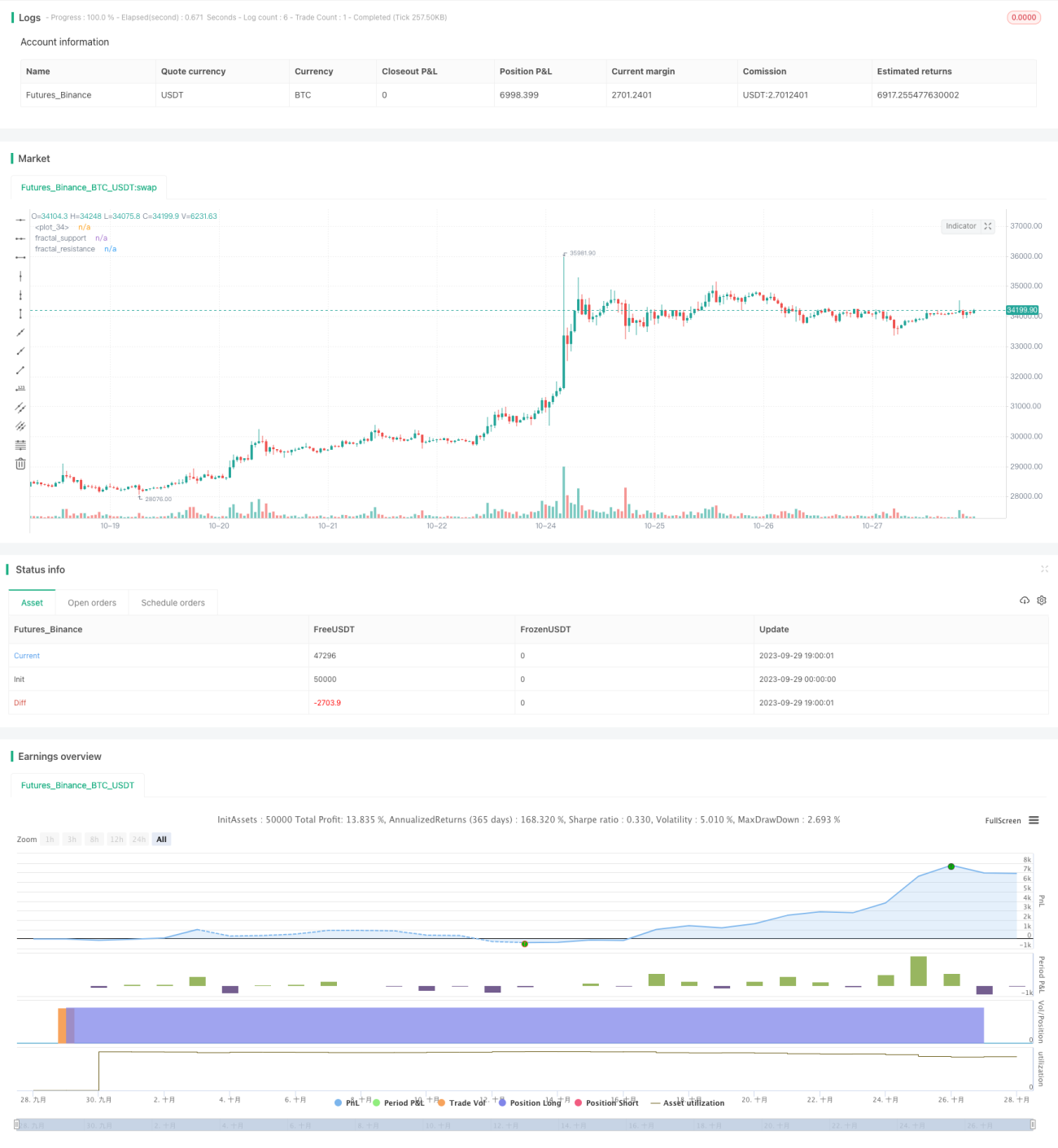

Stratégie de trading de renversement basée sur le support/résistance généralisé

Aperçu

Cette stratégie utilise des facteurs longs/courts basés sur des indicateurs pour effectuer des transactions de retournement, tout en fixant des objectifs de profit. Le facteur long/court repose sur une extension du volume d'échanges appelée « support/résistance généralisé », adaptée aux actifs à volume et volatilité élevés. L'avantage de cette stratégie est de capter d'importantes opportunités de retournement de tendance à court ou moyen terme, permettant des gains rapides ; cependant, elle comporte également un risque de piégeage.

Principe de la stratégie

-

Identification des facteurs longs/courts via le « support/résistance généralisé » basé sur le volume

-

Utilisation de figures en chandeliers pour identifier les supports/résistances classiques, en filtrant les faux dépassements avec un volume élevé.

-

Le support/résistance généralisé offre une meilleure couverture que les figures classiques.

-

La rupture du support généralisé est un signal haussier (facteur long) ; la rupture de la résistance généralisée est un signal baissier (facteur court).

-

-

Transactions de retournement

-

Après l'émission d'un signal facteur, la position est prise à contre-courant.

-

Si une position est déjà ouverte, on réduit ou on ouvre une position inverse.

-

-

Objectifs de profit

-

Stop-loss basé sur l'ATR.

-

Fixation de multiples objectifs de profit : 1R, 2R, 3R, etc.

-

Réduction progressive des positions à mesure que les objectifs sont atteints.

-

Analyse des avantages

-

Capture de retournements importants à court/moyen terme

La rupture des supports/résistances représente un signal de retournement de tendance assez fiable, permettant de capter des mouvements significatifs.

-

Gains rapides et faible drawdown

Grâce au stop-loss et aux objectifs de profit multiples, on peut réaliser des gains rapides et limiter le drawdown individuel.

-

Adapté aux actifs à forte participation institutionnelle et volatilité élevée

La stratégie dépend d'indicateurs de volume, nécessitant des flux de capitaux institutionnels suffisants pour soutenir la tendance, tout en ayant besoin d'une marge de fluctuation pour générer des profits.

Analyse des risques

-

Risque d'être piégé dans une phase de consolidation

En période de consolidation, les sorties sur stop-loss suivies de réentrées à contre-courant peuvent entraîner des piégeages fréquents.

-

Risque d'inefficacité des supports/résistances

Les supports/résistances généralisés ne sont pas absolument fiables ; il existe une probabilité d'échec lors des tests de retournement.

-

Risque de position unilatérale

La stratégie étant purement basée sur le retournement, elle ignore le suivi de tendance et peut manquer des opportunités directionnelles majeures.

-

Gestion des risques

-

Il est possible d'assouplir les conditions de facteur pour les retournements, sans inverser à chaque rupture.

-

Combinaison avec d'autres indicateurs de filtre, comme la divergence prix-volume.

-

Optimisation de la stratégie de stop-loss pour réduire la probabilité de piégeage.

-

Pistes d'optimisation

-

Optimisation des paramètres de seuil

Ajuster les paramètres du support/résistance généralisé pour identifier des facteurs plus fiables.

-

Optimisation de la stratégie de profit

Ajouter davantage de paliers d'objectifs de profit ou utiliser des objectifs non fixes.

-

Optimisation de la stratégie de stop-loss

Modifier le paramètre ATR ou utiliser un stop-loss intelligent (istics) pour réduire les coûts de transaction liés à des stop-loss inutiles.

-

Combinaison avec la tendance et d'autres facteurs

Introduire des indicateurs de tendance comme les moyennes mobiles pour éviter de s'opposer fortement à la tendance ; ajouter d'autres facteurs auxiliaires.

Résumé

Le cœur de cette stratégie est d'utiliser les transactions de retournement pour capter les fortes fluctuations à court/moyen terme. L'approche est simple et directe, et un réglage des paramètres peut donner de bons résultats en conditions réelles. Cependant, la stratégie de retournement est agressive, avec un risque de drawdown et de piégeage. Il est nécessaire d'optimiser davantage les stratégies de stop-loss et de profit, et d'intégrer judicieusement le jugement de tendance pour réduire les pertes inutiles.

- 1