Sistem Pelacakan Bull Market

Gambaran Umum

Sistem Pelacak Bullish adalah sistem perdagangan mekanis berbasis trend following. Sistem ini menggunakan indikator tren pada grafik 4 jam untuk menyaring sinyal perdagangan, sementara entri ditentukan berdasarkan indikator pada grafik 15 menit. Indikator utama meliputi RSI, Stochastic, dan MACD. Kelebihan sistem ini adalah kombinasi multi-timeframe yang dapat menyaring sinyal palsu secara efektif, sekaligus memanfaatkan indikator timeframe lebih rendah untuk mendapatkan waktu masuk yang lebih akurat. Namun, sistem ini juga memiliki beberapa risiko, seperti kecenderungan menghasilkan overtrading dan masalah false breakout.

Prinsip Kerja

Logika inti sistem ini adalah menggabungkan indikator dari berbagai timeframe untuk mengidentifikasi arah tren dan waktu masuk. Secara spesifik, RSI, Stochastic, dan EMA pada grafik 4 jam harus memenuhi kondisi tertentu untuk menentukan arah tren secara keseluruhan. Hal ini dapat menyaring sebagian besar noise secara efektif. Sementara itu, RSI, Stochastic, MACD, dan EMA pada grafik 15 menit juga harus menunjukkan arah bullish atau bearish yang sama untuk menentukan waktu masuk yang spesifik. Dengan demikian, titik beli dan jual yang lebih baik dapat ditemukan. Sistem ini hanya akan mengeluarkan sinyal perdagangan ketika penilaian pada timeframe 4 jam dan 15 menit saling sesuai.

Keunggulan

- Kombinasi multi-timeframe secara efektif menyaring sinyal palsu dan mengidentifikasi tren utama.

- Indikator detail pada timeframe 15 menit memungkinkan waktu masuk yang lebih akurat.

- Kombinasi indikator menggunakan RSI, Stochastic, MACD, dan indikator teknikal populer lainnya, mudah dipahami dan juga mudah dioptimalkan.

- Menerapkan manajemen risiko yang ketat seperti trailing take profit, stop loss, trailing stop loss, dll., sehingga dapat mengendalikan risiko per transaksi secara efektif.

Risiko

- Risiko overtrading. Sistem ini cukup sensitif terhadap timeframe pendek, sehingga dapat menghasilkan banyak sinyal perdagangan dan menyebabkan overtrading.

- Risiko false breakout. Penilaian indikator jangka pendek dapat mengalami kesalahan dan menghasilkan sinyal false breakout.

- Risiko kegagalan indikator. Indikator teknikal sendiri memiliki keterbatasan tertentu dan dapat gagal dalam kondisi pasar yang ekstrem.

Sebagai respons, sistem ini dapat dioptimalkan dari beberapa aspek berikut:

- Menyesuaikan parameter indikator agar lebih cocok dengan berbagai kondisi pasar.

- Menambahkan kondisi penyaringan untuk mengurangi frekuensi perdagangan dan mencegah overtrading.

- Mengoptimalkan strategi take profit dan stop loss agar lebih sesuai dengan rentang volatilitas pasar.

- Menguji berbagai kombinasi indikator untuk mencari solusi optimal.

Kesimpulan

Secara keseluruhan, Sistem Pelacak Bullish adalah sistem perdagangan mekanis trend following yang sangat praktis. Sistem ini menggunakan indikator kombinasi multi-timeframe untuk mengidentifikasi tren pasar dan momentum entri kunci. Dengan pengaturan parameter yang tepat dan pengujian optimasi berkelanjutan, sistem ini dapat beradaptasi dengan sebagian besar kondisi pasar dan mencapai hasil profit yang stabil. Namun, kita juga harus menyadari beberapa potensi risiko di dalamnya dan mengambil langkah-langkah proaktif untuk mencegah dan mengatasinya.

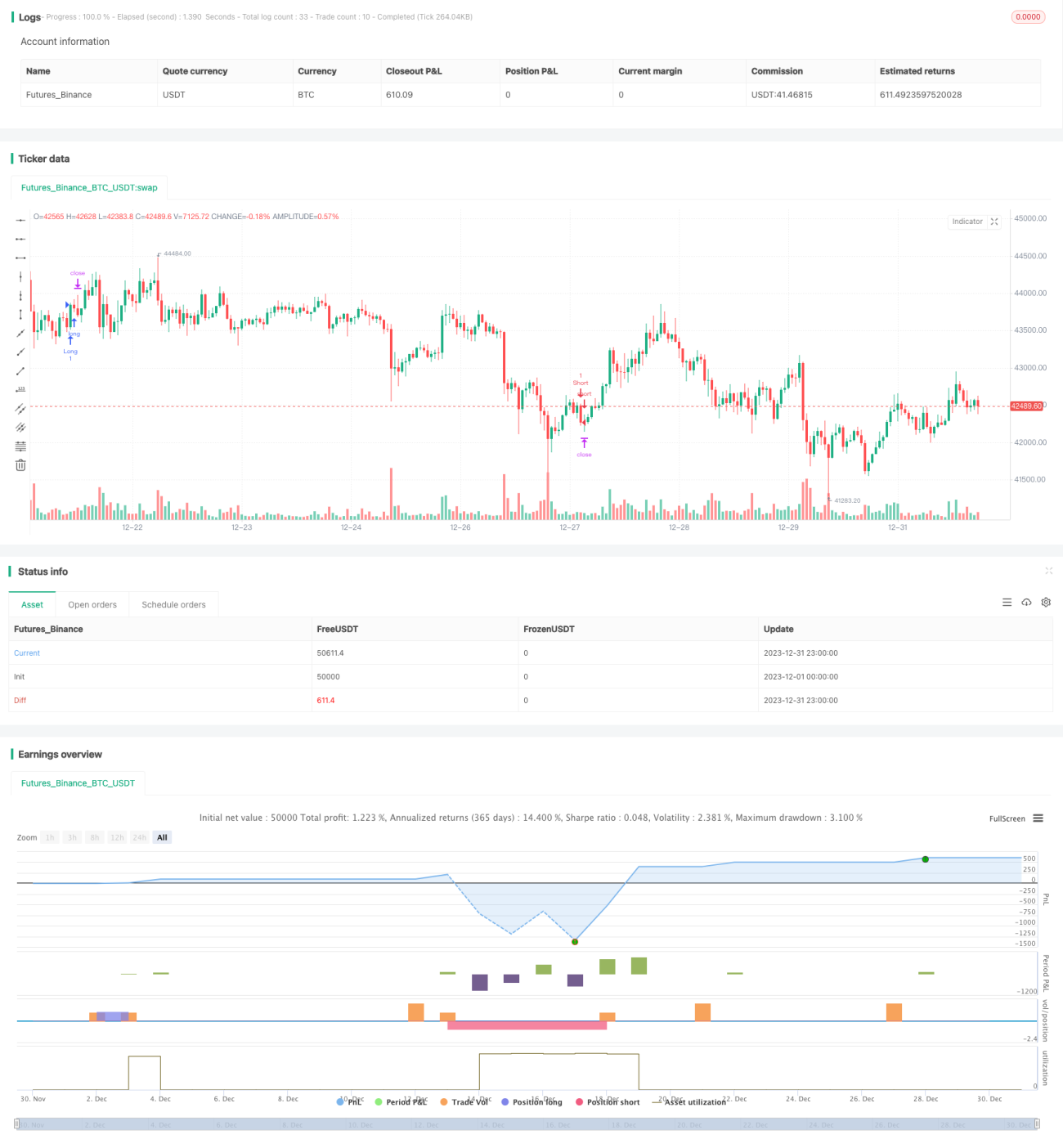

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Cowabunga System from babypips.com", overlay=true)

// 4 Hour Stochastics

length4 = input(162, minval=1, title="4h StochLength"), smoothK4 = input(48, minval=1, title="4h StochK"), smoothD4 = input(48, minval=1, title="4h StochD")- 1