Strategi RSI Bollinger Bands untuk Menangkap Volatilitas Dinamis

Ikhtisar

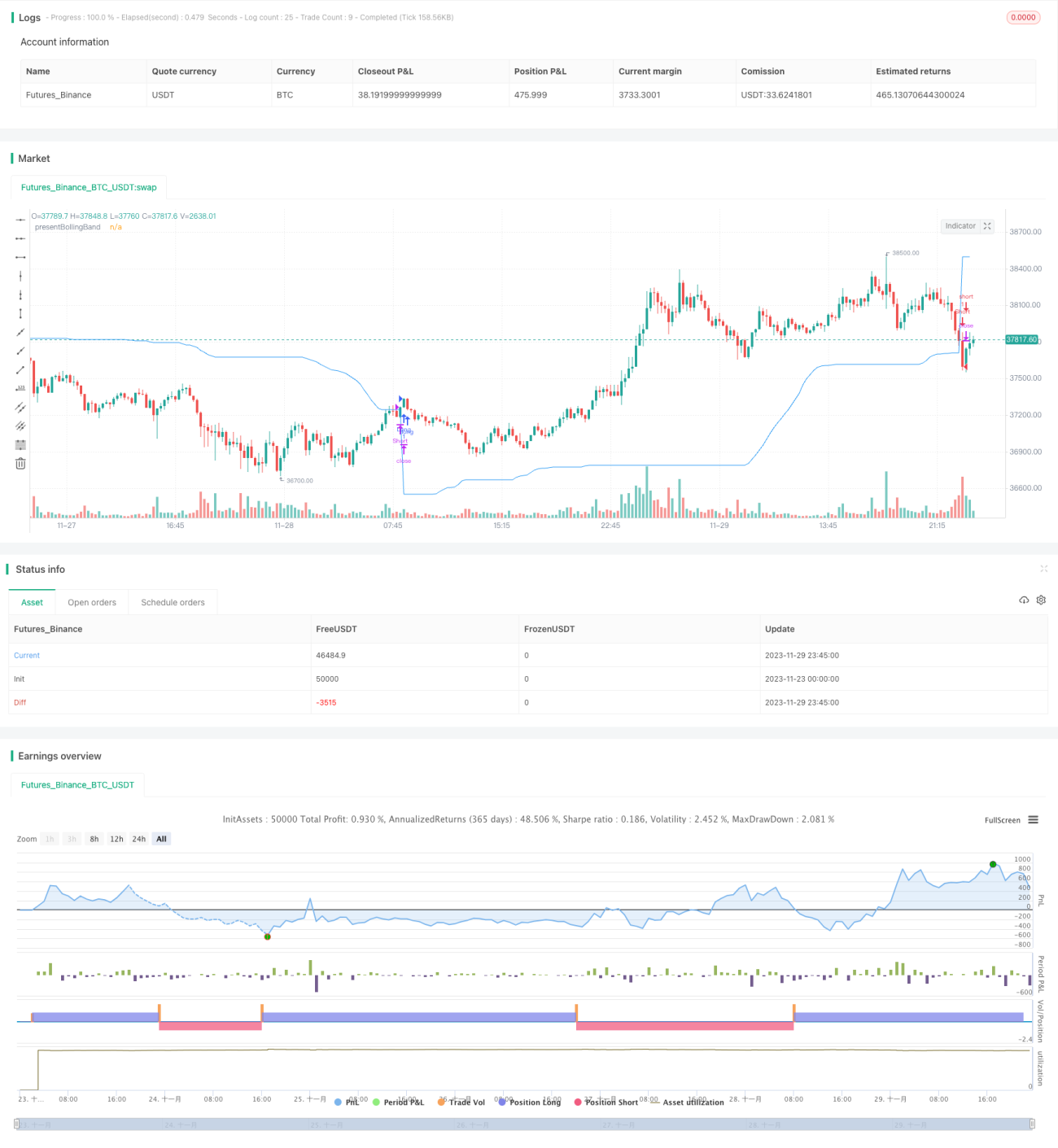

Strategi RSI-Bollinger Band Dynamic Wave Capture adalah strategi trading yang mengintegrasikan konsep Bollinger Band (BB), Relative Strength Index (RSI), dan Simple Moving Average (SMA). Keunikan strategi ini terletak pada kemampuannya menghitung level dinamis antara pita atas dan bawah berdasarkan harga penutupan. Fitur unik ini memungkinkan strategi untuk beradaptasi dengan volatilitas pasar dan pergerakan harga.

Pasar kripto dan saham sangat fluktuatif, sehingga sangat cocok untuk menggunakan strategi Bollinger Band. RSI membantu mengidentifikasi kondisi jenuh beli/jenuh jual di pasar yang seringkali spekulatif ini.

Prinsip Strategi

Bollinger Band Dinamis: Strategi ini pertama-tama menghitung pita atas dan bawah Bollinger Band berdasarkan panjang dan pengali yang ditentukan pengguna. Kemudian, menggabungkan Bollinger Band dan harga penutupan untuk menyesuaikan nilai presentBollingerBand secara dinamis. Akhirnya, ketika harga menembus presentBollingerBand, sinyal beli (long) dihasilkan, dan ketika harga menembus presentBollingerBand (arah sebaliknya), sinyal jual (short) dihasilkan.

RSI: Jika pengguna memilih untuk menggunakan RSI untuk menghasilkan sinyal, strategi ini juga akan menghitung RSI dan SMA-nya, serta menggunakannya untuk menghasilkan sinyal beli dan jual tambahan. Sinyal berbasis RSI hanya digunakan jika opsi "Gunakan RSI untuk menghasilkan sinyal" diatur ke true.

Kemudian, strategi akan memeriksa arah trading yang dipilih dan masuk ke posisi beli atau jual yang sesuai. Jika arah trading diatur ke "Kedua Arah", strategi dapat masuk ke posisi beli dan jual secara bersamaan.

Terakhir, posisi beli ditutup ketika harga penutupan menembus presentBollingerBand, dan posisi jual ditutup ketika harga penutupan menembus presentBollingerBand.

Analisis Keunggulan

Strategi ini menggabungkan keunggulan indikator Bollinger Band, RSI, dan SMA, mampu beradaptasi dengan volatilitas pasar, menangkap pergerakan secara dinamis, serta menghasilkan sinyal trading dalam kondisi jenuh beli/jenuh jual.

Indikator RSI melengkapi sinyal trading Bollinger Band, menghindari entry yang salah di pasar yang bergerak sideways. Memungkinkan pemilihan hanya long, hanya short, atau kedua arah, sehingga dapat beradaptasi dengan berbagai kondisi pasar.

Parameter dapat dikustomisasi, sehingga dapat disesuaikan dengan preferensi risiko individu.

Analisis Risiko

Strategi ini bergantung pada indikator teknis dan tidak dapat mengantisipasi perubahan fundamental yang signifikan.

Pengaturan parameter Bollinger Band yang tidak tepat dapat menyebabkan sinyal trading yang terlalu sering atau terlalu jarang.

Risiko trading dua arah lebih tinggi, perlu diwaspadai kerugian dari posisi short yang berlawanan arah.

Disarankan untuk menggabungkan stop loss guna mengendalikan risiko.

Arah Pengoptimalan

- Menggabungkan indikator lain untuk memfilter sinyal, misalnya MACD.

- Menambahkan strategi stop loss.

- Mengoptimalkan parameter Bollinger Band dan RSI.

- Menyesuaikan parameter berdasarkan instrumen trading dan periode yang berbeda.

- Pertimbangkan optimasi live trading, sesuaikan parameter agar sesuai dengan kondisi aktual.

Kesimpulan

Strategi RSI-Bollinger Band Dynamic Wave Capture adalah strategi yang digerakkan oleh indikator teknis, menggabungkan keunggulan Bollinger Band, RSI, dan SMA, serta menangkap volatilitas pasar melalui penyesuaian dinamis pada Bollinger Band. Strategi ini memiliki ruang kustomisasi dan pengoptimalan yang besar, namun tidak dapat memprediksi perubahan fundamental. Disarankan untuk memverifikasi efektivitasnya dalam live trading, dan jika perlu, sesuaikan parameter atau tambahkan indikator lain untuk mengurangi risiko.

- 1