アルゴリズムRSIレンジブレイク戦略

1

Follow

1802

Followers

概要

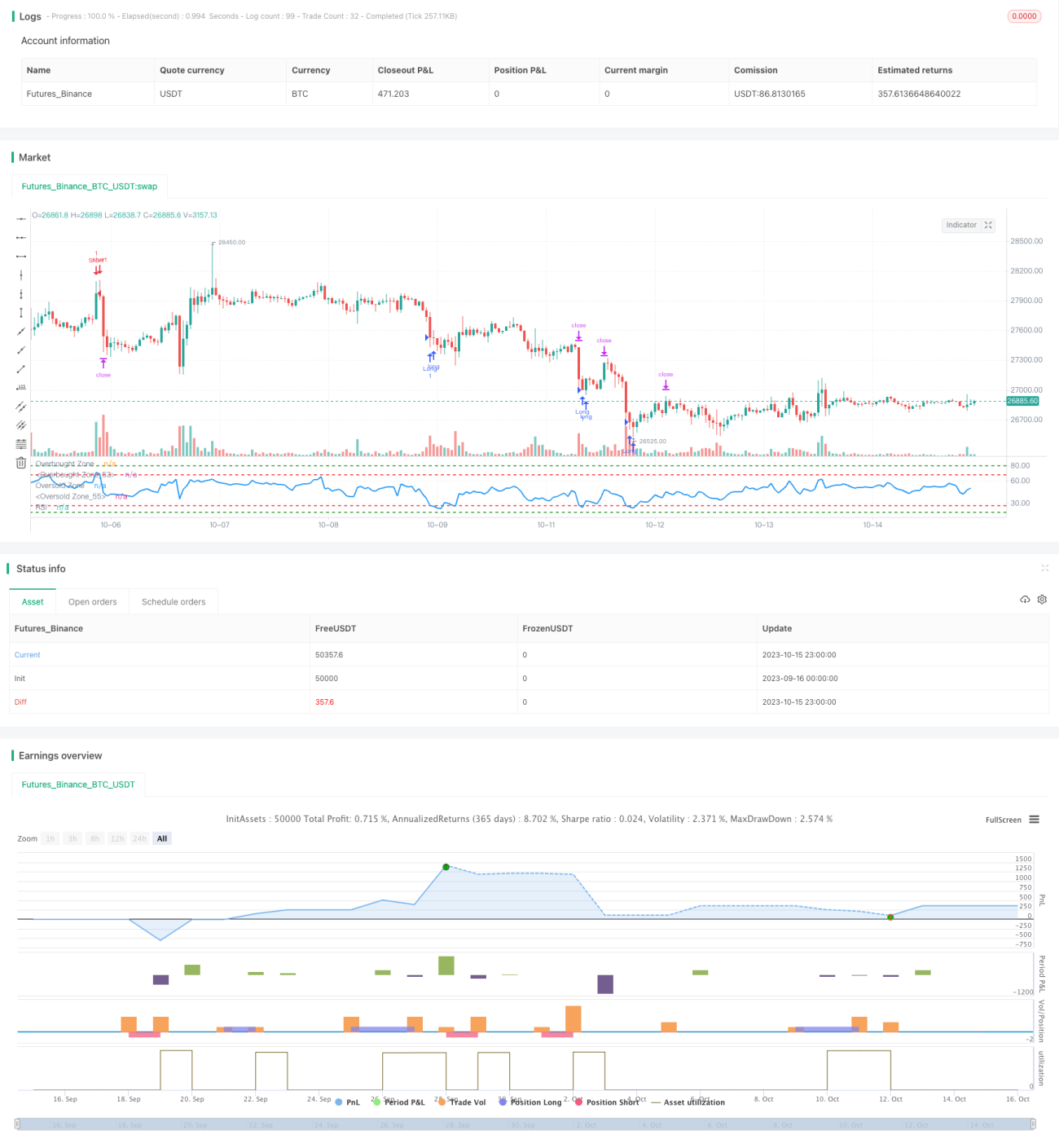

本戦略は、RSI指標が異なるゾーンを突破するのを監視することで、安値で買い高値で売ることを目的とします。RSIが低位ゾーンにあるときに買い、高位ゾーンにあるときに売ることで、買われすぎ・売られすぎ現象が発生した際に逆張りを行います。

戦略の原理

- RSIの期間を14に設定します。

- 買いシグナルのRSIゾーンを設定します。

- ゾーン1: RSI <= 27

- ゾーン2: RSI <= 18

- 売りシグナルのRSIゾーンを設定します。

- ゾーン1: RSI >= 68

- ゾーン2: RSI >= 80

- RSIが買いゾーンに入ったら、ロングエントリーします:

- RSIがゾーン1(27以下)に入った場合、1枚ロング

- RSIがゾーン2(18以下)に入った場合、さらに1枚ロング

- RSIが売りゾーンに入ったら、ショートエントリーします:

- RSIがゾーン1(68以上)に入った場合、1枚ショート

- RSIがゾーン2(80以上)に入った場合、さらに1枚ショート

- 各ポジションは固定利益確定2500pips、ストップロス5000pipsとします。

- RSIがシグナルゾーンを離れた場合、該当ポジションをクローズします。

優位性の分析

- 二重ゾーン設定により、買われすぎ・売られすぎをより明確に判断でき、反転のチャンスを逃しにくくなります。

- 固定の利益確定・ストップロスポイントを採用しているため、過度な追い上げや投げ売りを防ぎます。

- RSIは比較的成熟した買われすぎ・売られすぎ判断指標であり、他の指標よりも優位性があります。

- 本戦略のパラメータが適切に設定されていれば、トレンドの反転ポイントを効果的に捉え、超過収益を得ることができます。

リスク分析

- RSI指標が機能しない市場環境が発生し、システムが継続的にショートで損失を出す可能性があります。

- 固定の利益確定・ストップロスポイント設定が市場の変動幅と合わず、利益を得られない、または早期ストップロスが発生する可能性があります。

- ゾーン設定が不合理だと、トレード機会を逃したり、頻繁なトレードによる損失が発生する可能性があります。

- 本戦略はパラメータ最適化への依存度が高く、テスト期間とスリッページ管理に注意が必要です。

最適化の方向性

- 異なる期間のRSI指標の効果をテストできます。

- 買い・売りゾーンの数値を最適化し、さまざまな銘柄の特性に合わせることができます。

- 動的な利益確定・ストップロス方式を研究し、より効果的な利益確定と合理的なストップロスを実現できます。

- 他の指標と組み合わせて複合トレードを行い、システムの安定性を高めることを検討できます。

- 機械学習を活用してゾーンパラメータを自動最適化し、戦略のロバスト性を向上させる方法を探求できます。

まとめ

本戦略は、RSI指標の買われすぎ・売られすぎ判断原理に基づいて設計されています。二重の売買ゾーンを設定することでRSI指標の効用を発揮させ、一定の安定性を維持しつつ、市場の買われすぎ・売られすぎ現象を効果的に捉えて逆張りを行います。ただし、本戦略にはパラメータ依存性があり、銘柄ごとに最適化テストを行う必要があります。パラメータが適切に設定されれば、良好な超過収益を得ることができます。総じて、本戦略は成熟した指標を利用したシンプルで効果的な取引戦略であり、さらなる研究と最適化に値し、また定量取引戦略のアイデアを提供します。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1