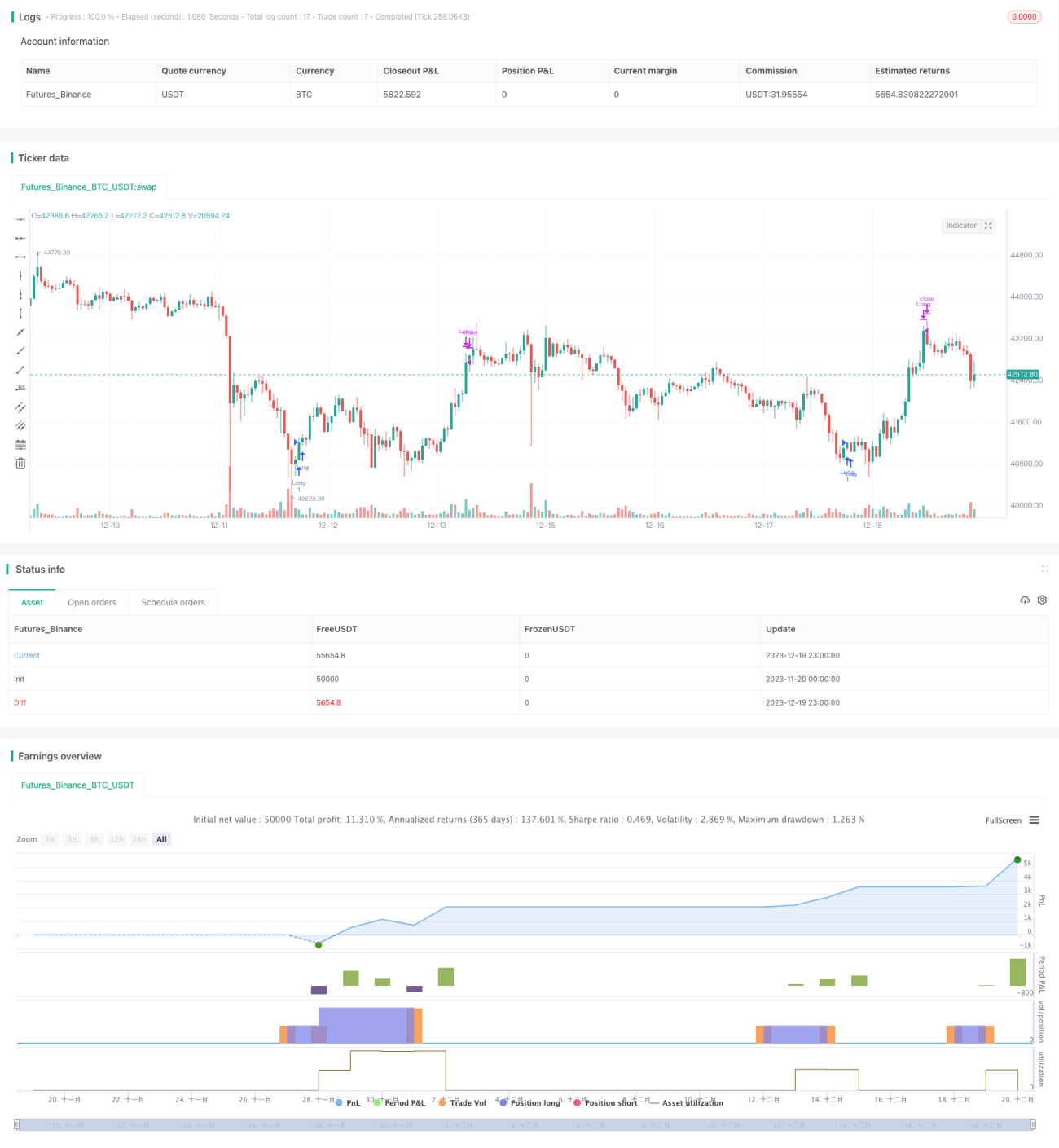

Strategi perdagangan multi-timeframe berdasarkan indikator volatilitas dan indikator stokastik.

Ikhtisar

Strategi ini menggabungkan indikator volatilitas VIX dan indikator stokastik RSI. Dengan mengombinasikan indikator dari periode waktu yang berbeda, strategi ini memungkinkan pembelian breakout yang efisien serta penutupan posisi stop loss berdasarkan kondisi jenuh beli/jenuh jual. Strategi ini memiliki ruang optimasi yang besar dan dapat beradaptasi dengan berbagai kondisi pasar.

Prinsip Strategi

- Hitung indikator volatilitas VIX: Hitung volatilitas menggunakan harga tertinggi dan terendah selama 20 hari terakhir. Ketika volatilitas berada di atas pita atas, pasar menunjukkan kepanikan; ketika di bawah pita bawah, pasar menunjukkan rasa puas diri (complacency).

- Hitung indikator RSI: Hitung persentase perubahan harga selama 14 hari terakhir. Ketika RSI di atas 70, itu adalah zona jenuh beli; ketika di bawah 30, itu adalah zona jenuh jual.

- Gabungkan kedua indikator: Lakukan posisi long ketika volatilitas berada di atas pita atas atau persentil tertinggi; tutup posisi ketika RSI di atas 70.

Kelebihan Strategi

- Menggabungkan berbagai indikator untuk menilai titik waktu pasar secara komprehensif.

- Indikator dari periode waktu yang berbeda saling memvalidasi, meningkatkan akurasi keputusan.

- Parameter dapat dioptimalkan dan disesuaikan agar sesuai dengan instrumen perdagangan yang berbeda.

Analisis Risiko

- Pengaturan parameter yang tidak tepat dapat menyebabkan banyak sinyal palsu.

- Indikator penutupan posisi tunggal rentan melewatkan pembalikan harga.

Saran Optimasi

- Tambahkan lebih banyak indikator verifikasi, misalnya moving average atau Bollinger Bands, untuk menentukan waktu masuk.

- Tambahkan lebih banyak indikator penutupan posisi, misalnya pola candlestick pembalikan, dll.

Kesimpulan

Strategi ini memanfaatkan indikator VIX untuk menilai titik waktu dan tingkat risiko pasar, serta menggabungkan indikator RSI untuk menyaring titik perdagangan yang tidak menguntungkan akibat kondisi jenuh beli/jenuh jual. Dengan demikian, strategi ini dapat melakukan pembelian pada waktu yang efisien dan melakukan stop loss tepat waktu. Strategi ini memiliki ruang optimasi yang besar dan dapat beradaptasi dengan lingkungan pasar yang lebih luas.

- 1