Strategi Pelacakan Momentum dengan Filter Rentang Adaptif Dua Arah

1

Follow

1802

Followers

Ringkasan

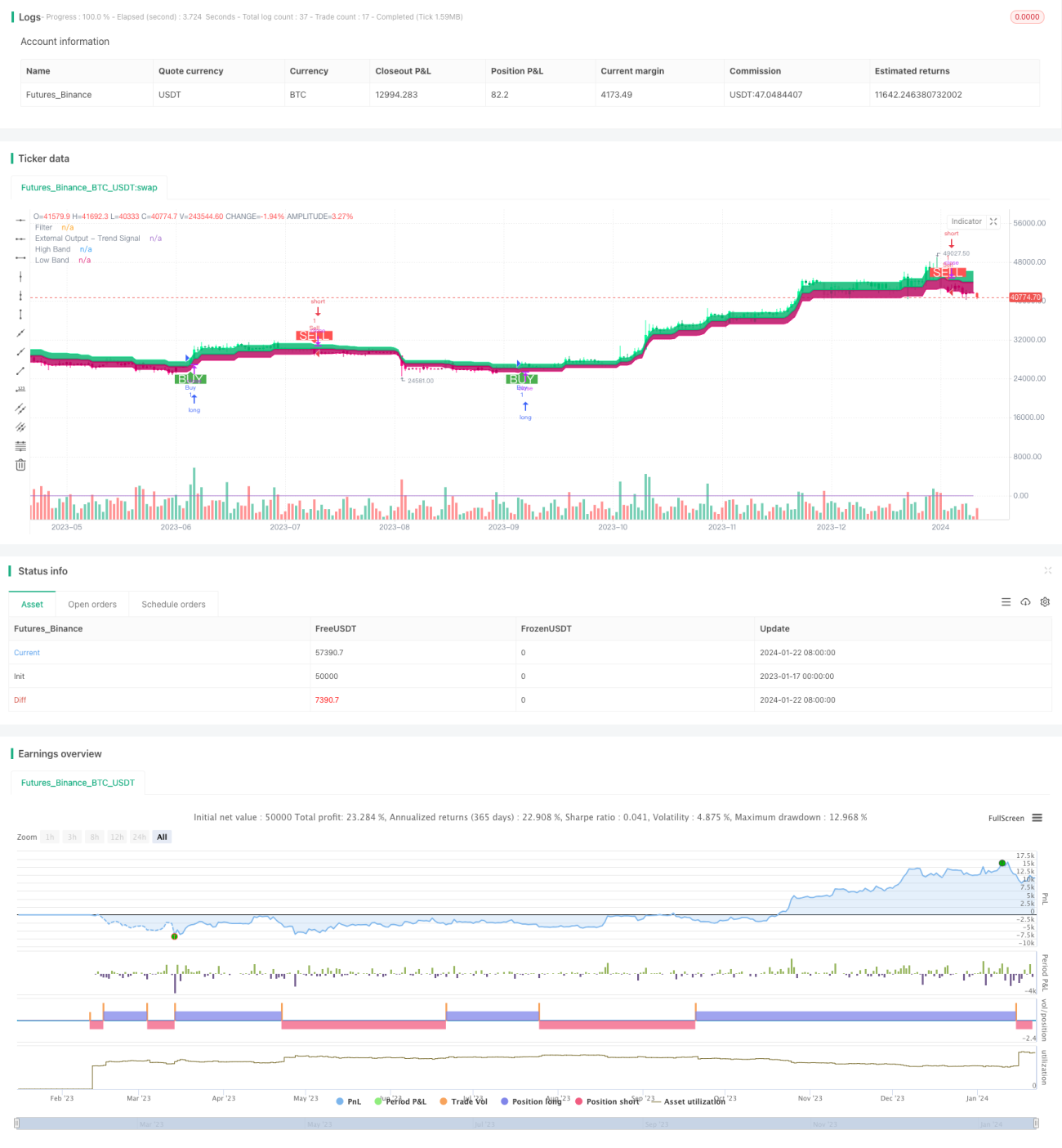

Strategi ini adalah strategi pelacakan momentum filter rentang adaptif dua arah. Strategi ini menggunakan filter rentang adaptif untuk melacak pergerakan harga, dan menggabungkan indikator volume untuk menentukan arah nilai, sehingga dapat membeli di harga rendah dan menjual di harga tinggi.

Prinsip Strategi

- Gunakan filter rentang adaptif untuk melacak pergerakan harga. Ukuran filter disesuaikan secara adaptif berdasarkan periode rentang, jumlah, dan skala yang ditetapkan pengguna.

- Filter dibagi menjadi dua jenis: Tipe 1 dan Tipe 2. Tipe 1 adalah tipe pelacakan rentang standar, Tipe 2 adalah tipe pembulatan bertahap.

- Arah pergerakan harga ditentukan berdasarkan hubungan antara filter dan harga penutupan. Harga di atas pita atas menandakan bullish, di bawah pita bawah menandakan bearish.

- Arah nilai ditentukan dengan menggabungkan perubahan harga penutupan dibandingkan hari sebelumnya. Nilai naik berarti posisi long, turun berarti posisi short.

- Saat harga menembus pita atas dan nilai naik, sinyal beli dikeluarkan; saat harga menembus di bawah pita bawah dan nilai turun, sinyal jual dikeluarkan.

Analisis Keunggulan

- Filter rentang adaptif dapat menangkap volatilitas pasar dengan akurat.

- Dua jenis filter dapat memenuhi preferensi perdagangan yang berbeda.

- Menggabungkan indikator volume dapat secara efektif mengidentifikasi arah nilai.

- Strategi ini fleksibel, parameter dapat disesuaikan dengan pasar.

- Dapat dikustomisasi untuk memilih logika kondisi perdagangan yang sesuai.

Analisis Risiko

- Pengaturan parameter yang tidak tepat dapat menyebabkan overtrading atau kehilangan sinyal.

- Sinyal breakout memiliki sedikit keterlambatan.

- Indikator volume memiliki risiko lag (keterlambatan).

- Breakout rentang rentan terhadap jebakan (perangkap).

Pencegahan Risiko:

- Pilih kombinasi parameter yang tepat dan sesuaikan tepat waktu.

- Gabungkan dengan indikator lain untuk mengidentifikasi tren.

- Berhati-hatilah dalam bertransaksi di dekat level kunci dan saat pembalikan tren.

Arah Optimasi

- Uji berbagai kombinasi ukuran rentang dan periode smoothing untuk menemukan kombinasi terbaik.

- Coba berbagai jenis filter, pilih jenis yang sesuai preferensi pribadi.

- Uji coba indikator volume lain atau indikator teknis tambahan.

- Optimalkan dan sesuaikan logika kondisi perdagangan untuk mengurangi perdagangan irasional.

- Gabungkan teori fraktal pasar untuk menetapkan proporsi penyesuaian posisi yang adaptif.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1