Strategi Perdagangan Multi-Kerangka Waktu Berbasis RSI dan Rata-rata Bergerak

Ikhtisar

Strategi ini menggabungkan Stochastic RSI, Simple Moving Average (SMA), dan Weighted Moving Average (WMA) untuk mencari sinyal beli dan jual. Strategi ini secara bersamaan menilai arah tren pada kerangka waktu 5 menit dan 1 jam. Dalam tren yang stabil, ketika RSI cepat melintasi ke atas atau ke bawah garis RSI lambat, maka dihasilkan sinyal trading.

Prinsip Strategi

Strategi ini terlebih dahulu menghitung Weighted Moving Average (WMA) periode 144 dan Simple Moving Average (SMA) periode 5 pada dua kerangka waktu, yaitu 1 jam dan 5 menit. Hanya ketika SMA 5 menit berada di atas WMA, pasar dianggap dalam kondisi bullish. Kemudian strategi menghitung indikator bullish/bearish RSI, serta garis K dan D yang sesuai. Ketika garis K melintasi ke bawah garis D dari area overbought, dihasilkan sinyal jual; ketika garis K melintasi ke atas garis D dari area oversold, dihasilkan sinyal beli.

Analisis Keunggulan

Ini adalah strategi pengikut tren yang sangat efektif. Strategi ini menggabungkan dua kerangka waktu untuk menilai tren, sehingga sangat efektif mengurangi sinyal palsu. Selain itu, strategi ini menggabungkan berbagai indikator untuk menyaring sinyal, termasuk RSI, SMA, dan WMA, membuat sinyal lebih andal. Dengan menggunakan RSI untuk menggerakkan KDJ, strategi ini juga memodifikasi masalah sinyal palsu yang sering terjadi pada strategi KDJ biasa. Selain itu, strategi ini memiliki pengaturan stop loss dan take profit untuk mengunci keuntungan, sehingga dapat mengelola risiko secara efektif.

Analisis Risiko

Risiko terbesar dari strategi ini adalah kesalahan dalam penilaian tren. Pada titik balik pasar, rata-rata bergerak jangka pendek dan jangka panjang mungkin melintasi ke atas atau ke bawah secara bersamaan, sehingga menghasilkan sinyal palsu. Selain itu, dalam kondisi pasar yang bergejolak (sideways), RSI juga dapat menghasilkan banyak sinyal trading yang membingungkan. Namun, risiko-risiko ini dapat dikurangi dengan menyesuaikan periode SMA dan WMA serta parameter RSI secara tepat.

Arah Optimasi

Strategi ini dapat dioptimalkan dari beberapa aspek berikut:

- Menguji SMA, WMA, dan RSI dengan panjang yang berbeda untuk menemukan kombinasi parameter terbaik.

- Menambahkan indikator lain seperti MACD, Bollinger Bands, dll. untuk memverifikasi keandalan sinyal.

- Mengoptimalkan strategi stop loss dan take profit dengan menguji metode fixed percentage stop loss, balance slippage stop loss, trailing stop, dll.

- Menambahkan modul manajemen modal untuk mengontrol ukuran investasi per perdagangan dan eksposur risiko keseluruhan.

- Menambahkan algoritma machine learning untuk menemukan parameter dengan kinerja terbaik melalui backtesting yang ekstensif.

Kesimpulan

Strategi ini memanfaatkan sepenuhnya keunggulan moving average dan indikator stochastic untuk membangun sistem pengikut tren yang cukup andal. Melalui verifikasi berbagai kerangka waktu dan indikator, strategi ini mampu menangkap arah tren jangka menengah dan panjang dengan lancar. Pada saat yang sama, pengaturan stop loss dan take profit memungkinkannya menahan fluktuasi pasar sampai batas tertentu. Namun, masih ada ruang untuk perbaikan, seperti menguji kombinasi lebih banyak indikator, memperkenalkan metode machine learning untuk menemukan parameter optimal, dll. Secara keseluruhan, ini adalah strategi trading yang sangat menjanjikan.

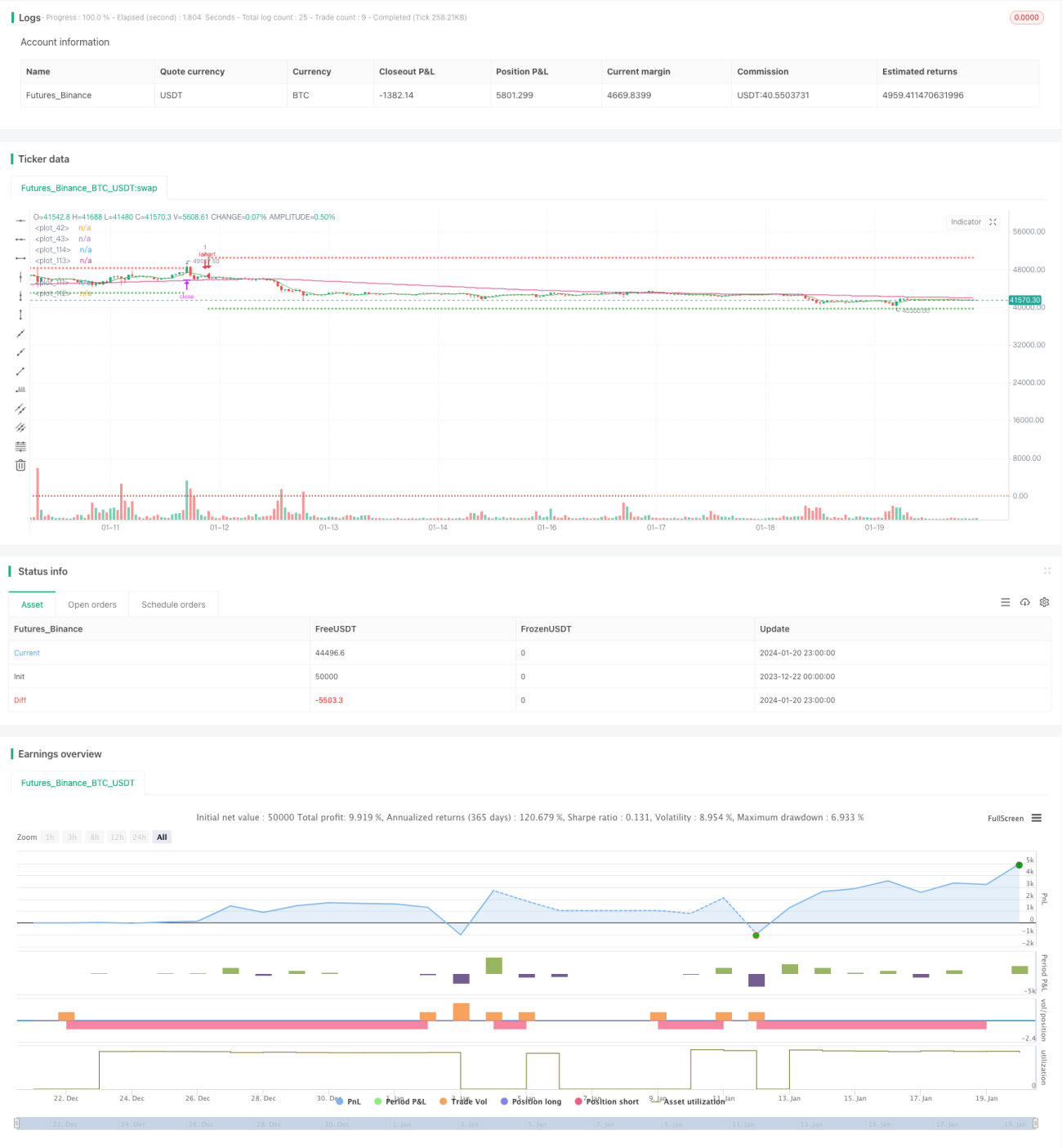

/*backtest

start: 2023-12-22 00:00:00

end: 2024-01-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © bufirolas

// Works well with a wide stop with 20 bars lookback- 1