मूविंग एवरेज पर आधारित ट्रेंड फॉलोइंग रणनीति

अवलोकन

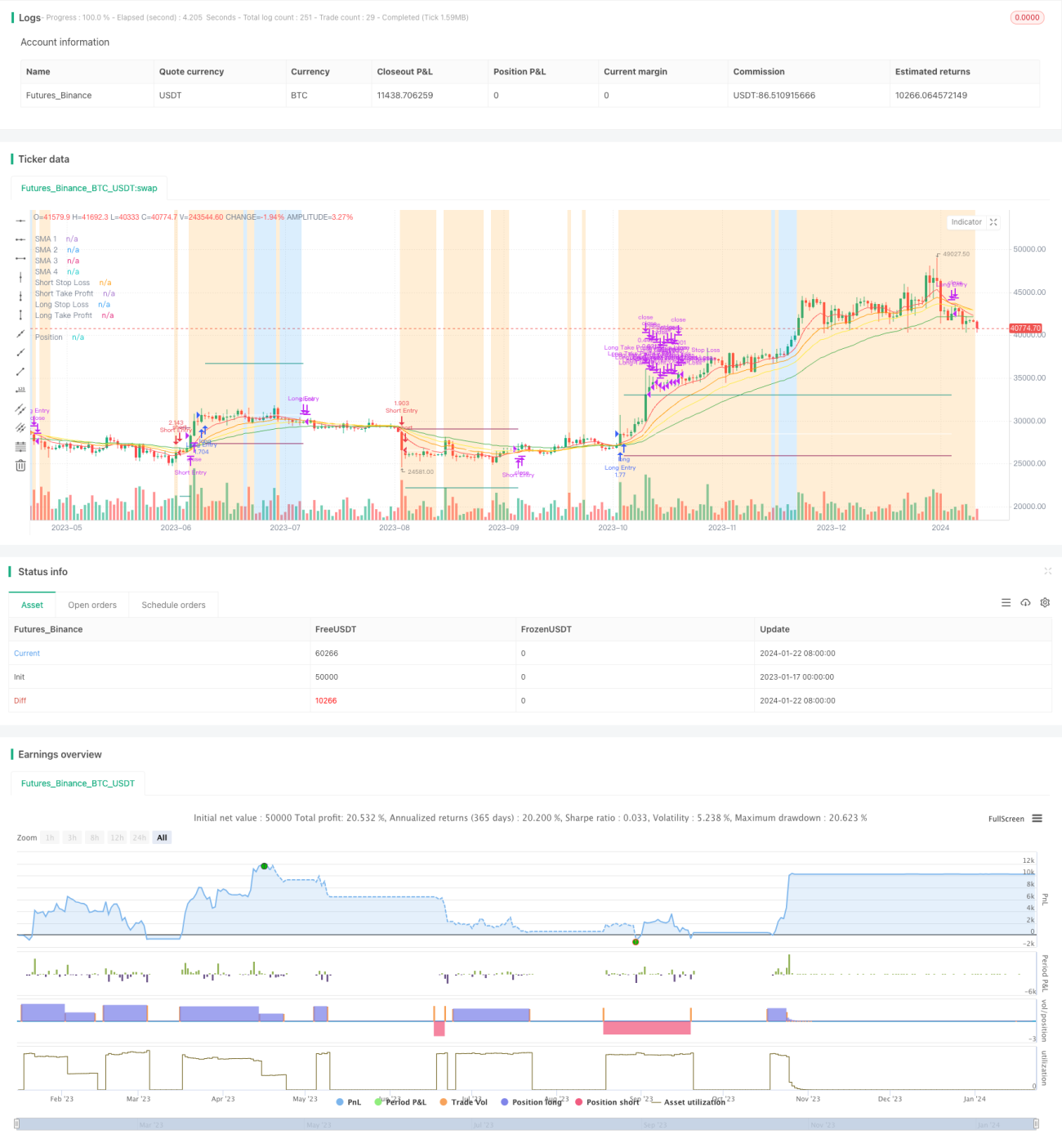

यह रणनीति मूविंग एवरेज पर आधारित एक सरल ट्रेंड फॉलोइंग रणनीति है। यह विभिन्न अवधियों के मूविंग एवरेज के आकार संबंधों की तुलना करके वर्तमान ट्रेंड की दिशा और ट्रेंड की अवधि निर्धारित करती है। जब छोटी अवधि का मूविंग एवरेज नीचे से ऊपर की ओर लंबी अवधि के मूविंग एवरेज को पार करता है, तो लॉन्ग पोजीशन ली जाती है, और जब छोटी अवधि का मूविंग एवरेज ऊपर से नीचे की ओर लंबी अवधि के मूविंग एवरेज को पार करता है, तो शॉर्ट पोजीशन ली जाती है। साथ ही, रणनीति में जोखिम नियंत्रण के लिए स्टॉप लॉस और टेक प्रॉफिट स्तर निर्धारित किए गए हैं।

रणनीति का सिद्धांत

यह रणनीति चार अलग-अलग अवधियों के मूविंग एवरेज का उपयोग करती है: 5-दिवसीय, 10-दिवसीय, 15-दिवसीय और 25-दिवसीय। इन चार मूविंग एवरेज को MA1, MA2, MA3 और MA4 कहा जाता है। इनमें MA1 सबसे छोटी अवधि का है और MA4 सबसे लंबी अवधि का है।

जब MA1 > MA2 > MA3 > MA4 होता है, तो यह संकेत मिलता है कि कीमत बढ़ती प्रवृत्ति में है, तब लॉन्ग पोजीशन ली जाती है; जब MA1 < MA2 < MA3 < MA4 होता है, तो यह संकेत मिलता है कि कीमत घटती प्रवृत्ति में है, तब शॉर्ट पोजीशन ली जाती है।

लॉन्ग और शॉर्ट पोजीशन खोलने की शर्तों को ATR स्टॉप फिल्टर को भी पूरा करना होता है, अर्थात ATR मान ATR के 40-अवधि के सरल मूविंग एवरेज से अधिक होना चाहिए, जिससे कीमत में बहुत कम उतार-चढ़ाव होने पर गलत संकेत से बचा जा सके।

रणनीति के लाभ

इस रणनीति के निम्नलिखित लाभ हैं:

- सिद्धांत सरल और समझने में आसान है, क्रियान्वयन सरल है।

- कई मूविंग एवरेज का उपयोग करके ट्रेंड की दिशा निर्धारित करना विश्वसनीय है।

- स्टॉप लॉस और टेक प्रॉफिट स्तर निर्धारित करने से एकल ट्रेड में अधिकतम हानि को प्रभावी ढंग से नियंत्रित किया जा सकता है।

- ATR स्टॉप फिल्टर कीमत में बहुत कम उतार-चढ़ाव होने पर गलत संकेत से बचाता है।

जोखिम विश्लेषण

इस रणनीति में निम्नलिखित जोखिम भी हैं:

- अत्यधिक उतार-चढ़ाव वाले बाजार में गलत संकेत उत्पन्न होने की संभावना है।

- पैरामीटर सेटिंग्स (मूविंग एवरेज अवधि आदि) अनुपयुक्त होने पर रणनीति का प्रदर्शन खराब हो सकता है।

- मौलिक कारकों और महत्वपूर्ण समाचारों के मूल्य पर प्रभाव पर विचार नहीं किया गया है।

इन जोखिमों को कम करने के लिए, पैरामीटर को उपयुक्त रूप से अनुकूलित किया जा सकता है, या रणनीति की स्थिरता बढ़ाने के लिए अन्य फिल्टर शर्तें जोड़ी जा सकती हैं।

अनुकूलन की दिशाएँ

इस रणनीति के अनुकूलन की दिशाएँ निम्नलिखित हैं:

- विभिन्न मूविंग एवरेज अवधि पैरामीटर संयोजन का परीक्षण करके सर्वोत्तम पैरामीटर खोजना।

- अन्य तकनीकी संकेतक फिल्टर जैसे MACD, KDJ आदि जोड़कर संकेतों की विश्वसनीयता निर्धारित करना।

- ट्रेडिंग वॉल्यूम फिल्टर जोड़ना, केवल तभी ट्रेड करना जब ट्रेडिंग वॉल्यूम बढ़ा हो।

- विभिन्न उपकरणों के पैरामीटर अंतर के अनुसार बारीकी से उपकरण-वार पैरामीटर अनुकूलन करना।

- संकेत निर्धारण के लिए मशीन लर्निंग एल्गोरिदम जोड़ना।

सारांश

कुल मिलाकर यह रणनीति एक सरल ट्रेंड फॉलोइंग रणनीति है, जो मूविंग एवरेज के माध्यम से ट्रेंड की दिशा निर्धारित करती है और जोखिम स्तर को नियंत्रित करने के लिए उपयुक्त स्टॉप लॉस और टेक प्रॉफिट निर्धारित करती है। रणनीति में अनुकूलन की काफी गुंजाइश है, पैरामीटर समायोजन, फिल्टर जोड़ने आदि के माध्यम से रणनीति की स्थिरता और लाभप्रदता को और बढ़ाया जा सकता है।

- 1