Stratégie de suivi de momentum avec filtre de plage adaptatif bidirectionnel

1

Follow

1802

Followers

Aperçu

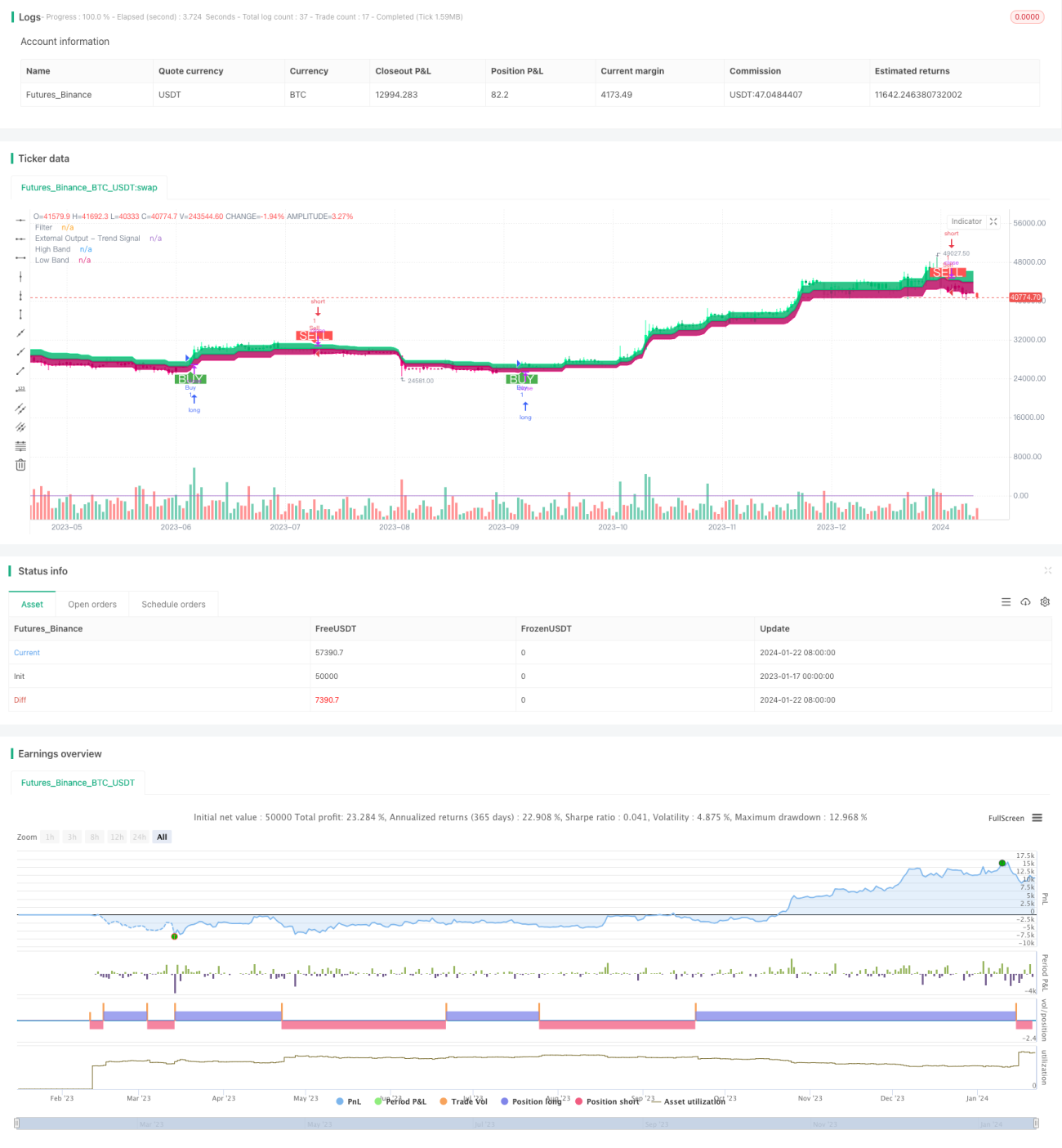

Cette stratégie est une stratégie de suivi de momentum à plage filtrée, adaptative et bidirectionnelle. Elle utilise un filtre de plage adaptatif pour suivre les fluctuations de prix et combine un indicateur de volume pour déterminer la direction de la valeur, permettant d'acheter bas et de vendre haut.

Principe de la stratégie

- Utiliser un filtre de plage adaptatif pour suivre les fluctuations de prix. La taille du filtre s'ajuste de manière adaptative en fonction de la période, du nombre et de l'échelle de la plage définis par l'utilisateur.

- Le filtre existe en deux types : Type 1 (suivi de plage standard) et Type 2 (arrondi par paliers).

- Déterminer la direction des fluctuations de prix en comparant la position du filtre par rapport au cours de clôture. Un prix au-dessus de la bande supérieure indique une tendance haussière, en dessous de la bande inférieure une tendance baissière.

- Combiner la variation du cours de clôture par rapport à la veille pour déterminer la direction de la valeur. Une hausse de la valeur indique une position longue, une baisse une position courte.

- Générer un signal d'achat lorsque le prix franchit la bande supérieure et que la valeur augmente ; générer un signal de vente lorsque le prix franchit la bande inférieure et que la valeur diminue.

Analyse des avantages

- Le filtre de plage adaptatif capture avec précision les fluctuations du marché.

- Les deux types de filtres répondent à différentes préférences de trading.

- La combinaison avec un indicateur de volume permet d'identifier efficacement la direction de la valeur.

- La stratégie est flexible et ses paramètres peuvent être ajustés en fonction du marché.

- Possibilité de personnaliser la logique des conditions de transaction.

Analyse des risques

- Un mauvais réglage des paramètres peut entraîner un surtrading ou des ordres manqués.

- Les signaux de franchissement présentent un certain retard.

- L'indicateur de volume peut présenter un risque de latence.

- Le franchissement de plage expose au risque d'être piégé.

Prévention des risques :

- Choisir une combinaison de paramètres appropriée et l'ajuster en temps utile.

- Combiner avec d'autres indicateurs pour identifier la tendance.

- Négocier prudemment près des niveaux clés et en cas de retournement de tendance.

Axes d'optimisation

- Tester différentes combinaisons de tailles de plage et de périodes de lissage pour trouver la combinaison optimale.

- Essayer différents types de filtres et choisir celui qui correspond à ses préférences.

- Expérimenter d'autres indicateurs de volume ou indicateurs techniques auxiliaires.

- Optimiser et ajuster la logique des conditions de transaction pour réduire les transactions irrationnelles.

- Intégrer la théorie fractale du marché pour définir une proportion de réallocation adaptative.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1