Strategi Trading Emas Berbasis Momentum dan Standar Deviasi

Ikhtisar

Strategi ini menilai kondisi overbought dan oversold pasar dengan menghitung deviasi harga emas terhadap rata-rata pergerakan eksponensial 21 hari, dikombinasikan dengan standar deviasi. Ketika deviasi mencapai level standar deviasi tertentu, strategi mengadopsi pendekatan pengikut tren (trend-following) dan dilengkapi mekanisme stop-loss untuk mengelola risiko.

Prinsip Strategi

- Hitung rata-rata pergerakan eksponensial 21 hari sebagai garis tengah.

- Hitung deviasi harga emas terhadap rata-rata pergerakan tersebut.

- Standarisasi deviasi menjadi Z-Score.

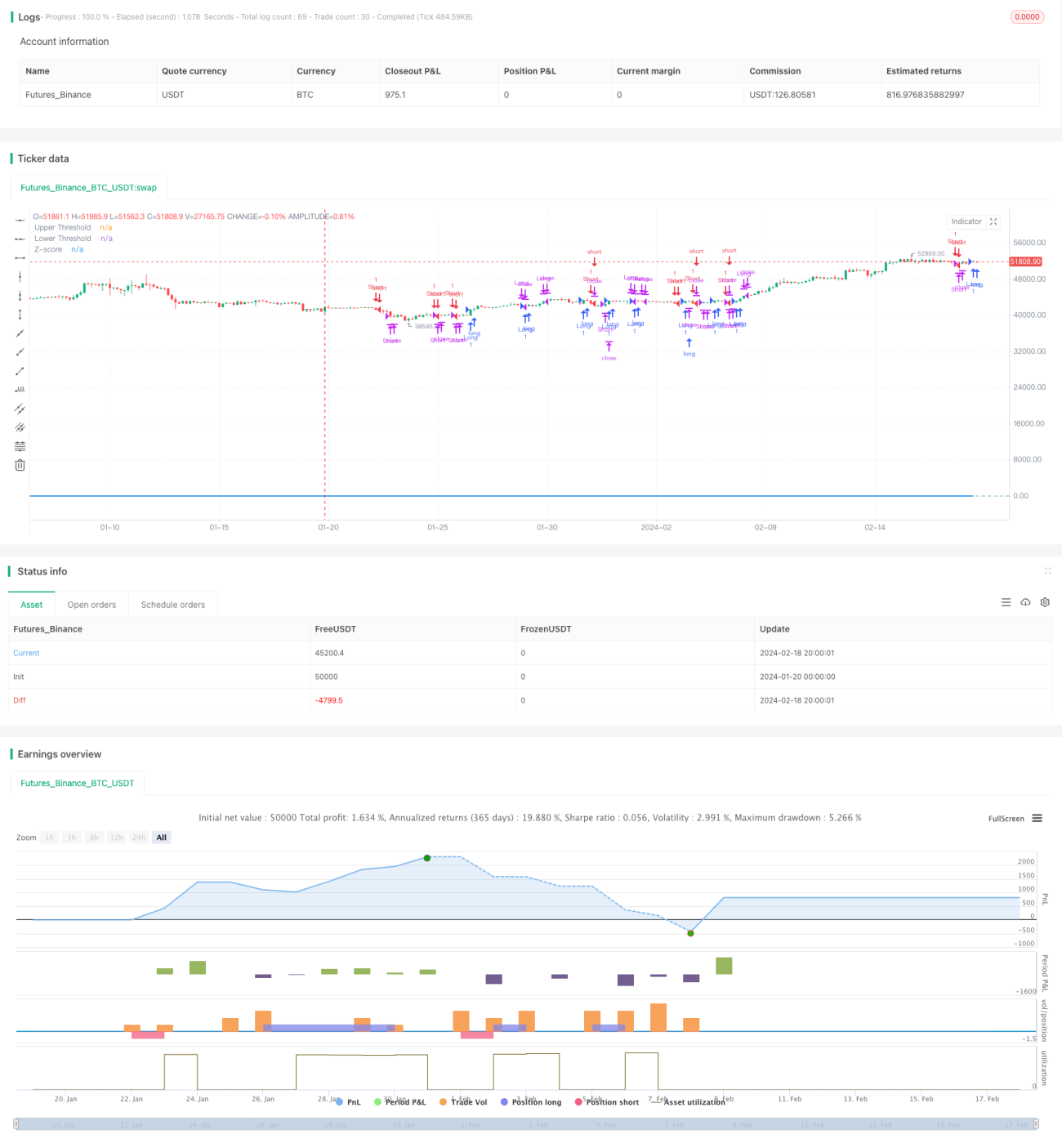

- Ketika Z-Score menembus ke atas 0,5, lakukan posisi long (beli); ketika Z-Score menembus ke bawah -0,5, lakukan posisi short (jual).

- Ketika Z-Score kembali ke ambang batas 0,5/-0,5, tutup posisi.

- Ketika Z-Score melebihi 3/-3, lakukan stop-loss.

Analisis Keunggulan

Ini adalah strategi pengikut tren yang menilai kondisi overbought dan oversold berdasarkan momentum harga dan standar deviasi. Keunggulannya meliputi:

- Menggunakan rata-rata pergerakan sebagai support/resistance dinamis, mampu menangkap tren.

- Standar deviasi dan Z-Score dapat menilai kondisi overbought/oversold dengan baik, mengurangi sinyal palsu.

- Menggunakan rata-rata pergerakan eksponensial yang lebih sensitif terhadap perubahan harga terkini.

- Standarisasi deviasi harga dengan Z-Score membuat aturan penilaian lebih seragam dan konsisten.

- Memiliki mekanisme stop-loss untuk menghentikan kerugian tepat waktu dan mengelola risiko.

Analisis Risiko

Strategi ini juga memiliki beberapa risiko:

- Ketika harga mengalami gap atau breakout signifikan, rata-rata pergerakan sebagai acuan dapat menghasilkan sinyal yang salah.

- Ambang batas penilaian standar deviasi dan Z-Score perlu diatur dengan tepat; terlalu besar atau terlalu kecil akan memengaruhi kinerja strategi.

- Pengaturan stop-loss yang tidak tepat dapat terlalu agresif dan menyebabkan kerugian yang tidak perlu.

- Fluktuasi harga drastis akibat kejadian tak terduga dapat memicu stop-loss dan menyebabkan hilangnya peluang tren.

Solusi:

- Atur parameter rata-rata pergerakan secara wajar untuk mengidentifikasi tren utama.

- Optimalkan parameter standar deviasi melalui backtest untuk menemukan ambang batas terbaik.

- Gunakan trailing stop untuk memeriksa kewajaran stop-loss strategi.

- Evaluasi ulang kondisi pasar dan sesuaikan parameter strategi setelah kejadian.

Arah Optimasi

Strategi ini dapat dioptimalkan dari beberapa aspek berikut:

- Gunakan indikator volatilitas seperti ATR sebagai pengganti standar deviasi sederhana untuk menilai risiko dengan lebih baik.

- Coba berbagai jenis rata-rata pergerakan untuk menemukan garis tengah yang lebih sesuai.

- Optimalkan parameter rata-rata pergerakan untuk mengidentifikasi periode terbaik.

- Optimalkan ambang batas Z-Score untuk menemukan titik parameter kinerja strategi terbaik.

- Tambahkan metode stop-loss berbasis volatilitas agar stop-loss lebih cerdas dan rasional.

Kesimpulan

Secara keseluruhan, strategi ini merupakan strategi pengikut tren yang fundamental dan wajar. Ia menggunakan rata-rata pergerakan untuk menilai arah tren utama, dan melalui standarisasi deviasi harga, mampu menilai kondisi overbought/oversold dengan jelas sehingga menghasilkan sinyal perdagangan. Pengaturan stop-loss yang tepat juga memungkinkan strategi mengendalikan risiko sambil mempertahankan profit. Dengan optimasi parameter lebih lanjut dan penambahan lebih banyak kondisi penilaian, strategi ini dapat menjadi lebih stabil dan andal, serta memiliki nilai aplikasi yang tinggi.

- 1