Nouvelle stratégie de trading quantitatif basée sur le motif ABCD avec trailing stop-loss et trailing take-profit.

I. Aperçu de la stratégie

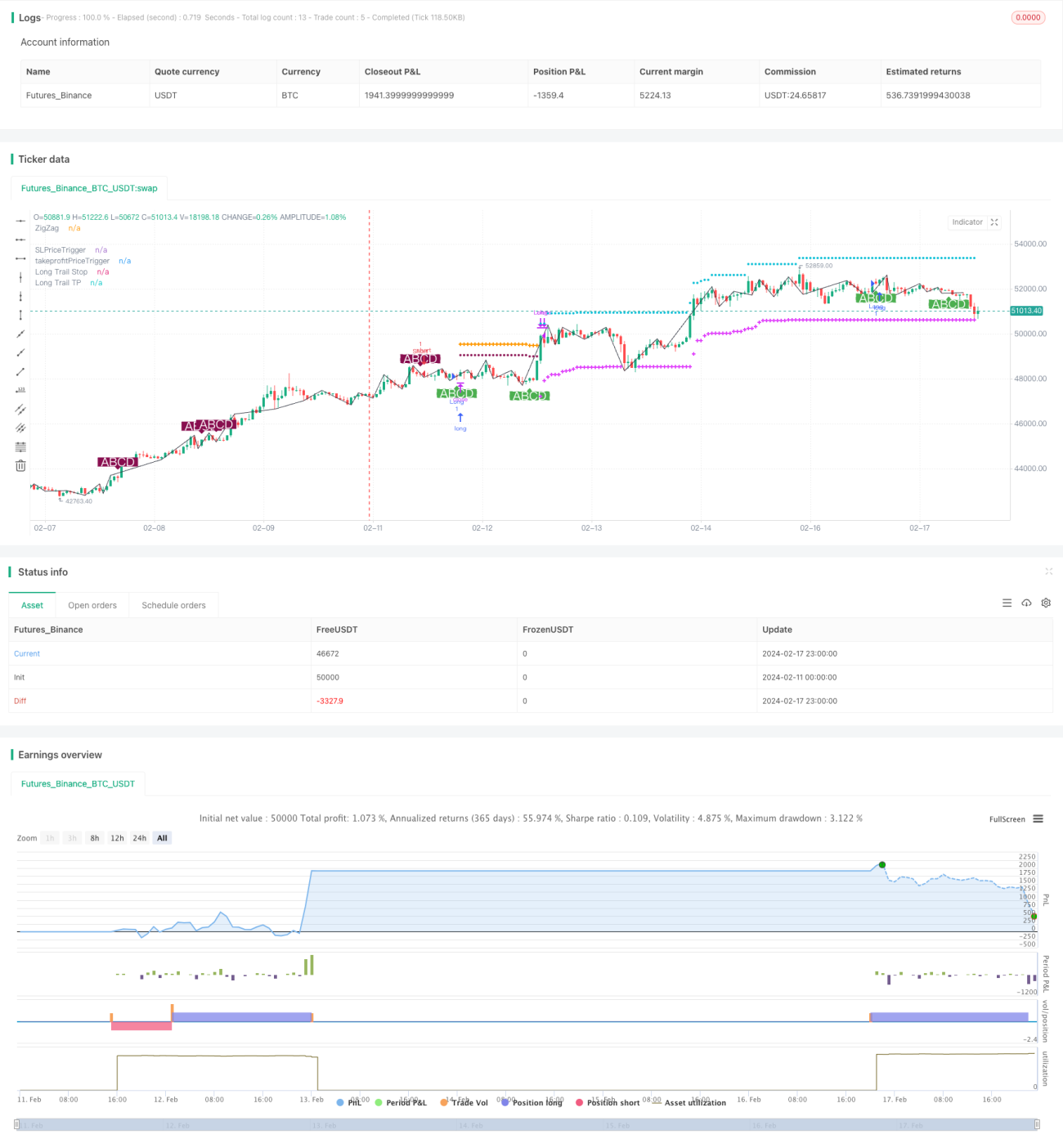

Cette stratégie est appelée « Stratégie de trading de la meilleure formation ABCD (avec trailing stop-loss et trailing take-profit) ». Il s'agit d'une stratégie quantitative qui effectue des opérations de trading basées sur un modèle clair de formation de prix ABCD. L'idée principale est d'identifier le modèle de formation ABCD complet, puis d'acheter ou de vendre à découvert selon la direction de la formation, et de mettre en place un trailing stop-loss et un trailing take-profit pour gérer les positions.

II. Principe de la stratégie

- Utiliser la méthode d'identification assistée par les bandes de Bollinger pour reconnaître les points de retournement du prix, obtenant ainsi la courbe ZigZag du prix.

- Sur la courbe ZigZag, identifier le modèle de formation ABCD complet. Les quatre points A, B, C, D doivent satisfaire certaines relations de proportion. Après avoir identifié une formation ABCD conforme, prendre une position longue ou courte.

- Après avoir pris une position longue ou courte, mettre en place un trailing stop-loss pour contrôler le risque. Le stop-loss commence par un stop-loss fixe, puis se transforme en trailing stop-loss lorsque le profit atteint un certain pourcentage, afin de verrouiller une partie des profits.

- De même, le take-profit est également configuré en trailing, pour prendre profit à temps après avoir obtenu un gain suffisant, évitant ainsi le retournement des profits. Le trailing take-profit se fait également en deux étapes : d'abord un take-profit fixe pour capter une partie des profits, puis un take-profit mobile pour continuer à suivre le prix.

- Lorsque le prix déclenche le trailing stop-loss ou le trailing take-profit, la position est fermée, complétant ainsi un cycle de trading.

III. Analyse des avantages de la stratégie

- L'utilisation de la méthode d'identification assistée par les bandes de Bollinger pour la courbe ZigZag évite le problème de rétrospection de la courbe ZigZag traditionnelle, rendant les signaux de trading plus fiables.

- Le modèle de trading de la formation ABCD est mature et stable, les opportunités de trading sont relativement abondantes. De plus, la direction de la formation ABCD est claire, ce qui facilite la détermination de la direction d'entrée.

- La mise en place d'un trailing stop-loss et take-profit en deux étapes permet de mieux contrôler les risques et d'obtenir des profits. Le trailing stop-loss et take-profit rend la stratégie plus flexible et adaptable.

- Les paramètres de la stratégie sont bien conçus : les pourcentages de stop-loss et take-profit, ainsi que le pourcentage de déclenchement du trailing, sont personnalisables, ce qui offre une grande flexibilité d'utilisation.

- Cette stratégie peut être utilisée sur n'importe quel instrument, y compris le forex, les crypto-monnaies et les indices boursiers.

IV. Analyse des risques de la stratégie

- Bien que la formation ABCD soit relativement claire, les opportunités de trading sont limitées et ne garantissent pas une fréquence de trading suffisante.

- Dans un marché en range, les stop-loss et take-profit peuvent être déclenchés fréquemment. Dans ce cas, il est nécessaire d'ajuster les paramètres en élargissant la plage de stop-loss et take-profit.

- Il faut prêter attention à la liquidité de l'instrument négocié. Sur les actifs à faible liquidité, l'exécution des stop-loss et take-profit peut être difficile.

- La stratégie est sensible aux coûts de transaction ; il faut choisir un courtier et un compte à faibles commissions.

- Certains paramètres peuvent être optimisés davantage, par exemple les conditions de déclenchement du trailing stop-loss et take-profit peuvent être testées avec plus de valeurs pour trouver le meilleur point.

V. Directions d'optimisation de la stratégie

- On peut combiner d'autres indicateurs et ajouter plus de filtres pour éviter certaines formations HW. Cela peut réduire l'apparition de transactions inefficaces.

- Ajouter un jugement sur la structure en trois phases du marché, en ne cherchant des opportunités de trading que dans la troisième phase. Cela peut améliorer le taux de réussite de la stratégie.

- Tester et optimiser la taille du capital initial pour trouver le meilleur niveau de capital de départ. Trop grand ou trop petit n'est pas favorable à l'obtention du meilleur taux de rendement.

- On peut tester des données hors échantillon pour vérifier la robustesse des paramètres. Ceci est essentiel pour comprendre la stabilité à moyen et long terme de la stratégie.

- Continuer à optimiser les conditions de déclenchement du trailing stop-loss/take-profit et la taille du slippage pour améliorer l'efficacité d'exécution de la stratégie. L'optimisation des paramètres est un processus sans fin.

VI. Résumé de la stratégie

Cette stratégie repose principalement sur la formation de prix ABCD pour le jugement et l'entrée. Elle met en place un trailing stop-loss et take-profit en deux étapes pour gérer les risques et les profits. La stratégie est relativement mature et stable, mais la fréquence de trading peut être faible. Nous pouvons obtenir des opportunités de trading plus efficaces en ajoutant des filtres. De plus, continuer à optimiser les paramètres et la taille du capital peut également améliorer la rentabilité stable de la stratégie. Dans l'ensemble, cette stratégie a une logique claire, facile à comprendre et à mettre en œuvre, et constitue une stratégie de trading quantitatif digne d'être étudiée et appliquée en profondeur.

- 1