Stratégie RSI-Bollinger Bands de capture de volatilité dynamique

Aperçu

La stratégie de capture dynamique d'amplitude avec RSI et bandes de Bollinger est une stratégie de trading qui intègre les concepts des bandes de Bollinger (BB), du Relative Strength Index (RSI) et de la moyenne mobile simple (SMA). Sa particularité réside dans le calcul d'un niveau dynamique basé sur la position du cours de clôture entre les bandes supérieure et inférieure. Cette fonctionnalité unique permet à la stratégie de s'adapter à la volatilité du marché et aux variations de prix.

Les marchés des cryptomonnaies et des actions sont très volatils, ce qui les rend particulièrement adaptés à l'utilisation des bandes de Bollinger. Le RSI aide à identifier les conditions de surachat et de survente sur ces marchés souvent spéculatifs.

Principe de la stratégie

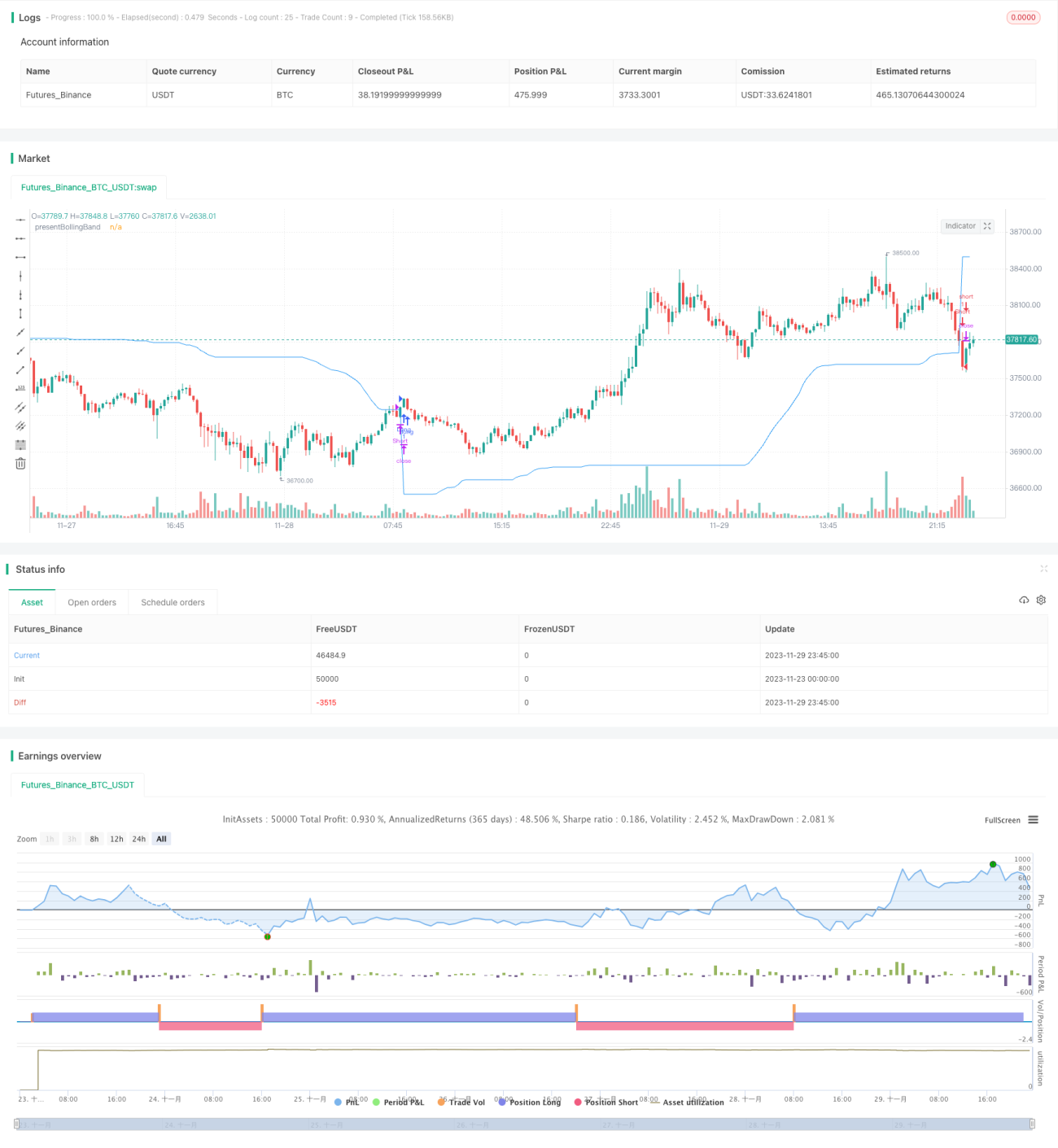

Bandes de Bollinger dynamiques : La stratégie calcule d'abord les bandes supérieure et inférieure de Bollinger en fonction d'une longueur et d'un multiplicateur définis par l'utilisateur. Elle combine ensuite les bandes de Bollinger et le cours de clôture pour ajuster dynamiquement la valeur de presentBollingBand. Enfin, un signal d'achat est généré lorsque le prix traverse la present BollingBand, et un signal de vente lorsqu'il la traverse dans l'autre sens.

RSI : Si l'utilisateur choisit d'utiliser le RSI pour générer des signaux, la stratégie calcule également le RSI et sa SMA, puis les utilise pour produire des signaux supplémentaires d'achat et de vente. Ces signaux basés sur le RSI ne sont utilisés que lorsque l'option "Utiliser le RSI pour générer des signaux" est définie sur true.

Ensuite, la stratégie vérifie la direction de trading sélectionnée et entre en position longue ou courte en conséquence. Si la direction de trading est définie sur "Bidirectionnel", la stratégie peut entrer à la fois en positions longues et courtes.

Enfin, la position longue est fermée lorsque le cours de clôture traverse la present BollingBand, et la position courte est fermée lorsque le cours de clôture la traverse dans le sens inverse.

Analyse des avantages

Cette stratégie combine les atouts des bandes de Bollinger, du RSI et de la SMA. Elle s'adapte à la volatilité du marché, capture dynamiquement les amplitudes et génère des signaux de trading en conditions de surachat/survente.

L'indicateur RSI complète les signaux des bandes de Bollinger, évitant les entrées erronées dans les marchés en range. Elle permet de choisir entre trading long uniquement, short uniquement, ou bidirectionnel, s'adaptant ainsi à différentes conditions de marché.

Les paramètres sont personnalisables, permettant un ajustement selon le profil de risque individuel.

Analyse des risques

La stratégie repose sur des indicateurs techniques et ne peut pas anticiper les retournements majeurs dus aux fondamentaux.

Un mauvais réglage des paramètres des bandes de Bollinger peut entraîner des signaux de trading trop fréquents ou trop rares.

Le trading bidirectionnel augmente le risque ; il faut être prudent face aux pertes potentielles en cas de vente à découvert.

Il est recommandé d'utiliser un stop-loss pour contrôler le risque.

Pistes d'optimisation

- Combiner avec d'autres indicateurs pour filtrer les signaux, par exemple le MACD.

- Ajouter une stratégie de stop-loss.

- Optimiser les paramètres des bandes de Bollinger et du RSI.

- Ajuster les paramètres en fonction des différents instruments et périodes de trading.

- Envisager une optimisation en conditions réelles, en ajustant les paramètres pour s'adapter à la réalité du marché.

Résumé

La stratégie de capture dynamique d'amplitude avec RSI et bandes de Bollinger est une stratégie pilotée par des indicateurs techniques. Elle combine les forces des bandes de Bollinger, du RSI et de la SMA pour capter la volatilité du marché via un ajustement dynamique des bandes. Cette stratégie offre une grande flexibilité de personnalisation et d'optimisation, mais ne peut pas prédire les changements fondamentaux. Il est recommandé de la valider en conditions réelles, et si nécessaire, d'ajuster les paramètres ou d'ajouter d'autres indicateurs pour réduire les risques.

- 1