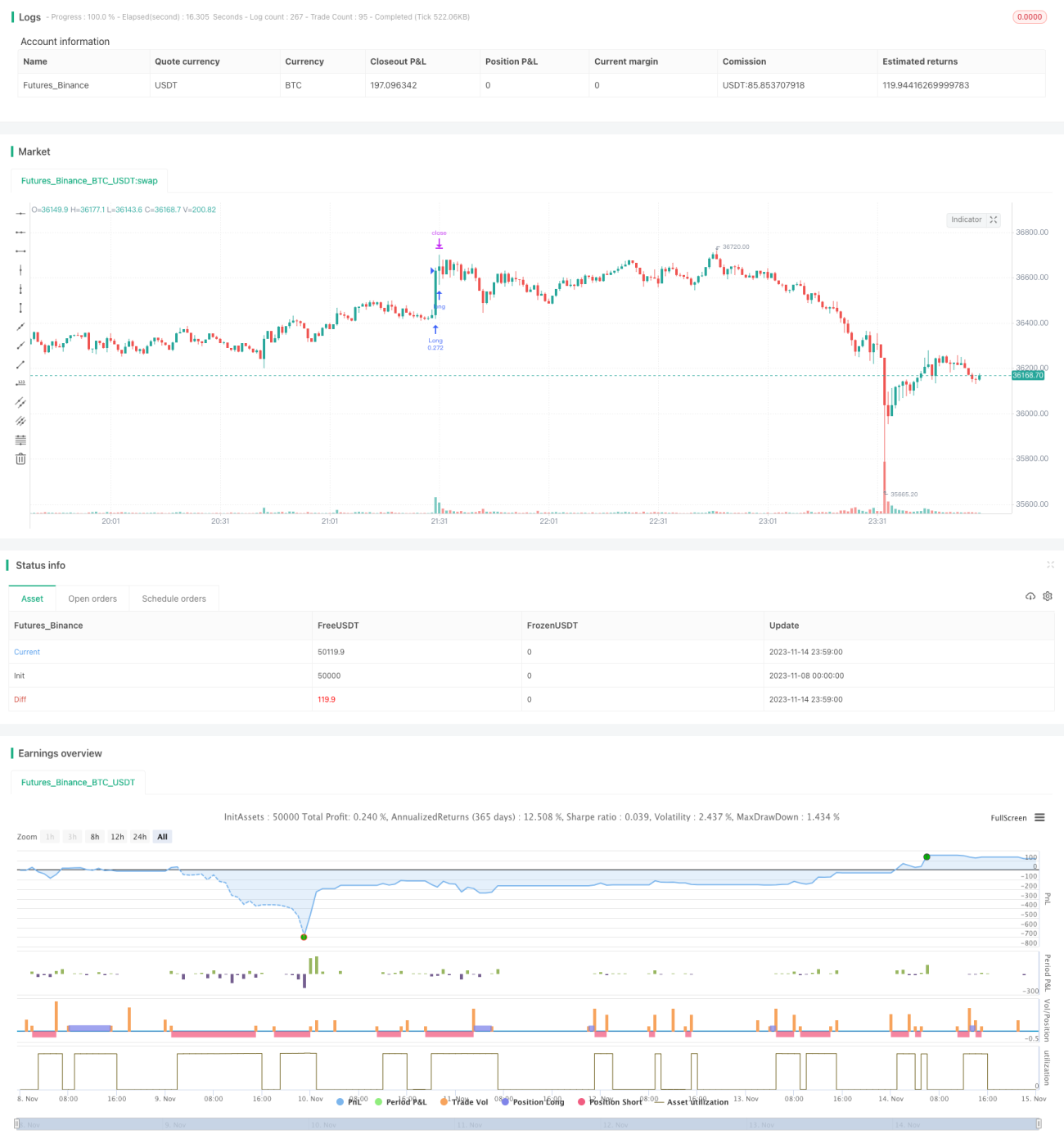

Stratégie de tendances multiples

Aperçu

Cette stratégie combine plusieurs indicateurs pour identifier la direction de la tendance, en utilisant une approche de suivi de tendance pour capturer les opportunités à moyen et court terme. La stratégie est spécialement conçue pour suivre la tendance, afin d'augmenter le taux de réussite et de réduire les baisses.

Principe de la stratégie

- Utilisation de l'indicateur WVAP pour évaluer le rapport de prix ;

- Indicateur RSI pour mesurer le momentum haussier/baissier ;

- Indicateur QQE pour identifier les cassures de prix ;

- Indicateur ADX pour évaluer la force de la tendance ;

- Coral Trend Indicator pour déterminer la tendance fondamentale ;

- Indicateur LSMA pour aider à juger la tendance ;

- Combinaison de signaux provenant de plusieurs indicateurs pour générer des signaux de trading.

Cette stratégie s'appuie principalement sur plusieurs indicateurs tels que RSI, QQE, ADX pour juger la direction et la force de la tendance, et utilise la courbe du Coral Trend Indicator comme critère de tendance fondamentale. Lorsque des indicateurs comme le RSI émettent un signal d'achat, si le Coral Trend Indicator montre également une courbe ascendante, la probabilité d'une tendance haussière est élevée et la stratégie choisit d'acheter. Les indicateurs comme WVAP servent principalement à évaluer si le prix est raisonnable et à éviter d'acheter à des sommets.

Avantages de la stratégie

- Combinaison de multiples indicateurs, améliorant la précision des jugements ;

- Accent mis sur le suivi de tendance, augmentant la probabilité de profit ;

- Approche par cassure, filtrant les marchés en range ;

- Intégration d'indicateurs fondamentaux, évitant les trades contraires à la tendance ;

- Réglages raisonnables du temps de trading et de la taille des positions, réduisant les risques ;

- Logique de stratégie claire, facile à comprendre et à optimiser.

Le principal avantage de cette stratégie est la combinaison de multiples indicateurs, ce qui permet de réduire dans une certaine mesure la probabilité d'erreur d'un seul indicateur et d'améliorer la précision des jugements. De plus, l'accent mis sur le suivi de tendance et l'approche par cassure aide à sélectionner des opportunités fiables à moyen et court terme. En outre, l'ajout d'indicateurs fondamentaux évite les opérations contraires à la tendance. Ces éléments améliorent la stabilité et la probabilité de profit de la stratégie.

Risques de la stratégie

- Les jugements haussiers/baissiers présentent un décalage temporel, ce qui peut faire manquer les meilleurs points d'entrée ;

- Le contrôle des baisses n'est pas parfait, ce qui expose à un risque de baisse important ;

- En cas de retournement fondamental, la stratégie peut manquer les signaux ;

- Les coûts de transaction ne sont pas pris en compte, ce qui peut entraîner une baisse des rendements en application réelle.

Le plus grand risque de cette stratégie réside dans le fait que la combinaison de multiples indicateurs peut entraîner un décalage temporel, faisant manquer le meilleur moment d'entrée et affectant ainsi la marge bénéficiaire. De plus, le contrôle des baisses n'est pas idéal, présentant un risque de baisse important. Lorsque les fondamentaux du marché se retournent avant que les indicateurs ne les reflètent, des pertes peuvent également survenir. En application réelle, les coûts de transaction auront également un certain impact sur les rendements.

Directions d'optimisation de la stratégie

- Ajout d'une stratégie de stop-loss pour optimiser le contrôle des baisses ;

- Optimisation des paramètres pour réduire le décalage des indicateurs ;

- Augmentation de l'utilisation des indicateurs fondamentaux pour améliorer la précision ;

- Intégration d'algorithmes d'apprentissage automatique pour une optimisation dynamique des paramètres.

L'optimisation de cette stratégie devrait se concentrer sur le contrôle des baisses, en ajoutant par exemple un stop-loss suiveur pour verrouiller les profits et réduire les baisses. On peut également optimiser les réglages de paramètres pour réduire le décalage des indicateurs et améliorer la sensibilité de la stratégie aux changements du marché. De plus, on peut ajouter davantage d'indicateurs de jugement fondamental pour améliorer la précision. Si l'on parvient à utiliser des méthodes d'apprentissage automatique pour une optimisation dynamique des paramètres, la stabilité de la stratégie sera également considérablement améliorée.

Résumé

Cette stratégie combine plusieurs indicateurs pour juger la direction de la tendance, en adoptant une approche de suivi de tendance conçue pour améliorer la précision des jugements et augmenter la probabilité de profit. La stratégie présente des avantages tels que la combinaison d'indicateurs, l'accent mis sur le suivi de tendance et l'intégration d'éléments fondamentaux, mais elle souffre également de problèmes comme le décalage dans les jugements et un contrôle insuffisant des baisses. À l'avenir, des améliorations pourront être apportées en optimisant les réglages des paramètres, en perfectionnant la stratégie de stop-loss, en ajoutant des indicateurs fondamentaux, etc., afin d'obtenir de meilleurs résultats en application réelle.

- 1