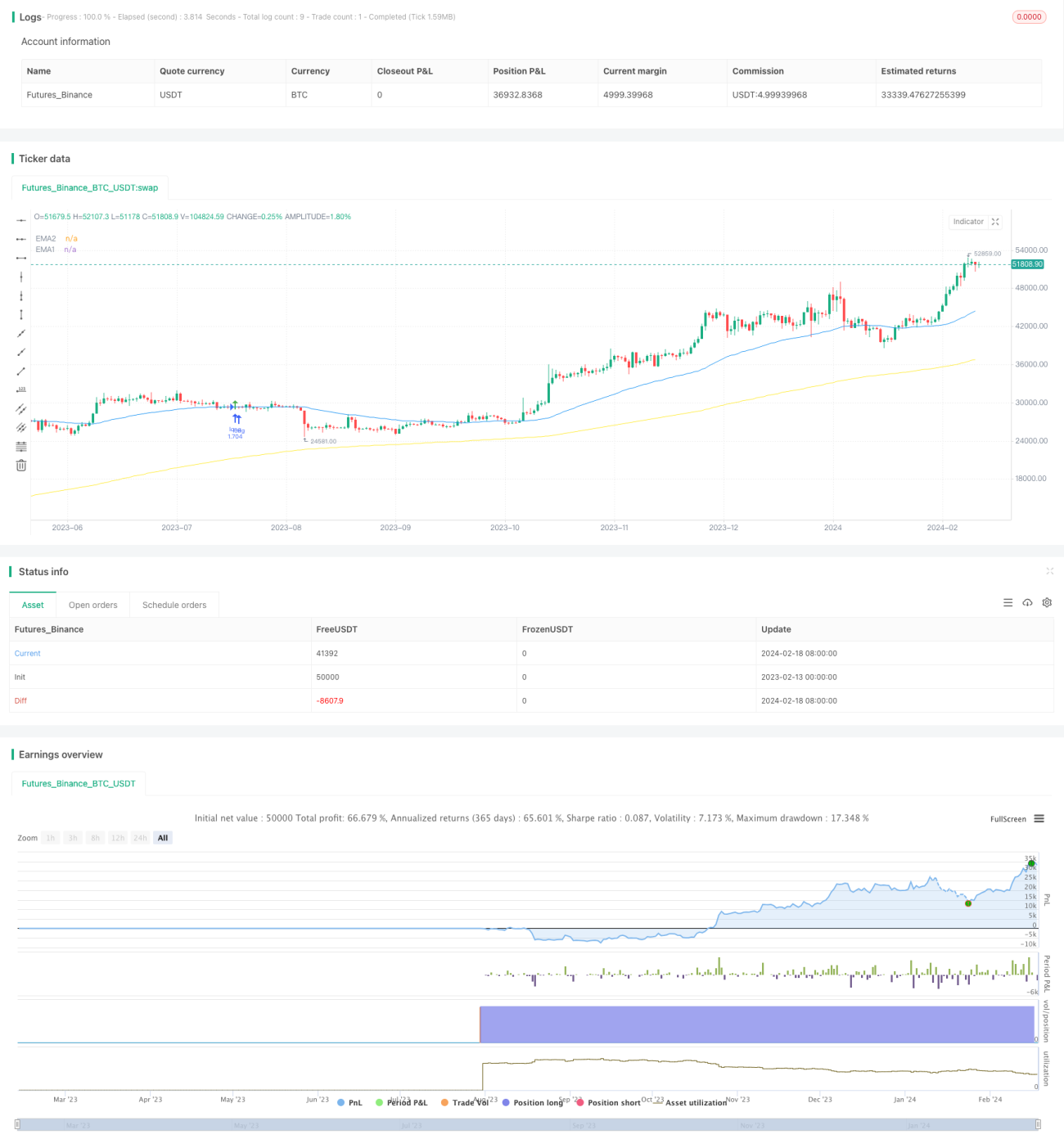

Stratégie de suivi de tendance basée sur le franchissement d'une combinaison d'indicateurs

Aperçu

Cette stratégie est intitulée « Stratégie de suivi de tendance par combinaison d'indicateurs ». Elle combine plusieurs indicateurs pour identifier la direction de la tendance du marché et effectuer des opérations de suivi de tendance. Elle comprend principalement les parties suivantes :

- Utilisation d'un indicateur de tendance ondulatoire pour déterminer la tendance principale du marché.

- Combinaison avec l'indicateur RSI et l'indicateur de flux de capitaux pour filtrer une partie des faux signaux.

- Utilisation de l'indicateur EMA pour déterminer la direction opérationnelle spécifique.

- Entrée en position par une méthode de rupture de suivi, garantissant le suivi de la tendance.

Principe de la stratégie

Cette stratégie détermine principalement la direction et la force de la grande tendance, et met en place des transactions bidirectionnelles (achat et vente). Le principe de fonctionnement spécifique est le suivant :

Signal d'entrée en position longue :

- Le prix est supérieur à l'EMA 200 jours, indiquant un marché haussier.

- Le prix effectue un repli près de l'EMA 50 jours, formant un support.

- L'indicateur ondulatoire s'inverse en tendance haussière et émet un signal d'achat.

- Le RSI et le MFI indiquent tous deux une zone de surachat.

- Trois bougies consécutives franchissent successivement l'EMA 50 jours, signalant une cassure à la hausse.

Signal d'entrée en position courte :

À l'inverse du signal d'entrée en position longue.

Méthode de prise de bénéfices et de stop-loss :

Deux options disponibles : stop-loss sur le plus bas/plus haut, stop-loss basé sur l'ATR.

Analyse des avantages de la stratégie

Cette stratégie présente les avantages suivants :

- Combinaison de multiples indicateurs pour déterminer la grande tendance, évitant les faux cassages.

- Utilisation de l'EMA pour déterminer la direction opérationnelle, facilitant le suivi de la tendance.

- Méthode de stop-loss suiveur permettant de réaliser des profits continus.

- Possibilité d'acheter et de vendre simultanément, suivant le marché dans n'importe quelle direction.

Analyse des risques de la stratégie

Cette stratégie comporte également certains risques :

- Probabilité que les indicateurs émettent des signaux erronés.

- Un stop-loss trop serré augmente le risque d'être stoppé.

- Un nombre élevé de transactions, les frais de transaction représentant une perte cachée.

Pour réduire ces risques, plusieurs axes d'optimisation peuvent être envisagés :

- Ajuster les paramètres des indicateurs pour filtrer les signaux erronés.

- Élargir modérément les niveaux de stop-loss.

- Optimiser les paramètres des indicateurs pour réduire le nombre de transactions.

Pistes d'optimisation de la stratégie

Du point de vue du code, les principales pistes d'optimisation de cette stratégie sont les suivantes :

- Ajuster les paramètres de l'indicateur ondulatoire, du RSI et du MFI pour trouver la meilleure combinaison de paramètres.

- Tester la performance de différentes périodes d'EMA.

- Ajuster le ratio risque/récompense pour la prise de bénéfices et le stop-loss afin d'obtenir la configuration optimale.

Grâce à l'ajustement et aux tests des paramètres, la stratégie peut maximiser les rendements tout en réduisant le drawdown et le risque.

Conclusion

Cette stratégie combine plusieurs indicateurs pour déterminer la direction de la grande tendance, utilise l'EMA comme signal opérationnel spécifique et emploie un stop-loss suiveur pour verrouiller les profits. Grâce à l'optimisation des paramètres, elle peut générer des rendements stables satisfaisants. Il convient toutefois d'être conscient des risques inhérents au système et de surveiller en permanence l'efficacité des indicateurs ainsi que les évolutions des conditions de marché.

- 1