Strategi Pembalikan RSI dari Indikator MACD

Ikhtisar

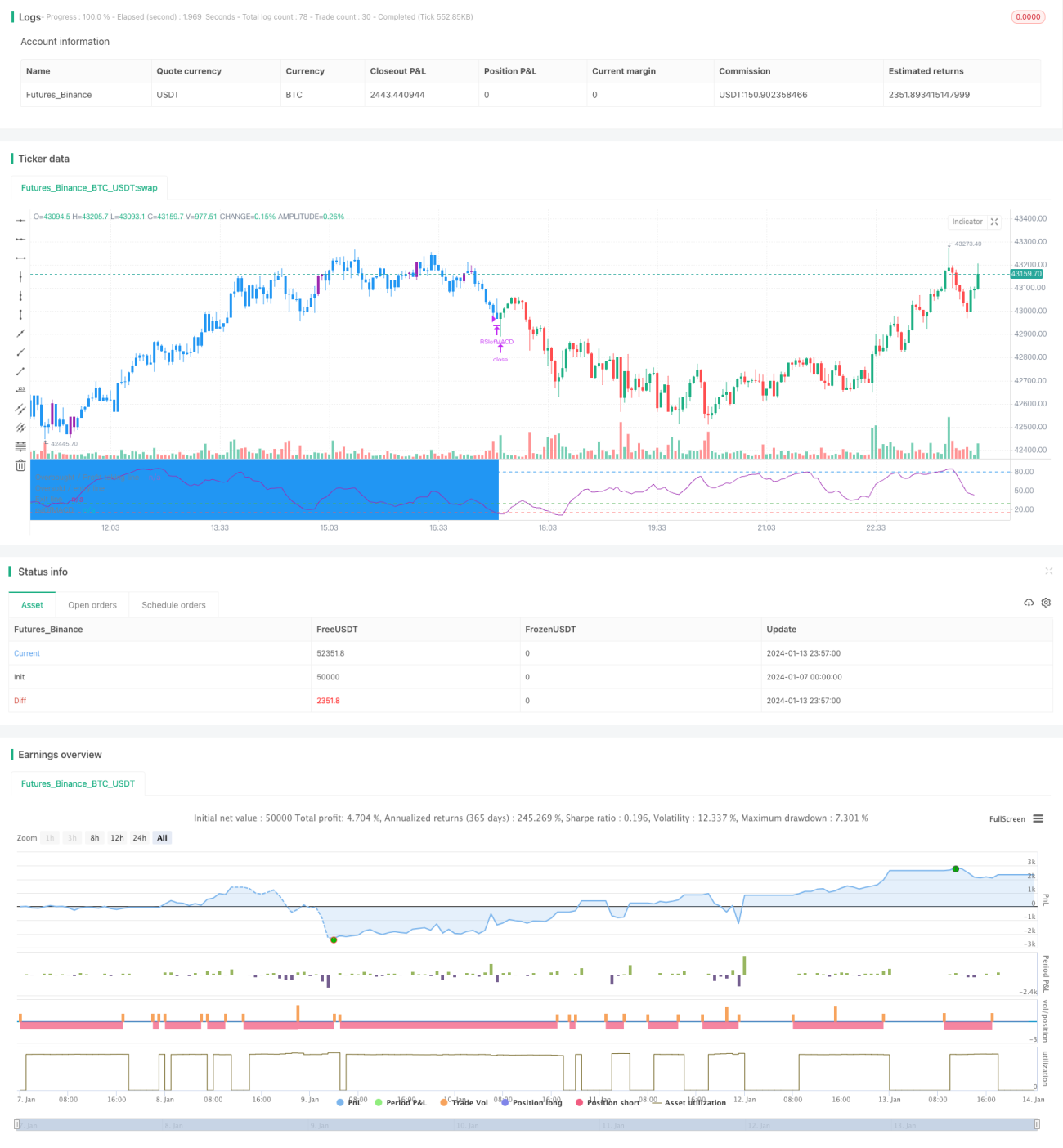

Strategi ini menggunakan nilai RSI dari indikator MACD untuk menentukan sinyal beli dan jual. Pembelian dilakukan ketika nilai RSI melebihi garis overbought atau zona oversold, sedangkan stop loss atau take profit dilakukan ketika nilai RSI turun di bawah zona oversold.

Prinsip Strategi

Strategi ini menggabungkan keunggulan indikator MACD dan RSI.

Pertama, tiga kurva indikator MACD dihitung, yaitu garis DIF, garis DEA, dan garis MACD. Kemudian dihitung indikator RSI pada garis MACD, sehingga terbentuk RSI of MACD.

Ketika nilai RSI of MACD melebihi zona oversold 30 atau 35, sinyal beli dihasilkan, yang menunjukkan bahwa garis MACD memasuki area oversold dan tren harga saham mulai berbalik naik. Ketika nilai RSI of MACD kembali turun di bawah zona oversold 15, sinyal jual dihasilkan, yang menunjukkan bahwa pembalikan tren telah berakhir.

Strategi ini juga menetapkan take profit sebagian, ketika nilai RSI of MACD melebihi zona overbought 80, sebagian posisi dapat dijual untuk mengunci sebagian keuntungan.

Analisis Keunggulan

- Menggunakan indikator MACD untuk menentukan titik pembalikan tren

- Menggunakan indikator RSI untuk menentukan area overbought/oversold, menyaring sinyal palsu

- Kombinasi dua indikator untuk menentukan titik beli dan jual secara akurat

- Menetapkan take profit sebagian untuk mencegah kerugian membesar

Analisis Risiko

- Pengaturan parameter MACD yang tidak tepat dapat menyebabkan ketidakmampuan menentukan tren secara akurat

- Pengaturan parameter RSI yang tidak tepat dapat menyebabkan ketidakmampuan menentukan overbought/oversold secara akurat

- Pengaturan take profit sebagian yang terlalu agresif dapat menyebabkan kehilangan potensi kenaikan yang lebih besar

Solusi:

- Optimalkan parameter MACD untuk menemukan kombinasi parameter terbaik

- Optimalkan parameter RSI untuk meningkatkan akurasi

- Longgarkan kondisi take profit sebagian secara tepat untuk mengejar keuntungan yang lebih besar

Arah Optimasi

Strategi ini juga dapat dioptimalkan dari beberapa arah berikut:

- Menambahkan strategi stop loss untuk lebih mengendalikan risiko penurunan

- Menambahkan modul manajemen posisi agar posisi dapat diperbesar secara bertahap seiring pergerakan harga

- Mengintegrasikan model machine learning, menggunakan data historis untuk pelatihan guna lebih meningkatkan akurasi penentuan titik beli dan jual

- Mencoba berjalan pada siklus yang lebih pendek seperti 15 menit atau 5 menit untuk meningkatkan frekuensi strategi

Kesimpulan

Strategi ini memiliki kerangka pemikiran yang jelas secara keseluruhan, dengan ide inti menggunakan pembalikan MACD yang dikombinasikan dengan penyaringan RSI untuk menentukan titik beli dan jual. Melalui optimasi parameter, manajemen stop loss, pengendalian risiko, dan cara lainnya, strategi ini dapat diubah menjadi strategi trading kuantitatif yang sangat praktis.

- 1