反転型ボリンジャーバンドチャネル・トレンドレンジ戦略

概要

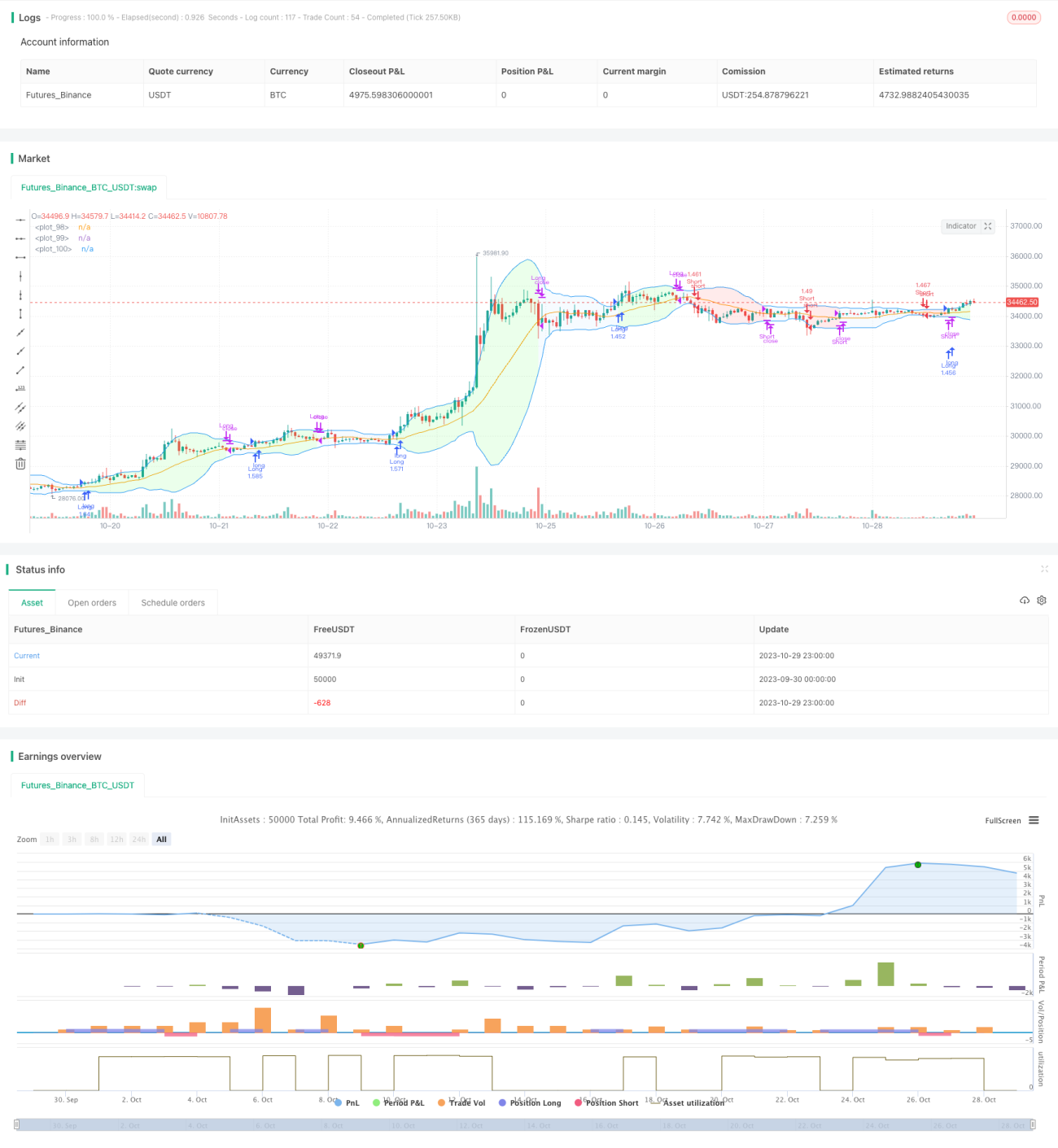

これは、ボリンジャーバンドチャネルに基づく逆張り型のレンジ・トレンド戦略です。ボリンジャーバンドの上下チャネルをトレンド判断に利用し、価格がチャネルの境界に近づいたときに反転の機会を捉えてエントリーします。

戦略の原理

本戦略は、主要なテクニカル指標としてボリンジャーバンドを使用します。ボリンジャーバンドは、n日移動平均線とその上下の変動幅で構成され、上部バンド = n日移動平均線 + m × n日標準偏差、下部バンド = n日移動平均線 - m × n日標準偏差で表されます。ここでnとmはパラメータです。

価格が上部バンドに近づくと、上昇トレンドにあるが天井に達して反転する可能性があることを示します。価格が下部バンドに近づくと、下降トレンドにあるが底を打って反転する可能性があることを示します。このとき、価格が効果的にボリンジャーバンドの上下バンドを突破した場合、反転が始まる可能性があります。

本戦略の具体的な取引ルールは以下の通りです。

-

終値がボリンジャーバンドの上部バンドを上回った場合、買いエントリー。終値がボリンジャーバンドの下部バンドを下回った場合、売りエントリー。

-

利確・損切りのシグナルとしてn日移動平均線を使用します。買いポジションの場合、終値がn日移動平均線を下回ったら利確で決済。売りポジションの場合、終値がn日移動平均線を上回ったら損切りで決済。

-

固定ロットを使用し、取引ごとの数量は固定。

-

固定比率の資金管理法を採用し、固定の損益比率と注文調整幅を設定します。固定比率の利益が達成された場合は固定幅でポジションを増やし、損失が出た場合はポジションを減らします。

優位性分析

本戦略には以下の優位性があります。

-

ボリンジャーバンドチャネルでトレンド方向を判断し、逆張り戦略を採用することで、価格が反転する可能性のある時点でエントリーし、多くの揉み合いを避けて勝率を高めます。

-

移動平均線を利確・損切りのシグナルとして使用することで、信頼性が高く、大部分の利益を確保できます。

-

固定ロット戦略はシンプルで実行しやすく、複雑な計算を必要としません。

-

固定比率の資金管理戦略は、ポジション調整を通じて利益を拡大しつつリスクをコントロールできます。

リスク分析

本戦略には以下のリスクも存在します。

-

ボリンジャーバンドの判断で誤ったシグナルが発生する可能性があり、トレンド中に逆張りで損失を出すことがあります。

-

移動平均線の遅延性により、利確が十分でない可能性があります。

-

固定ロットは市場状況に応じてポジションを調整できないため、ポジションが大きすぎたり小さすぎたりする問題があります。

-

固定比率の資金管理方法はポジション調整幅が大きく、損失が拡大する可能性があります。

対策:ボリンジャーバンドのパラメータを最適化しシグナルの精度を向上させる。他のインジケーターと組み合わせてトレンドを判断する。固定ロットサイズを適切に小さくする。固定比率資金管理のポジション調整幅を小さくする。

最適化の方向性

本戦略は以下の点で最適化が可能です。

-

ボリンジャーバンドのパラメータ(n値、m値など)を最適化し、チャネル判断の精度を高める。

-

MACD、KDなどの他のインジケーターを追加し、ボリンジャーバンドの誤シグナルを回避する。

-

固定ロットを動的ロットに変更し、市場状況に応じて柔軟にポジションを調整する。

-

固定比率資金管理法のポジション調整幅を小さくし、資金曲線を最適化する。

-

ストップロス戦略(トレーリングストップ、レンジブレイクアウトストップなど)を追加し、リスクをさらに抑制する。

-

パラメータ最適化を実施し、自動的にパラメータ組み合わせを最適化して、最適なパラメータで戦略を改善する。

まとめ

本戦略は全体として、典型的なボリンジャーバンド逆張り戦略です。ボリンジャーバンドでトレンド反転点を判断し、移動平均線で利確・損切りを設定し、固定ロットと固定比率資金管理でリスクをコントロールします。従来のボリンジャーバンド戦略と比較して、逆張り戦略であるため、理論上は一部の揉み合いを避け、利益を得る確率を高められます。しかし、ボリンジャーバンドや移動平均線などのインジケーター自体に欠点があるため、実際に運用する際にはさらなる最適化が必要であり、戦略をパラメータ化し取引リスクを低減することが求められます。

- 1