Stratégie de trading multi-période de temps basée sur l'indicateur de volatilité et le stochastique

Aperçu

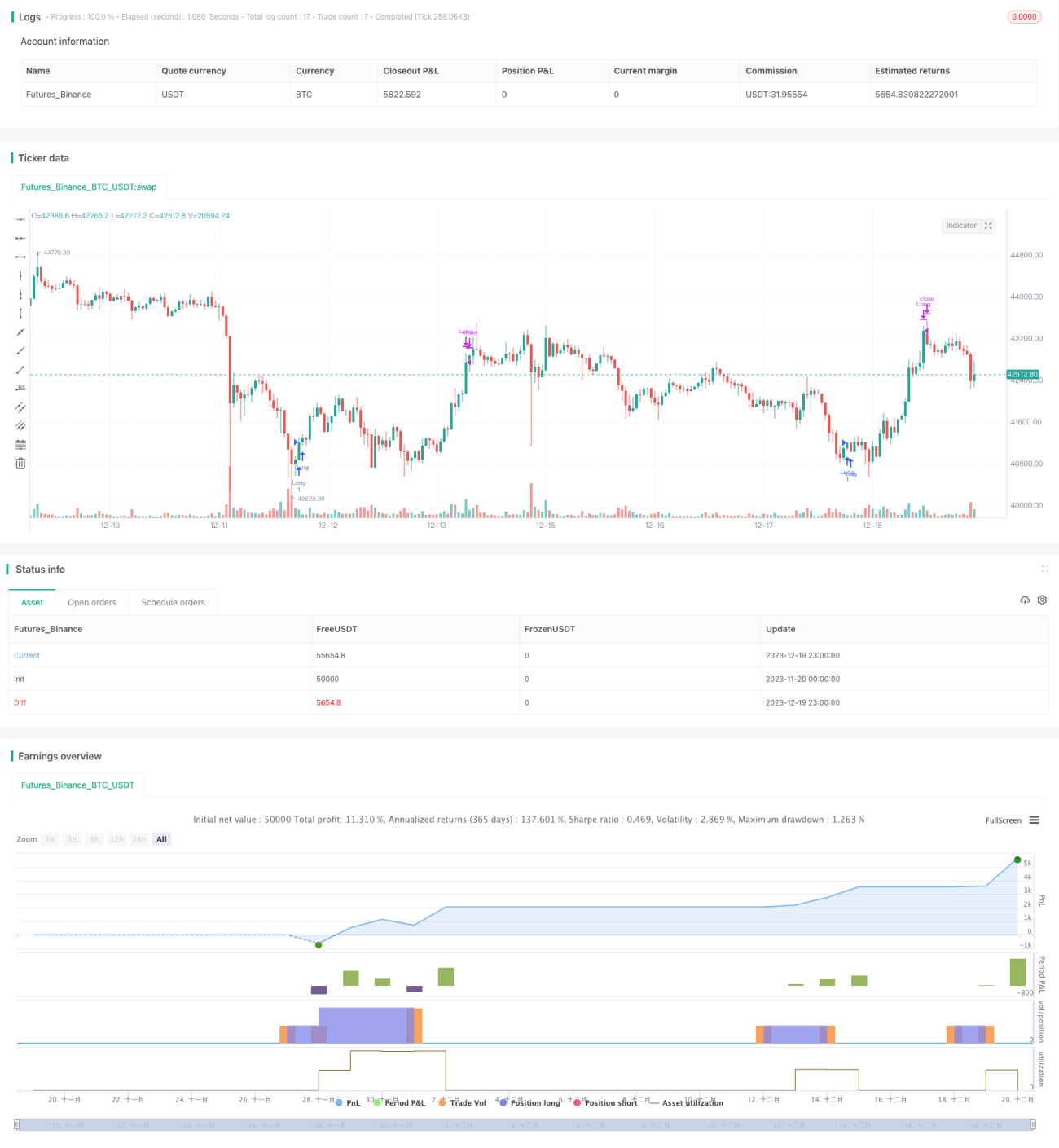

Cette stratégie combine l'indicateur de volatilité VIX et l'indicateur stochastique RSI. En utilisant une combinaison d'indicateurs sur différentes périodes, elle permet d'effectuer des entrées efficaces lors des cassures et de clôturer les positions en cas de surachat ou survente afin de limiter les pertes. La stratégie offre une grande marge d'optimisation et peut s'adapter à différents environnements de marché.

Principe de la stratégie

-

Calcul de l'indicateur de volatilité VIX : on calcule la volatilité en prenant le plus haut et le plus bas des 20 derniers jours. Lorsque la volatilité dépasse la bande supérieure, cela indique un sentiment de panique sur le marché ; lorsqu'elle passe en dessous de la bande inférieure, cela indique un sentiment de complaisance.

-

Calcul de l'indicateur stochastique RSI : on calcule les variations de prix sur les 14 derniers jours. Un RSI supérieur à 70 indique une zone de surachat, tandis qu'un RSI inférieur à 30 indique une zone de survente.

-

Combinaison des deux indicateurs : on prend une position longue lorsque la volatilité dépasse la bande supérieure ou le percentile le plus élevé ; on clôture la position lorsque le RSI dépasse 70.

Avantages de la stratégie

- Combinaison de multiples indicateurs pour une évaluation globale des points d'entrée sur le marché.

- Les indicateurs de différentes périodes se valident mutuellement, améliorant la précision des décisions.

- Paramètres ajustables pour s'adapter à différents instruments de trading.

Analyse des risques

- Un mauvais réglage des paramètres peut entraîner de nombreux faux signaux.

- Un unique indicateur de clôture peut manquer les retournements de prix.

Suggestions d'optimisation

- Ajouter davantage d'indicateurs de confirmation, comme les moyennes mobiles ou les bandes de Bollinger, pour déterminer les points d'entrée.

- Ajouter davantage d'indicateurs de clôture, comme les figures de chandeliers de retournement.

Résumé

Cette stratégie utilise l'indicateur VIX pour évaluer le timing et le niveau de risque du marché, combiné au RSI pour filtrer les points de trading défavorables liés au surachat et à la survente. Elle permet ainsi d'acheter à des moments efficaces et de limiter les pertes en temps utile. La stratégie offre une grande marge d'optimisation et peut s'adapter à un large éventail de conditions de marché.

- 1