累積RSIブレイクアウト戦略

概要

本戦略は、累積RSIインジケーターを利用してトレンドを識別し、RSIインジケーターの累積値が重要な閾値を突破した際に買い・売りを実行します。この戦略は市場のノイズを効果的に除去し、中長期のトレンド取引機会を捉えることができます。

戦略の原理

本戦略は主に累積RSIインジケーターに基づいて取引判断を行います。累積RSIインジケーターはRSIインジケーターの累積値であり、パラメータcumlenを設定することで、RSIインジケーターのcumlen日間の数値を累積加算して累積RSIインジケーターを取得します。このインジケーターは短期的な市場ノイズを除去することができます。

累積RSIインジケーターがボリンジャーバンドの上限を上抜けた場合、買いエントリーを行います。累積RSIインジケーターがボリンジャーバンドの下限を下抜けた場合、売り決済を行います。ボリンジャーバンドの上限・下限は長年の過去データに基づいて計算され、動的に変動する参考価格帯です。

さらに、本戦略にはトレンドフィルターオプションも追加されています。価格が100日移動平均線よりも高い場合、すなわち上昇トレンドチャネルにある場合にのみ、買いエントリーを行います。このフィルターは価格がレンジ相場にある際の誤った取引を回避します。

戦略の優位性

- 累積RSIインジケーターを活用してノイズを効果的に除去し、中長期トレンドを捉える

- トレンドフィルターを追加し、不合理な取引を回避

- 固定値ではなく、動的な参考価格帯の突破で判断

- 多くのパラメータを調整可能で、異なる市場に合わせて調整可能

- 10年間のバックテスト結果が優れており、バイ・アンド・ホールド戦略を大きく上回るリターン

戦略のリスクと改善点

- 単一指標である累積RSIのみで判断しているため、他の判断指標やフィルターを追加して総合判断する余地がある

- 固定倍率のレバレッジが高いため、ドローダウン状況に応じてレバレッジ比率を調整可能

- ロング方向のみのため、ショート機会の追加を検討可能

- パラメータの組み合わせ最適化が可能であり、市場状況によってパラメータ設定が大きく異なる

- 決済条件を充実させ、ストップロスやトレーリングストップなどの追加を検討可能

- 他の戦略と組み合わせて相乗効果を発揮することも考慮可能

まとめ

本累積RSIブレイクアウト戦略は全体的に動作がスムーズでロジックが明確であり、累積RSIインジケーターによる効果的なフィルタリングとトレンド判断により、中長期トレンドを正確に捉え、過去のバックテストでも優れた結果を示しています。しかし、パラメータ設定の調整、判断指標の追加、決済条件の充実など、さらなる最適化の余地があり、より堅牢で包括的なトレンド戦略へと発展させることができます。本戦略は斬新なアイデアであり、さらなる探求と応用に値します。

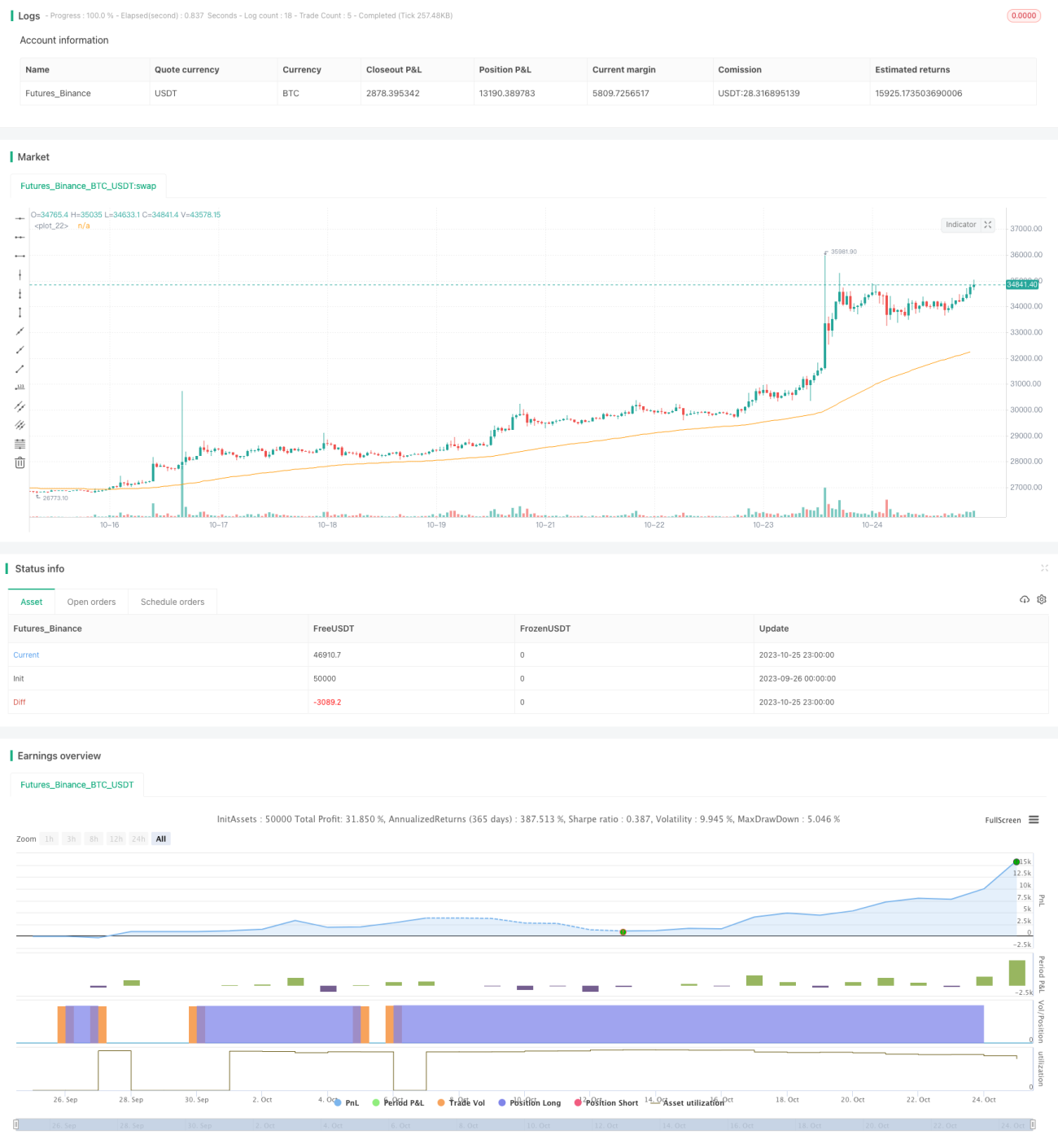

/*backtest

start: 2023-09-26 00:00:00

end: 2023-10-26 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// @version=5

// Author = TradeAutomation

- 1