Menerapkan Strategi Pelacakan Keseimbangan dengan Hull Moving Average

Ikhtisar

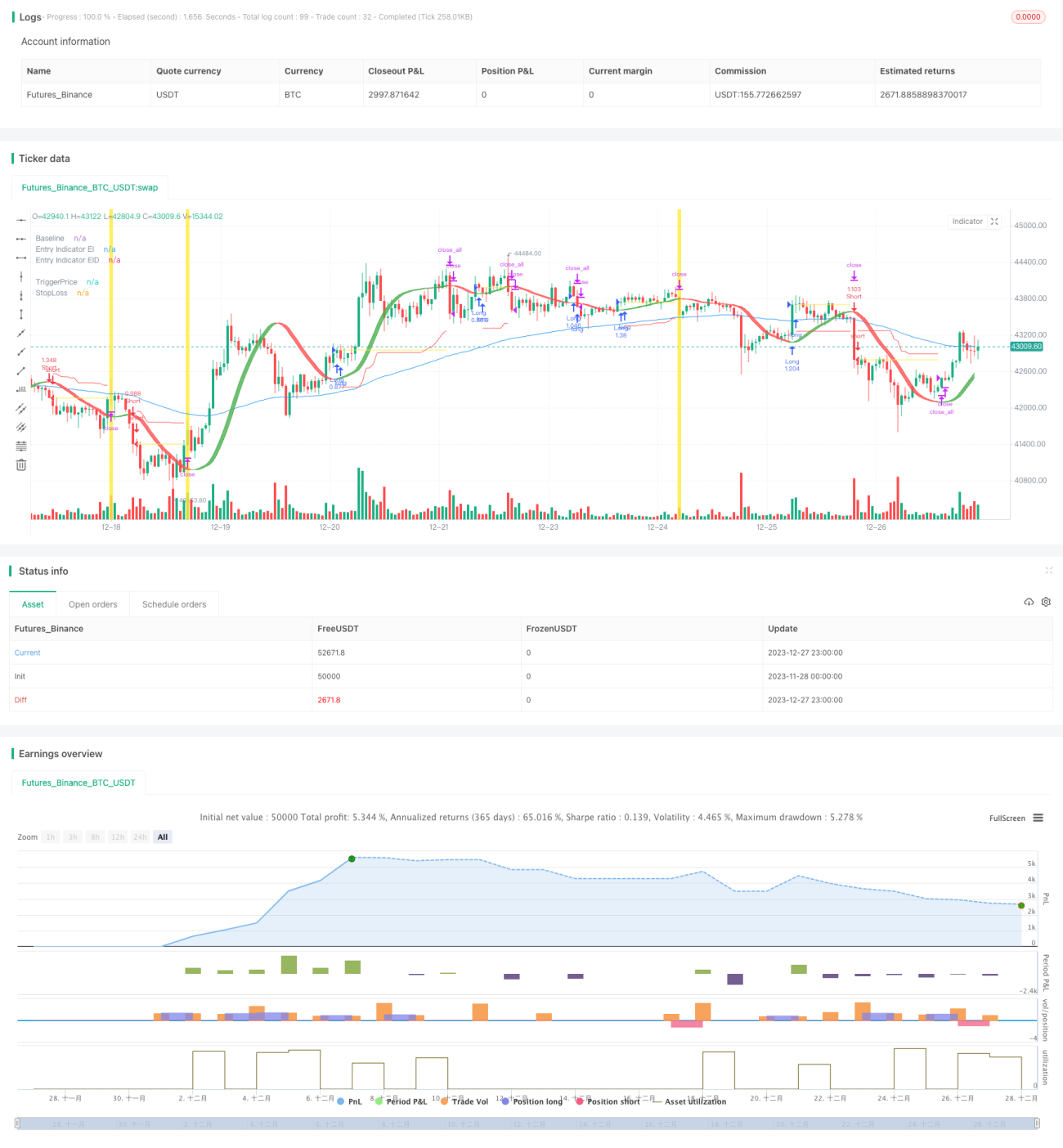

Strategi pelacakan keseimbangan menggunakan Hull Moving Average sebagai indikator masuk utama untuk menentukan arah tren harga. Pada saat yang sama, strategi ini menggabungkan berbagai indikator lain, seperti garis dasar, indikator konfirmasi, dll., untuk memvalidasi tren harga dan menyaring sinyal palsu. Setelah masuk pasar, strategi ini menggunakan Average True Range untuk menghitung stop-loss dinamis guna melacak keuntungan dari tren.

Prinsip Strategi

Inti dari strategi pelacakan keseimbangan adalah Hull Moving Average. Hull Moving Average lebih sensitif terhadap perubahan harga dan dapat secara efektif menentukan arah tren. Ketika harga menembus ke atas garis Hull, konfirmasi tren naik terbentuk, lakukan long; ketika harga menembus ke bawah garis Hull, konfirmasi tren turun terbentuk, lakukan short.

Selain itu, strategi ini juga memperkenalkan indikator garis dasar untuk menentukan tren jangka panjang/pendek; indikator konfirmasi untuk menyaring breakout palsu. Hanya ketika garis dasar dan indikator konfirmasi keduanya memvalidasi arah tren, sinyal trading akan dihasilkan.

Setelah masuk pasar, strategi ini menggunakan Average True Range yang dihitung dari ATR dan Hull EMA untuk menetapkan posisi stop-loss. Seiring berlanjutnya tren, garis stop-loss juga akan terus bergerak ke atas/bawah untuk mengunci keuntungan dari tren.

Analisis Keunggulan

Strategi pelacakan keseimbangan menggabungkan keunggulan penentuan tren dan manajemen risiko, sehingga dapat memperoleh hasil yang baik dalam kondisi tren. Dibandingkan dengan strategi stop-loss tetap, strategi ini dapat melacak pergerakan tren melalui stop-loss bergerak, menghindari stop-loss akibat fluktuasi normal pasar.

Kombinasi berbagai indikator juga membuat strategi lebih sensitif terhadap perubahan pasar, sekaligus dapat secara efektif menyaring sinyal palsu. Selain itu, strategi ini menyediakan beberapa parameter yang dapat disesuaikan, sehingga pengguna dapat mengoptimalkannya sesuai dengan penilaian pasar mereka sendiri.

Analisis Risiko

Strategi ini terutama bergantung pada indikator tren, sehingga mudah menghasilkan sinyal palsu dan stop-loss saat pasar sideways. Selain itu, kombinasi beberapa indikator juga dapat menyebabkan konflik indikator. Pengaturan parameter yang tidak tepat juga dapat menyebabkan performa strategi yang buruk.

Pertimbangkan untuk menambahkan modul penilaian tambahan ke dalam strategi, seperti menjeda trading saat indikator berbeda pendapat; atau menggunakan mekanisme voting untuk menggabungkan hasil penilaian dari beberapa indikator. Dalam hal pengaturan parameter, parameter optimal dapat ditemukan melalui metode optimasi backtest.

Arah Optimasi

Strategi pelacakan keseimbangan dapat dioptimalkan dari beberapa arah berikut:

- Menambahkan modul penilaian, seperti modul volatilitas, untuk menjeda trading saat volatilitas tinggi;

- Menambahkan modul machine learning, menggunakan algoritma machine learning untuk menentukan bobot indikator;

- Mengoptimalkan parameter indikator untuk menemukan kombinasi parameter terbaik;

- Mengoptimalkan algoritma stop-loss bergerak agar stop-loss dapat melacak tren dengan lebih baik;

- Menambahkan modul manajemen risiko, seperti penghentian kerugian yang melanggar, penyesuaian posisi dinamis, dll.

Kesimpulan

Secara keseluruhan, strategi pelacakan keseimbangan adalah strategi pelacakan tren yang sangat baik. Strategi ini berhasil menggabungkan penentuan tren dengan stop-loss dinamis, sehingga dapat secara efektif melacak keuntungan dari tren. Melalui optimasi lebih lanjut, strategi ini diharapkan dapat memperoleh performa yang lebih baik. Strategi ini menyediakan referensi yang baik untuk pembangunan strategi trading kuantitatif.

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1