सामान्यीकृत समर्थन/प्रतिरोध पर आधारित प्रतिवर्ती व्यापार रणनीति

सारांश

यह रणनीति संकेतक के बुलिश/बेयरिश कारकों पर आधारित रिवर्सल ट्रेडिंग का उपयोग करती है, साथ ही लाभ लक्ष्य भी निर्धारित करती है। बुलिश/बेयरिश कारक का मूल वॉल्यूम-आधारित विस्तारित रूप "व्यापक समर्थन/प्रतिरोध" है, जो उच्च ट्रेडिंग वॉल्यूम और अस्थिरता वाले उपकरणों के लिए उपयुक्त है। रणनीति का लाभ यह है कि यह मध्यम से अल्पकालिक बड़े ट्रेंड रिवर्सल अवसरों को पकड़ सकती है और तेजी से लाभ कमा सकती है; हालांकि, इसमें फंसने का जोखिम भी है।

रणनीति सिद्धांत

-

वॉल्यूम-आधारित "व्यापक समर्थन/प्रतिरोध" से बुलिश/बेयरिश कारकों की पहचान

-

कैंडलस्टिक पैटर्न का उपयोग करके शास्त्रीय समर्थन/प्रतिरोध की पहचान, उच्च वॉल्यूम से झूठे ब्रेकआउट को फ़िल्टर करना

-

व्यापक समर्थन/प्रतिरोध शास्त्रीय पैटर्न की तुलना में अधिक समावेशी है

-

व्यापक समर्थन का ब्रेकआउट बुलिश कारक संकेत है, व्यापक प्रतिरोध का ब्रेकआउट बेयरिश कारक संकेत है

-

-

रिवर्सल ट्रेडिंग

-

कारक संकेत जारी होने के बाद, विपरीत कार्रवाई की जाती है

-

यदि पहले से कोई स्थिति है, तो विपरीत दिशा में स्थिति कम की जाती है या नई स्थिति खोली जाती है

-

-

लाभ लक्ष्य निर्धारण

-

ATR के आधार पर स्टॉप-लॉस सेट करना

-

1R/2R/3R जैसे कई लाभ लक्ष्य निर्धारित करना

-

विभिन्न लाभ लक्ष्यों तक पहुंचने पर चरणबद्ध तरीके से स्थिति कम करना

-

लाभ विश्लेषण

-

मध्यम से अल्पकालिक बड़े रिवर्सल को पकड़ सकता है

समर्थन/प्रतिरोध का ब्रेकआउट एक मजबूत ट्रेंड रिवर्सल संकेत है, जिसमें एक निश्चित विश्वसनीयता होती है और यह मध्यम से अल्पकालिक बड़े रिवर्सल को पकड़ सकता है।

-

तेजी से लाभ, कम ड्रॉडाउन

स्टॉप-लॉस और कई लाभ लक्ष्यों के माध्यम से तेजी से लाभ प्राप्त किया जा सकता है और व्यक्तिगत स्टॉक के ड्रॉडाउन को सीमित किया जा सकता है।

-

बड़ी संस्थागत पूंजी और उच्च अस्थिरता वाले उपकरणों के लिए उपयुक्त

यह रणनीति वॉल्यूम संकेतकों पर निर्भर करती है, इसलिए ट्रेंड को समर्थन देने के लिए पर्याप्त संस्थागत पूंजी प्रवाह की आवश्यकता होती है; साथ ही लाभ के लिए कुछ अस्थिरता स्थान की आवश्यकता होती है।

जोखिम विश्लेषण

-

साइडवेज़ बाजार में फंसने का जोखिम

जब बाजार साइडवेज़ होता है, तो स्टॉप-लॉस से बाहर निकलने और फिर विपरीत दिशा में प्रवेश करने से बार-बार फंसने की स्थिति हो सकती है।

-

समर्थन/प्रतिरोध विफलता का जोखिम

व्यापक समर्थन/प्रतिरोध पूरी तरह से विश्वसनीय नहीं है, इसमें असफल परीक्षण और रिवर्सल की संभावना है।

-

एकतरफा स्थिति का जोखिम

रणनीति विशुद्ध रूप से रिवर्सल है, ट्रेंड फॉलोइंग पर विचार नहीं करती, जिससे बड़े दिशात्मक अवसर छूट सकते हैं।

-

जोखिम प्रबंधन पक्ष

-

रिवर्सल ट्रेडिंग के कारक शर्तों को थोड़ा ढीला किया जा सकता है, हर ब्रेकआउट पर रिवर्सल की आवश्यकता नहीं

-

अन्य संकेतकों जैसे वॉल्यूम-प्राइस डायवर्जेंस के साथ फ़िल्टर किया जा सकता है

-

फंसने की संभावना कम करने के लिए स्टॉप-लॉस रणनीति को अनुकूलित किया जा सकता है

-

अनुकूलन दिशाएँ

-

पैरामीटर ऑप्टिमाइज़ेशन

अधिक विश्वसनीय कारकों की पहचान के लिए व्यापक समर्थन/प्रतिरोध के पैरामीटर ऑप्टिमाइज़ करना

-

लाभ रणनीति ऑप्टिमाइज़ेशन

अधिक लाभ लक्ष्य स्तर जोड़े जा सकते हैं, या गैर-निश्चित लाभ लक्ष्य का उपयोग किया जा सकता है

-

स्टॉप-लॉस रणनीति ऑप्टिमाइज़ेशन

ATR पैरामीटर समायोजित करना या अनावश्यक आक्रामक स्टॉप-लॉस से होने वाली ट्रेडिंग लागत को कम करने के लिए चतुर स्टॉप-लॉस का उपयोग करना

-

ट्रेंड और अन्य कारकों का संयोजन

ट्रेंड से गंभीर विरोध से बचने के लिए मूविंग एवरेज जैसे ट्रेंड निर्णय शामिल किए जा सकते हैं; अन्य सहायक कारक भी जोड़े जा सकते हैं

निष्कर्ष

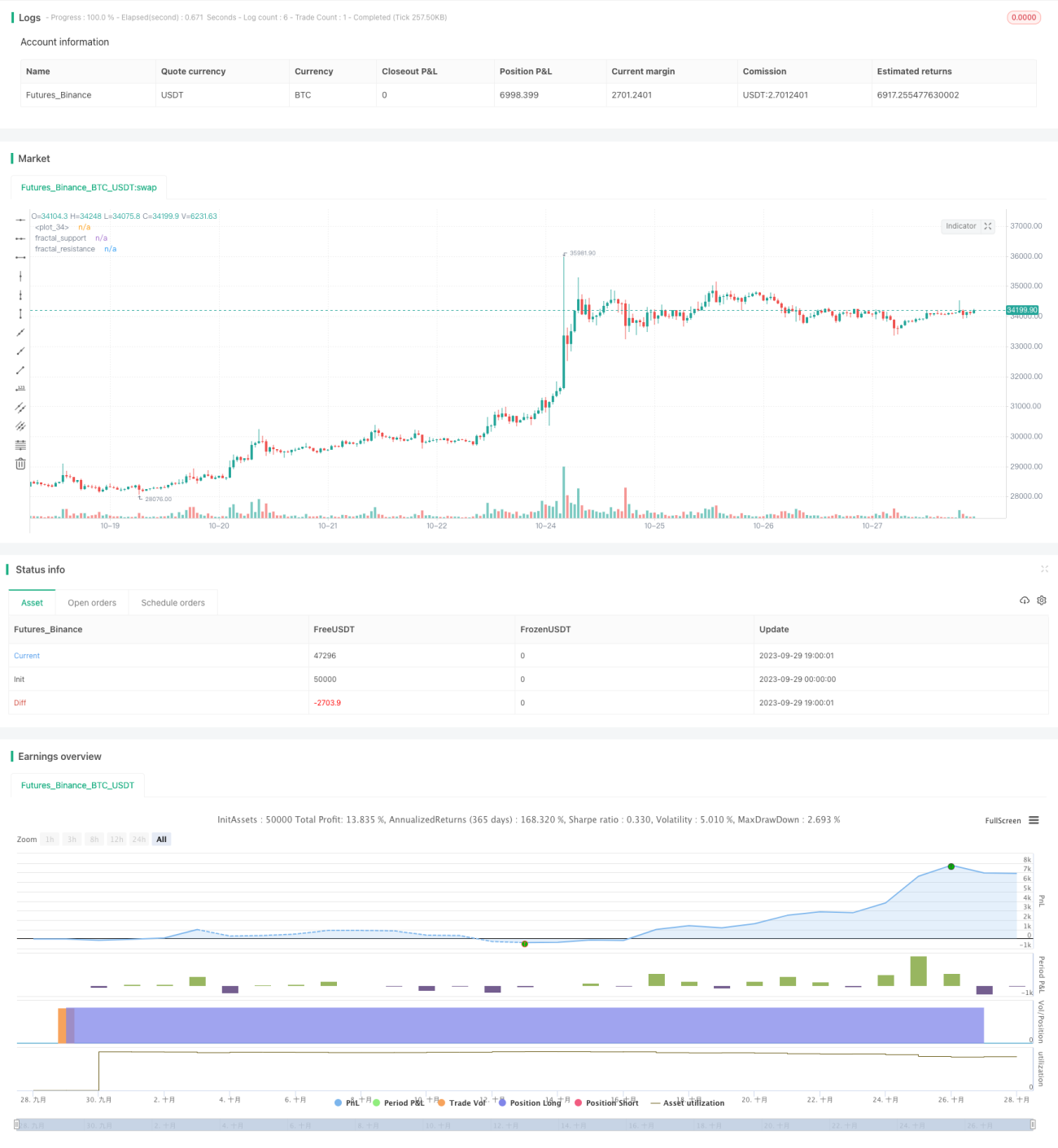

इस रणनीति का मूल रिवर्सल ट्रेडिंग के माध्यम से मध्यम से अल्पकालिक बड़ी अस्थिरता को पकड़ना है। रणनीति सरल और सीधी है, पैरामीटर समायोजन के माध्यम से अच्छे वास्तविक बाजार परिणाम प्राप्त किए जा सकते हैं। हालांकि, रिवर्सल रणनीति आक्रामक है, इसमें कुछ ड्रॉडाउन और फंसने का जोखिम है, इसलिए स्टॉप-लॉस और लाभ रणनीति को और अनुकूलित करने और अनावश्यक नुकसान को कम करने के लिए उचित रूप से ट्रेंड निर्णय को शामिल करने की आवश्यकता है।

- 1