Stratégie de trading en grille adaptative basée sur une plateforme de trading quantitatif

Aperçu

Cette stratégie est une stratégie de trading en grille adaptative basée sur une plateforme de trading quantitatif. Elle consiste à définir une plage de trading en grille, manuellement ou automatiquement, puis à placer des ordres d'achat et de vente à intervalles réguliers à l'intérieur de cette plage. Lorsque le prix franchit les limites supérieure ou inférieure de la grille, la stratégie ajuste automatiquement la plage.

Principe de la stratégie

-

Définir les prix limites supérieur et inférieur de la grille. Il est possible de calculer automatiquement les points hauts et bas historiques sur une période donnée pour servir de limites, ou de définir manuellement des limites fixes.

-

Calculer l'écart de prix entre chaque grille en fonction des prix limites et du nombre de grilles.

-

Entre les prix limites, disposer plusieurs points d'achat/vente à intervalles égaux pour former la grille.

-

Lorsque le prix du marché franchit la limite inférieure de la grille, placer un ordre d'achat sur la grille suivante après la grille où se trouve le dernier ordre ouvert ; lorsque le prix franchit la limite supérieure, placer un ordre de vente sur la grille précédente.

-

Ainsi, des opérations d'achat et de vente sont effectuées en continu entre les limites de la grille. Lorsque la tendance des prix s'inverse, les ordres précédents sont progressivement clôturés en prenant profit ou en limitant les pertes.

Avantages de la stratégie

-

Le trading en grille permet de générer des profits dans des marchés latéraux ou oscillants.

-

L'ajustement adaptatif de la plage de grille s'effectue automatiquement en fonction de la volatilité du marché, sans intervention humaine.

-

Il est possible de prédéfinir un montant de capital investi, réparti proportionnellement sur chaque grille, pour contrôler le risque par ordre.

-

Logique simple, facile à comprendre et paramètres ajustables avec flexibilité.

Risques et contre‑mesures

-

Pertes dues au franchissement des limites

- Solution : définir correctement le niveau du stop‑loss.

-

Pertes répétées en situation de tendance

- Solution : identifier la tendance et suspendre temporairement le trading.

-

Mauvais réglage des paramètres

- Solution : ajuster le nombre de grilles et l'écart de prix.

Pistes d'optimisation

-

Utiliser l'apprentissage automatique pour prédire l'amplitude des fluctuations et la tendance des prix, et ajuster dynamiquement les paramètres de la grille.

-

En marché tendanciel, adopter une stratégie de suivi de tendance pour éviter les pertes liées au trading en grille.

-

Intégrer des indicateurs tels que le taux d'utilisation du capital et le rendement pour le contrôle des risques.

-

Étendre à plusieurs instruments pour diversifier l'utilisation des capitaux.

Conclusion

Cette stratégie est une stratégie de grille adaptative avec paramètres auto‑ajustables, adaptée aux actions, crypto‑monnaies et devises en phase de consolidation ou d'oscillation. En ajustant les paramètres, elle peut s'adapter à différentes conditions de marché et possède une certaine valeur pratique.

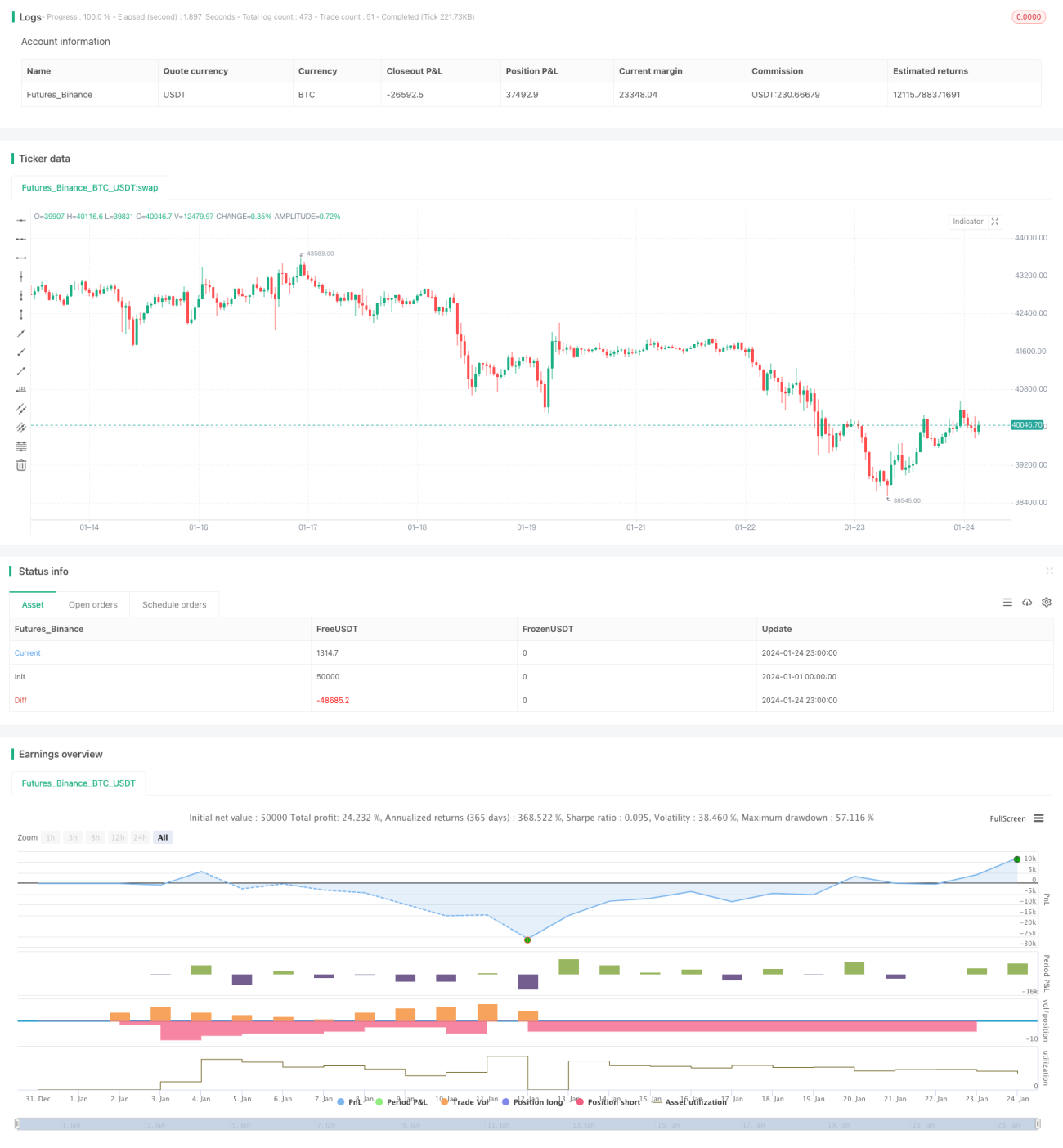

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-24 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//hk4jerry

strategy("Grid Bot Backtesting", overlay=false, pyramiding=3000, close_entries_rule="ANY", default_qty_type=strategy.cash, initial_capital=100.0, currency="USD", commission_type=strategy.commission.percent, commission_value=0.025)- 1