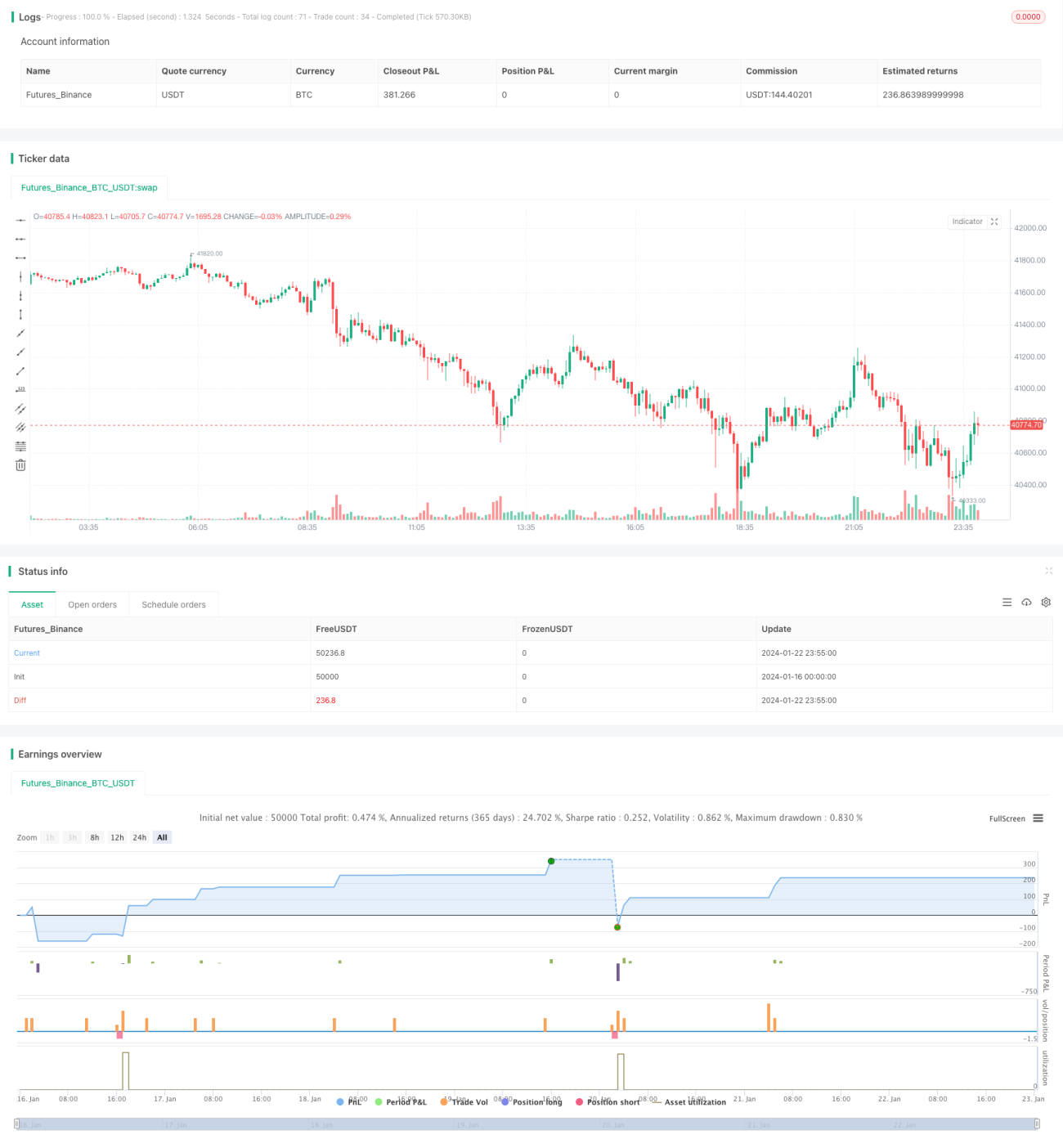

Estrategia cuantitativa utilizando el indicador RSI y el indicador de media móvil

Resumen

La estrategia de ruptura con doble RSI y medias móviles es una estrategia cuantitativa que utiliza simultáneamente el indicador RSI y las medias móviles para determinar los momentos de negociación. La idea central de la estrategia es, cuando el RSI alcanza zonas de sobrecompra o sobreventa, utilizar la dirección de la media móvil para filtrar las señales y buscar puntos de ruptura de mayor calidad para abrir posiciones.

Principio de la estrategia

-

Según los parámetros establecidos por el usuario, se calculan el indicador RSI y la media móvil simple (SMA).

-

Cuando el RSI cruza por encima de la línea de sobreventa establecida (por defecto 30), y si el precio es inferior a la media móvil de salida larga (LONG), se genera una señal larga.

-

Cuando el RSI cruza por debajo de la línea de sobrecompra establecida (por defecto 70), y si el precio es superior a la media móvil de salida corta (SHORT), se genera una señal corta.

-

El usuario puede seleccionar una media móvil de filtro; solo cuando el precio esté por encima de dicha media se generarán señales.

-

La salida de la posición se determina según la media móvil de salida larga y la media móvil de salida corta.

Análisis de ventajas

-

Diseño de doble indicador, integrando los dos factores principales del mercado para mejorar la precisión de las decisiones.

-

Uso razonable de la característica de reversión del RSI para identificar puntos de reversión oportunos.

-

El filtro de medias móviles añade rigor al juicio, evitando comprar en máximos y vender en mínimos.

-

Permite personalizar parámetros, lo que facilita la optimización para diferentes activos y plazos.

-

Lógica de diseño simple, fácil de entender y modificar.

Análisis de riesgos

-

El indicador RSI puede generar fácilmente líneas de cuello verticales; el indicador de densidad puede reducir este problema.

-

El RSI en plazos grandes tiende a perder eficacia; se puede reducir mediante optimización de parámetros o complementar con otros indicadores.

-

Las medias móviles tienen rezago; se puede acortar su longitud adecuadamente o complementar con indicadores como MACD.

-

Condiciones de juicio simples; se pueden incorporar más indicadores para asegurar la efectividad de las señales de trading.

Direcciones de optimización

-

Optimizar los parámetros del RSI o introducir el indicador de densidad para reducir la probabilidad de señales falsas.

-

Combinar indicadores de tendencia y volatilidad como DMI o Bandas de Bollinger para determinar la tendencia y niveles de soporte.

-

Introducir indicadores como MACD para reemplazar o complementar el juicio de las medias móviles.

-

Agregar lógica a las condiciones de apertura para evitar señales de ruptura no deseadas.

Resumen

La estrategia de ruptura con doble RSI y medias móviles utiliza de manera integral el indicador RSI para identificar sobrecompra/sobreventa y las medias móviles para determinar la tendencia, lo que teóricamente permite capturar oportunidades de reversión de manera efectiva. Esta estrategia es flexible y simple, fácil de comenzar, y también adecuada para la optimización en diferentes activos. Es una estrategia recomendable para quienes se inician en la cuantificación. Al incorporar más indicadores como apoyo para el juicio, esta estrategia puede mejorar aún más la efectividad de las decisiones y aumentar la probabilidad de ganancias.

- 1