Stratégie avancée de super tendance

Aperçu

La stratégie avancée de Supertrend est une optimisation et une amélioration de l'indicateur classique Supertrend. Elle combine l'action des prix, la volatilité et plusieurs indicateurs techniques afin d'améliorer la qualité des signaux, de réduire le bruit et de capturer plus précisément les changements de tendance du marché.

Principe de la stratégie

Le cœur de la stratégie avancée de Supertrend est la ligne de Supertrend. Celle-ci est calculée à partir de la plage de variation réelle et de la dynamique des prix, afin de déterminer les tendances et les points de retournement potentiels. Lorsque le prix se situe au-dessus de la ligne de Supertrend, cela indique une tendance haussière ; en dessous, une tendance baissière.

Contrairement à l'indicateur Supertrend classique qui ne tient compte que du cours de clôture et de la plage de variation réelle, la stratégie avancée intègre également plusieurs dimensions telles que le volume des transactions, l'oscillateur de momentum et les données fondamentales, afin de valider la fiabilité des signaux. Cette approche multivariée garantit que les signaux de trading générés sont plus précis et plus fiables, moins sensibles au bruit du marché.

Analyse des avantages

Les principaux avantages de la stratégie avancée de Supertrend sont les suivants :

-

Meilleure évaluation de la tendance du marché, filtrage des faux cassures. Cette stratégie attend que plusieurs facteurs et indicateurs soient en accord avant de générer un signal de trading, ce qui peut augmenter considérablement le taux de réussite.

-

Réduction des interférences du bruit du marché. En utilisant une combinaison de filtres, elle peut éliminer une grande partie des données de marché non pertinentes, rendant l'analyse plus claire.

-

Optimisation de la gestion des risques. Des signaux de trading clairs aident les traders à mieux planifier leurs niveaux de stop-loss et de take-profit, offrant ainsi un meilleur contrôle des risques.

-

Grande adaptabilité. En plus d'identifier les tendances, cette stratégie peut être combinée avec d'autres outils techniques pour construire un système de trading complet et efficace.

Analyse des risques

La stratégie avancée de Supertrend présente également les risques principaux suivants :

-

Risque de paramétrage. Une combinaison incorrecte des paramètres des indicateurs peut entraîner l'échec de la stratégie ou générer trop de signaux erronés.

-

Risque d'erreur de jugement de tendance. Aucune stratégie ne peut totalement éviter le risque d'erreur de jugement ; un changement inattendu de tendance peut entraîner des pertes.

-

Risque de suroptimisation. Ajuster les paramètres à un niveau trop précis rend la stratégie trop dépendante des données historiques et incapable de s'adapter aux changements du marché.

-

Risque de coûts de transaction. Lorsque le nombre de transactions augmente, les coûts de transaction comme les commissions et le slippage peuvent augmenter considérablement.

Solutions correspondantes :

-

Optimiser les réglages des paramètres et effectuer des backtests réguliers pour vérifier leur robustesse.

-

Mettre en place des stop-loss et take-profit pour contrôler les pertes par opération.

-

Éviter la suroptimisation et maintenir la capacité de généralisation des paramètres.

-

Calculer le ratio risque/rendement des signaux et contrôler les coûts de transaction.

Pistes d'optimisation

La stratégie avancée de Supertrend peut être optimisée dans les domaines suivants :

-

Adapter les paramètres en fonction des différents marchés pour mieux correspondre à leurs caractéristiques. Par exemple, sur un marché volatil, on peut réduire la période de calcul.

-

Ajouter un mécanisme de filtrage adaptatif. Lorsque le marché entre dans un état spécifique, ajuster automatiquement les paramètres des indicateurs ou désactiver certains filtres.

-

Explorer des méthodes d'apprentissage automatique, en utilisant des réseaux de neurones ou d'autres modèles pour optimiser dynamiquement les paramètres.

-

Intégrer des indicateurs de sentiment et des informations d'actualité, afin d'utiliser des données non structurées pour améliorer les performances.

-

Ajouter une fonction de dimensionnement de position ciblée. Lorsque le taux de réussite est élevé, il est possible d'augmenter la mise pour obtenir des gains plus élevés.

Conclusion

La stratégie avancée de Supertrend améliore et optimise l'indicateur classique Supertrend en introduisant plusieurs filtres et indicateurs de confirmation, permettant de mieux évaluer la tendance du marché et d'améliorer la qualité des signaux. Par rapport à un indicateur unique, cette stratégie offre une solution de trading plus robuste, plus complète et plus efficace. Cependant, il est nécessaire de se méfier des risques liés à un mauvais réglage des paramètres et à des erreurs de jugement, et de prendre des mesures de contrôle des risques appropriées. En poursuivant l'optimisation et en l'utilisant en conjonction avec d'autres outils, la stratégie avancée de Supertrend présente un fort potentiel d'application.

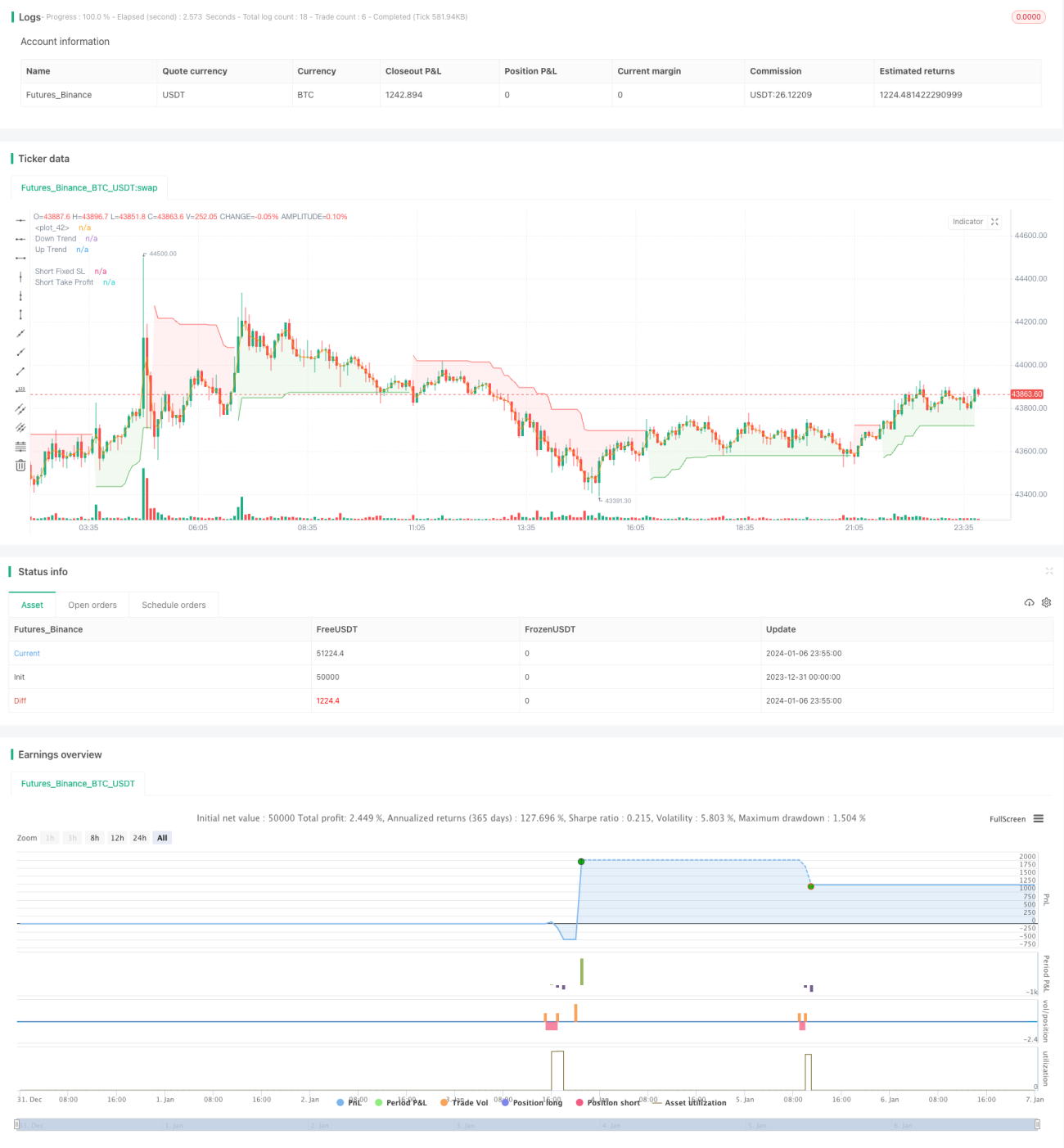

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © JS_TechTrading

//@version=5- 1