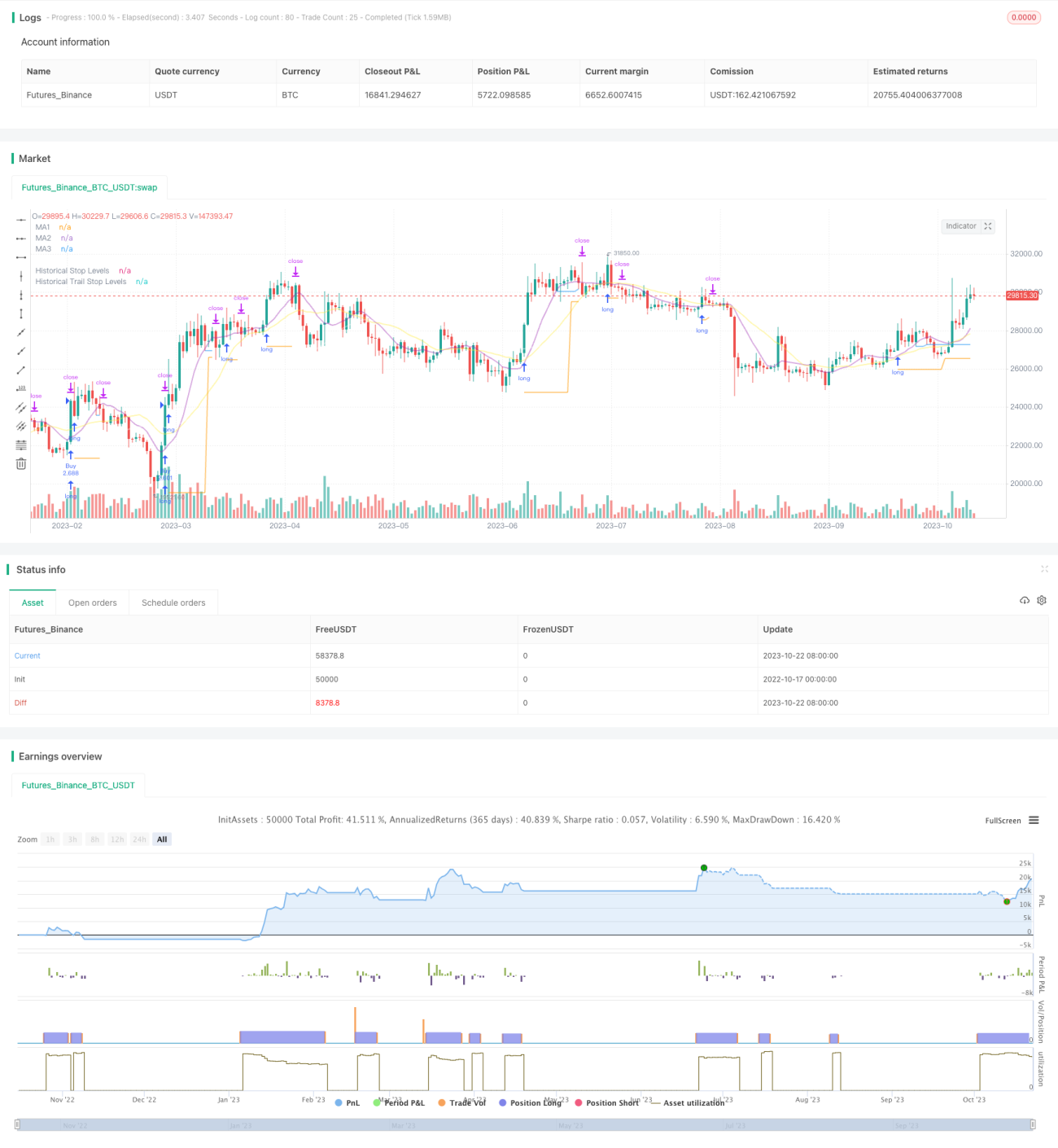

Strategi Trailing Stop Loss Breakout V2

Ringkasan

Strategi ini menggabungkan keunggulan strategi breakout dan strategi trailing stop berbasis tren, yang bertujuan untuk menangkap sinyal breakout support dan resistance dalam grafik jangka panjang, sambil menggunakan moving average untuk trailing stop, sehingga dapat meraih keuntungan searah dengan tren jangka panjang sekaligus mengendalikan risiko.

Prinsip Strategi

-

Strategi pertama-tama menghitung beberapa kelompok moving average dengan parameter yang berbeda, masing-masing digunakan untuk penentuan tren, support/resistance, dan trailing stop.

-

Kemudian menentukan titik tertinggi dan terendah dalam periode tertentu sebagai zona support/resistance untuk entry. Ketika harga menembus support/resistance ini, sinyal dihasilkan.

-

Strategi menggunakan penembusan titik tertinggi sebagai sinyal long untuk membeli, dan penembusan titik terendah sebagai sinyal short untuk menjual.

-

Setelah entry, posisi ditahan dengan menggunakan titik terendah yang ditembus sebagai level stop loss.

-

Ketika posisi sudah dalam keadaan profit, level stop loss akan berubah menjadi trailing moving average. Ketika harga turun di bawah moving average, titik stop ditetapkan sebagai titik terendah dari candle tersebut.

-

Dengan cara ini, keuntungan dapat diamankan sementara posisi memiliki ruang yang cukup untuk mengikuti pergerakan tren.

-

Strategi juga menambahkan Average True Range (ATR) untuk memastikan hanya membeli pada breakout dengan rentang yang sesuai, menghindari breakout yang terlalu melebar.

Analisis Keunggulan Strategi

-

Menggabungkan keunggulan ganda strategi breakout dan strategi trailing stop berbasis tren.

-

Mampu membeli breakout berdasarkan tren jangka panjang, meningkatkan probabilitas keuntungan.

-

Strategi stop loss tidak hanya melindungi posisi, tetapi juga memberikan ruang yang cukup bagi posisi untuk bergerak.

-

Menambahkan filter volatilitas untuk menghindari breakout yang tidak menguntungkan akibat pergerakan yang berlebihan.

-

Otomatisasi perdagangan, cocok untuk copy trading pada sebagian waktu.

-

Dapat disesuaikan dengan moving average periode berbeda untuk operasional.

-

Dapat secara fleksibel menyesuaikan metode trailing stop.

Analisis Risiko Strategi

-

Strategi breakout rentan terhadap risiko false breakout. Dapat memperlonggar konfirmasi breakout secara wajar.

-

Membutuhkan volatilitas yang cukup untuk menghasilkan sinyal breakout, tidak efektif dalam kondisi pasar yang bergelombang.

-

Beberapa breakout mungkin terlalu singkat untuk ditangkap. Dapat menurunkan timeframe untuk mencari lebih banyak peluang.

-

Trailing stop dapat terlalu sering menghentikan posisi dalam kondisi pasar sideways. Dapat memperlonggar jarak stop loss secara wajar.

-

Filter volatilitas mungkin melewatkan sebagian peluang. Dapat menurunkan parameter filter.

Arah Optimasi Strategi

-

Menguji kombinasi parameter moving average yang berbeda untuk menemukan parameter optimal.

-

Menguji mekanisme konfirmasi breakout yang berbeda, seperti channel, pola candle, dll.

-

Mencoba berbagai metode trailing stop untuk menemukan stop loss terbaik.

-

Mengoptimalkan strategi manajemen modal, seperti position score, dll.

-

Menambahkan filter indikator teknis statistik untuk meningkatkan akurasi filter.

-

Menguji efektivitas strategi pada berbagai instrumen.

-

Menambahkan algoritma pembelajaran mesin untuk meningkatkan efektivitas strategi.

Kesimpulan

Strategi ini mengintegrasikan ide breakout dan trailing stop berbasis tren. Dengan asumsi penentuan tren jangka panjang yang benar, strategi ini dapat mengoptimalkan ruang keuntungan. Kuncinya adalah menemukan kombinasi parameter terbaik dan menggabungkannya dengan strategi manajemen modal yang baik untuk menangkap peluang jangka panjang sambil mengendalikan risiko. Strategi ini diharapkan dapat menjadi strategi tren jangka panjang yang lebih andal melalui optimasi lebih lanjut.

/*backtest

start: 2022-10-17 00:00:00

end: 2023-10-23 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © millerrh

// The intent of this strategy is to buy breakouts with a tight stop on smaller timeframes in the direction of the longer term trend.- 1