Stratégie d'indicateur technique des bandes de Bollinger basée sur la décomposition en séries temporelles et pondérée par le volume.

Aperçu

Cette stratégie combine quatre indicateurs techniques : la décomposition de séries temporelles, le prix moyen pondéré par le volume, les bandes de Bollinger et le delta (OBV-PVT), afin de réaliser une analyse multidimensionnelle de la tendance des prix et des conditions de surachat/survente.

Principe de la stratégie

- Utiliser la décomposition de séries temporelles pour éliminer le bruit et la cyclicité des prix, obtenant ainsi une évaluation plus précise de la tendance.

- Sur la base de cette ligne de tendance, calculer un nouveau prix pondéré par le volume.

- Calculer le pourcentage de largeur des bandes de Bollinger (BB%B) du cours de clôture pour déterminer les conditions de surachat/survente.

- Calculer la variation du delta (OBV-PVT) en pourcentage de largeur des bandes de Bollinger, comme critère de divergence entre le volume et le prix.

- Générer des signaux de trading en fonction du croisement haussier/baissier des indicateurs de volume et de prix, ainsi que des dépassements/retraits des bandes de Bollinger.

Analyse des avantages

- Combinaison de multiples jugements basés sur les prix, les volumes et les caractéristiques statistiques, offrant une robustesse élevée.

- La combinaison de BB%B et du delta (OBV-PVT) permet de mieux identifier les phénomènes de surachat/survente à court terme.

- Le croisement des signaux volume-prix filtre une partie des points de trading parasites.

Analyse des risques

- Les paramètres sont trop complexes et difficiles à ajuster.

- Une période de range étroit à court terme pourrait augmenter les pertes.

- La divergence volume-prix ne peut pas filtrer complètement les signaux trompeurs.

Il est possible d'optimiser la stratégie en ajustant les périodes des moyennes mobiles, la largeur des bandes de Bollinger et le ratio risque/rendement, afin de réduire la fréquence des transactions tout en améliorant le ratio gain/perte par transaction.

Résumé

Cette stratégie combine de manière synthétique plusieurs outils d'analyse : décomposition de séries temporelles, bandes de Bollinger, indicateur OBV, etc. L'intégration organique des relations volume-prix, des caractéristiques statistiques et de l'évaluation des tendances permet d'identifier les contrecoups à court terme tout en capturant efficacement la tendance principale du marché. Elle comporte également certains risques et nécessite des ajustements de paramètres pour atteindre des performances optimales.

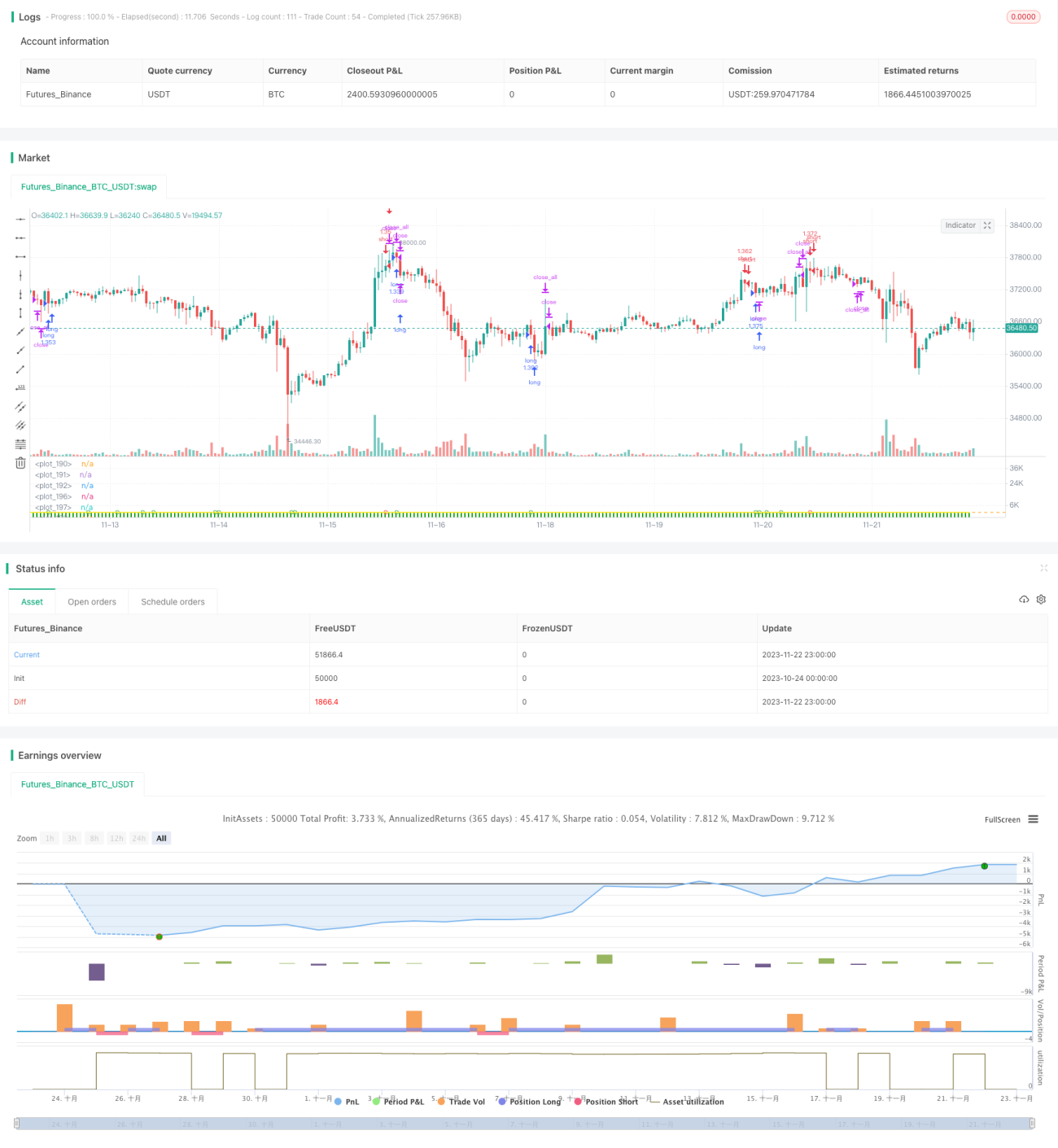

/*backtest

start: 2023-10-24 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © oakwhiz and tathal

- 1