Nueva estrategia de trading cuantitativo basada en el patrón ABCD con seguimiento de stop loss y seguimiento de take profit.

I. Resumen de la estrategia

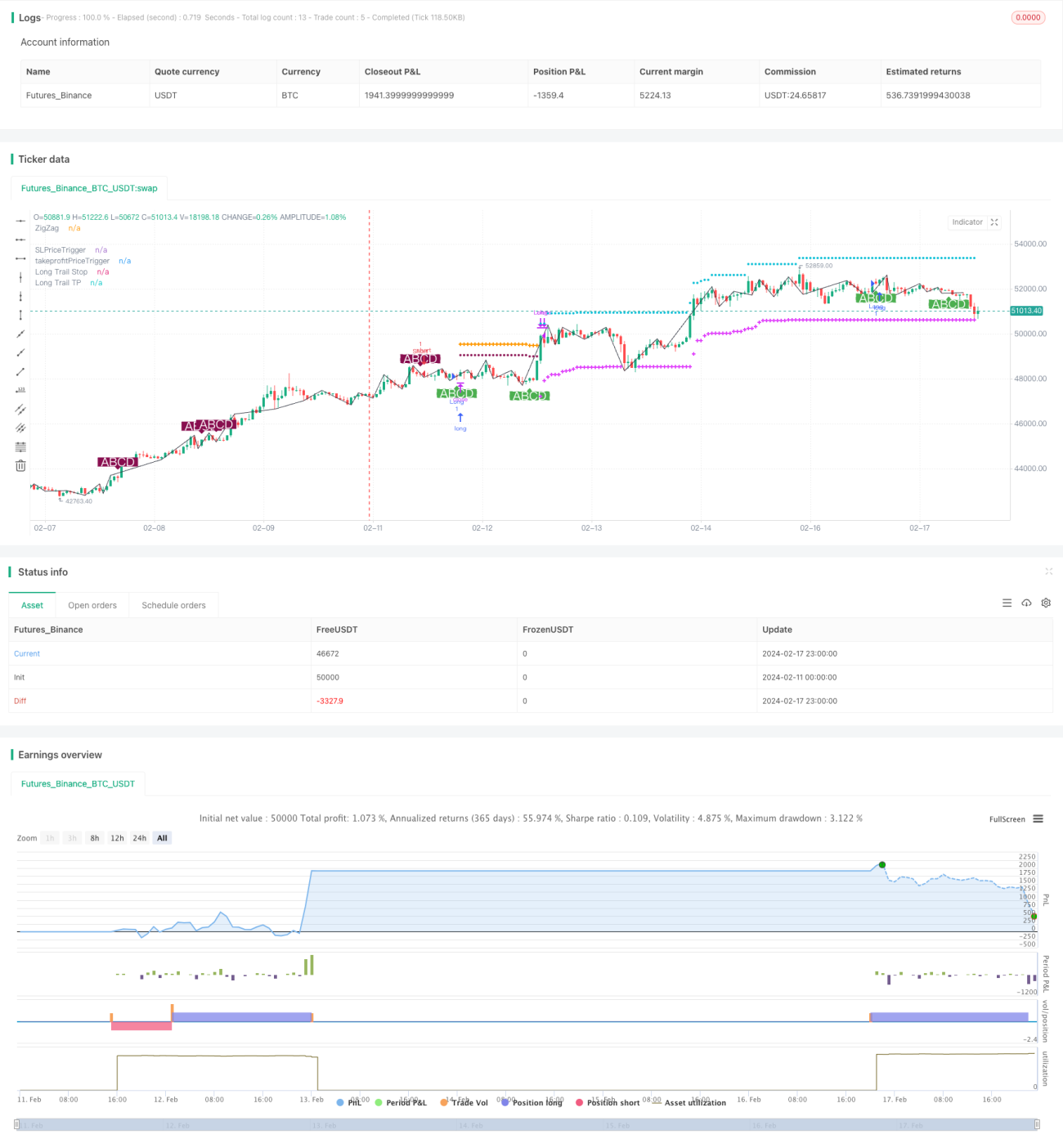

El nombre de esta estrategia es "Estrategia de trading con patrón ABCD óptimo (con trailing stop loss y trailing take profit)". Es una estrategia cuantitativa de trading basada en un modelo claro de patrón de precios ABCD. La idea principal es identificar el patrón ABCD completo y, según la dirección del patrón, tomar posiciones largas o cortas, estableciendo trailing stop loss y trailing take profit para gestionar las posiciones.

II. Principio de la estrategia

-

Utiliza el método de asistencia de Bandas de Bollinger para identificar los puntos de quiebre de máximos y mínimos del precio, obteniendo la curva ZigZag del precio.

-

Identifica el patrón ABCD completo en la curva ZigZag. Los puntos A, B, C y D deben cumplir ciertas relaciones de proporción. Tras detectar un patrón ABCD válido, se toma una posición larga o corta.

-

Después de abrir una posición larga o corta, se establece un trailing stop loss para controlar el riesgo. Inicialmente, se utiliza un stop loss fijo; cuando las ganancias alcanzan un cierto porcentaje, se convierte en un stop loss móvil para asegurar parte de las ganancias.

-

Del mismo modo, se aplica un trailing take profit a la línea de take profit para cerrar la posición oportunamente una vez obtenidas suficientes ganancias, evitando la reversión de beneficios. El trailing take profit también tiene dos fases: primero se usa un take profit fijo para obtener una parte de las ganancias, y luego se convierte en un take profit móvil para seguir la tendencia del precio.

-

Cuando el precio alcanza el trailing stop loss o take profit, se cierra la posición, completando un ciclo de trading.

III. Análisis de ventajas de la estrategia

-

El uso del método de asistencia de Bandas de Bollinger para identificar la curva ZigZag evita el problema de retroceso típico de la curva ZigZag tradicional, haciendo que las señales de trading sean más fiables.

-

El modelo de trading con patrón ABCD es maduro y estable, con oportunidades de trading relativamente abundantes. Además, la dirección del patrón ABCD es clara, facilitando la determinación de la dirección de entrada.

-

El establecimiento de un trailing stop loss y take profit en dos fases permite un mejor control del riesgo y la obtención de ganancias. El trailing stop loss/take profit móvil hace que la estrategia sea más flexible.

-

Los parámetros de la estrategia están diseñados de manera razonable: los porcentajes de stop loss, take profit y el umbral para activar el trailing son personalizables, lo que brinda flexibilidad en su uso.

-

Esta estrategia se puede aplicar a cualquier activo, incluyendo Forex, criptomonedas e índices bursátiles.

IV. Análisis de riesgos de la estrategia

-

Aunque el patrón ABCD es relativamente claro, las oportunidades de trading son limitadas, por lo que no se garantiza una frecuencia de trading suficiente.

-

En mercados laterales o con oscilaciones, es posible que se activen frecuentemente tanto el stop loss como el take profit. En estos casos, es necesario ajustar los parámetros adecuadamente, ampliando el rango del stop loss y take profit.

-

Es necesario prestar atención a la liquidez del activo negociado. En activos con baja liquidez, la ejecución precisa del stop loss y take profit puede verse afectada.

-

La estrategia es sensible a los costos de transacción, por lo que se debe elegir un bróker y una cuenta con comisiones bajas.

-

Algunos parámetros pueden seguir optimizándose, como las condiciones para activar el trailing stop loss y take profit, probando diferentes valores para encontrar el punto óptimo.

V. Direcciones de optimización de la estrategia

-

Se pueden combinar otros indicadores para establecer más filtros y evitar patrones falsos (por ejemplo, patrones HW), reduciendo así las operaciones no rentables.

-

Añadir juicio sobre la estructura de tres fases del mercado, buscando oportunidades de trading solo en la tercera fase. Esto puede aumentar la tasa de acierto de la estrategia.

-

Probar y optimizar el tamaño del capital inicial para encontrar el nivel óptimo. Un capital demasiado grande o demasiado pequeño no favorece la obtención de la mejor tasa de rendimiento.

-

Realizar pruebas con datos fuera de la muestra para verificar la robustez de los parámetros. Esto es esencial para conocer la estabilidad a medio y largo plazo de la estrategia.

-

Continuar optimizando las condiciones de activación del trailing stop loss/take profit y el tamaño del deslizamiento (slippage) para mejorar la eficiencia de ejecución de la estrategia. La optimización de parámetros es un proceso interminable.

VI. Resumen de la estrategia

Esta estrategia se basa principalmente en el patrón de precios ABCD para identificar señales y entrar en el mercado. Se establece un trailing stop loss y take profit en dos fases para gestionar el riesgo y las ganancias. La estrategia es relativamente madura y estable, pero la frecuencia de trading puede ser baja. Podemos obtener oportunidades de trading más eficientes añadiendo filtros adicionales. Además, continuar optimizando los parámetros y el tamaño del capital también puede mejorar aún más la rentabilidad estable de la estrategia. En general, la estrategia tiene una lógica clara, es fácil de entender e implementar, y es una estrategia de trading cuantitativo que merece una investigación y aplicación más profundas.

- 1