モメンタムブレイクアウト識別戦略

概要

本戦略は、急騰する株式を識別し、新高値を更新したタイミングで買い建て(ロング)を行い、固定パーセンテージの利益確定(利確)によって利益を得る手法です。トレンドフォロー型の戦略に分類されます。

原理

本戦略は主に以下の2つの指標に基づいています。

-

高速RSI: 直近3本のローソク足の値上がり・値下がり変動を計算し、価格のモメンタムを判断します。高速RSIが10を下回った場合、株価が過度に売られた状態(売られ過ぎ)とみなします。

-

実体フィルター: 直近20本のローソク足の実体の平均サイズを計算し、価格の実体が平均実体の2.5倍を超えた場合、有効なブレイクアウトとみなします。

高速RSIが10未満であり、かつ実体フィルターが有効となった場合に、買い建て(ロング)エントリーを行います。その後、20%の固定利確ポイントを設定し、価格がエントリー価格 × (1 + 利確比率) を超えた時点でポジションを決済し利益を確定します。

本戦略の利点は、トレンド開始時のブレイクアウトのチャンスを捉えられることです。高速RSIで底値圏を判断し、実体フィルターで偽のブレイクアウトを回避します。固定利確方式で1回ごとの利益を確定することで、相場のトレンドを継続的に捉えることができます。

優位性分析

本戦略には以下のような優位性があります。

- 高速RSIを利用して底値の売られ過ぎ領域を判断することで、エントリーの精度を高めることができます。

- 実体フィルターにより、値動きの乱高下(ノイズ)による偽のブレイクアウトを回避できます。

- 固定パーセンテージの利確方式を採用することで、継続的に利益を得て相場のトレンドを捉えることができます。

- 戦略ロジックはシンプルかつ明確であり、理解と実装が容易です。

- コード構造が洗練されており、拡張性が高いため、戦略の最適化が容易です。

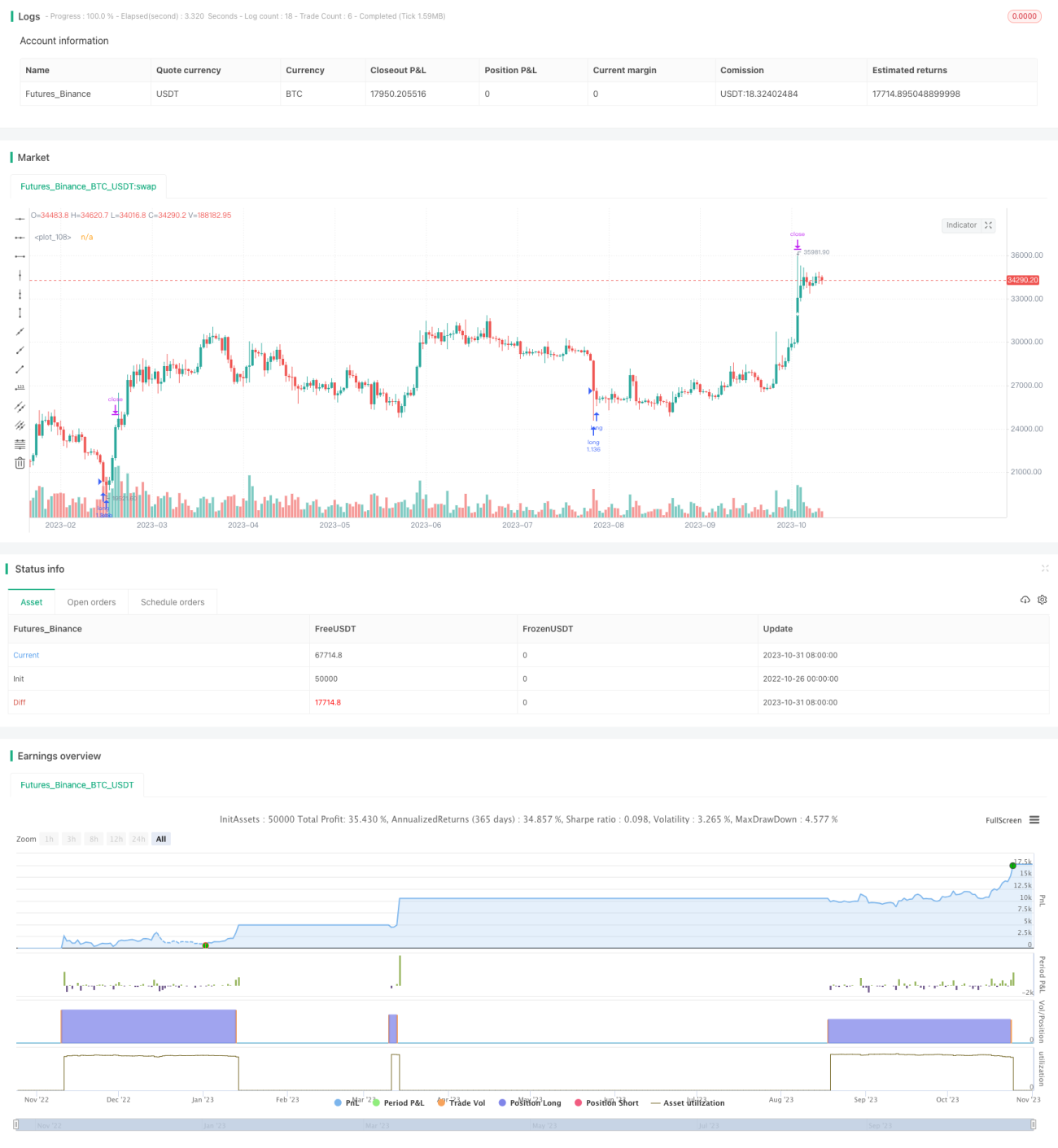

- バックテスト期間において、本戦略は安定したプラスのリターンを獲得し、勝率も高いです。

リスク分析

本戦略には以下のようなリスクも存在するため注意が必要です。

- ストップロス(損切り)の仕組みがないため、1回の損失が拡大するリスクがあります。

- 固定利確ポイントの設定が適切でない場合、早期利確や利確ポイントが深すぎる可能性があります。

- 相場がレンジ(もみ合い)状態の場合、連続した小さな損失が発生しやすくなります。

- 信用取引のコスト(金利など)が考慮されていないため、実運用ではリターンが減少します。

- 戦略パラメータの最適化が不十分であり、異なる銘柄ごとにパラメータの調整が必要です。

改善の方向性

本戦略は以下の観点から改善が可能です。

- ストップロスの仕組みを追加し、1回あたりの損失を制御します。

- 利確ポイントを最適化し、トレンドに動的に追従できるようにします。

- ブレイクアウトの判断指標を最適化し、エントリーの精度を高めます。

- ポジションサイズ管理モジュールを追加し、証拠金の使用率を最適化します。

- 銘柄ごとのパラメータ最適化モジュールを追加し、異なる銘柄のパラメータを自動最適化します。

- フィルター条件を追加し、相場が乱高下している場合の損失を回避します。

- ポジション平均コスト管理モジュールの追加を検討します。

まとめ

本戦略は全体として非常にシンプルで洗練されたトレンドフォロー型の戦略です。高速RSIで売られ過ぎを判断し、実体フィルターで有効なブレイクアウトを確定し、固定利確ポイントで安定した利益を得ます。改善の余地はいくつかありますが、本戦略は機敏に反応し、相場が急変する場面を捉えるのに適しており、非常に実用的なトレード戦略です。継続的な最適化により、強力で信頼性の高い長期保有戦略になると考えられます。

/*backtest

start: 2022-10-26 00:00:00

end: 2023-11-01 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// this is based on https://www.tradingview.com/v/PbQW4mRn/

strategy(title = "ONLY LONG V4 v1", overlay = true, initial_capital = 1000, pyramiding = 1000,

calc_on_order_fills = false, calc_on_every_tick = false, default_qty_type = strategy.percent_of_equity, default_qty_value = 50, commission_value = 0.075)- 1