Estrategia B-Xtrender de Cruce de Medias Móviles Exponenciales

1

Follow

1802

Followers

Resumen

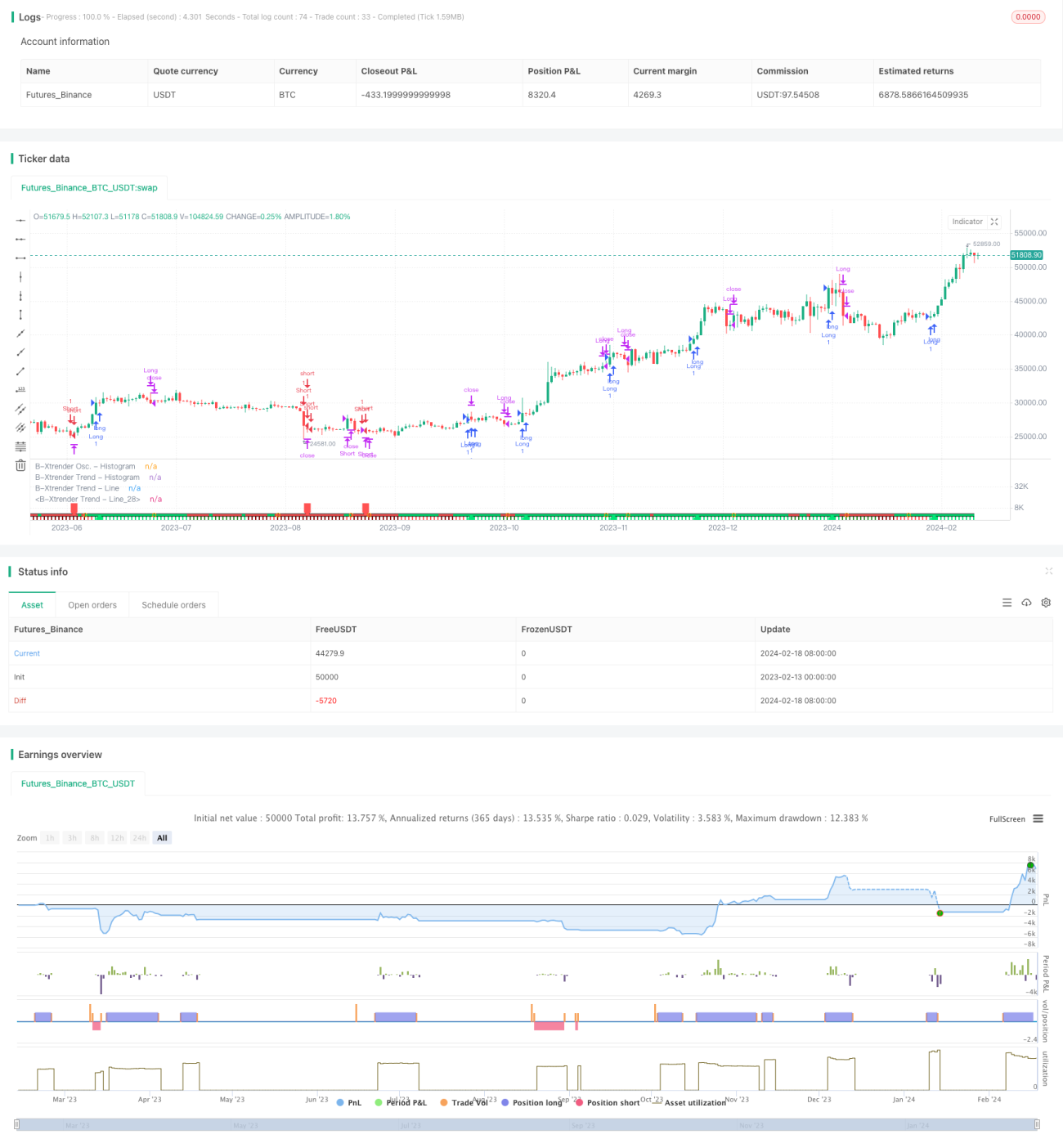

Esta estrategia es un sistema de trading basado en el cruce de medias móviles exponenciales (EMA). Combina el indicador RSI y un filtro de media móvil, formando un sistema completo de seguimiento de tendencia y trading de reversión.

Principio de la estrategia

- Utiliza el cruce rápido y lento de las medias móviles exponenciales para generar señales de trading. El cruce rápido corresponde a las EMAs de 5 y 20 periodos, y el cruce lento a las EMAs de 20 y 15 periodos.

- Cuando la EMA rápida cruza por encima de la EMA lenta, se genera una señal de compra; cuando cruza por debajo, una señal de venta. Se emplea el RSI como verificación secundaria: la señal solo se confirma si el RSI también cruza en la misma dirección.

- Se agrega la media móvil de 200 periodos como filtro: solo cuando el precio supera dicha media se emite una señal de trading, evitando así múltiples cruces falsos en mercados laterales.

Ventajas de la estrategia

- La combinación del doble cruce de EMA con el RSI mejora significativamente la fiabilidad de las señales y reduce la tasa de señales falsas.

- La combinación de parámetros rápidos y lentos de la EMA equilibra la sensibilidad de las señales con su estabilidad.

- La inclusión del filtro de media móvil filtra eficazmente el ruido en mercados laterales, evitando operaciones innecesarias.

Riesgos de la estrategia

- La EMA es un indicador rezagado, lo que provoca un retraso notable en movimientos bruscos de precio. Esto puede aumentar las pérdidas o hacer que se pierdan señales.

- Una configuración inadecuada de los parámetros del RSI también puede retrasar las señales.

- Aunque el filtro de media móvil evita operar en mercados laterales, también puede filtrar oportunidades de entrada tempranas al inicio de una tendencia.

Direcciones de optimización

- Ajustar dinámicamente los parámetros de la EMA para seleccionar la combinación óptima en diferentes ciclos.

- Probar la combinación de otros indicadores como el MACD con el RSI.

- Optimizar los parámetros del filtro de media móvil para encontrar un equilibrio entre eliminar ruido y capturar oportunidades.

Conclusión

En general, esta estrategia construye un sistema de trading basado en medias móviles exponenciales bastante completo. Sobre la base de generar señales de trading, introduce el RSI como capa adicional de verificación. Sin duda, esto mejora en gran medida la calidad de las señales, convirtiéndola en una estrategia digna de estudio y optimización. No obstante, debido al carácter rezagado de los propios indicadores, se debe prestar atención al riesgo de no detener las pérdidas a tiempo.

Source

Pine

/*backtest

start: 2023-02-13 00:00:00

end: 2024-02-19 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © QuantTherapy

//@version=4

strategy("B-Xtrender [Backtest Edition] @QuantTherapy")Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1