高低指標と移動平均線の組み合わせ戦略

概要

本戦略は主に高安指標、移動平均線指標とスーパートレンド指標を組み合わせ、市場のトレンドを判断してポジションを構築します。

戦略の原理

-

高安指標により、直近の一定期間内に価格が新高値または新安値を更新したかどうかを判断し、スコアを累積します。スコアが上昇するときは、買い勢力が強まっていることを示します。スコアが下降するときは、売り勢力が強まっていることを示します。

-

移動平均線指標により、価格が下から上への階段状の上昇トレンドにあるか、または上から下への階段状の下降トレンドにあるかを判断します。移動平均線が階段状に上昇している場合は買い勢力の強まりを、階段状に下降している場合は売り勢力の強まりを示します。

-

高安指標と移動平均線指標の判断結果を組み合わせて市場トレンドを特定し、さらにスーパートレンド指標の方向性と併せてポジション構築の機会を探ります。具体的には、高安指標と移動平均線指標がともに買い勢力の強まりを示し、かつスーパートレンド指標が下向きの場合にロングポジションを構築します。高安指標と移動平均線指標がともに売り勢力の強まりを示し、かつスーパートレンド指標が上向きの場合にショートポジションを構築します。

戦略のメリット

-

高安指標は価格の動きと勢力変化を効果的に判断でき、移動平均線指標は価格トレンドを効果的に判断できるため、両者を組み合わせることで市場の方向性をより正確に把握できます。

-

スーパートレンド指標を組み合わせてポジションを構築することで、早すぎるエントリーや遅すぎるエントリーを回避できます。スーパートレンド指標は価格の反転ポイントを効果的に識別できます。

-

複数の指標が相互に検証し合うことで、誤信号を減らせます。

戦略のリスク

-

高安指標と移動平均線指標が誤ったシグナルを発した場合、損失を伴うポジション構築につながる可能性があります。

-

参加度が低い場合やスーパートレンド指標のパラメータ設定が不適切な場合、誤ったシグナルが発生する可能性があります。

-

トレンドの反転が速すぎる場合やストップロスの設定が不適切な場合、大きな損失が発生する可能性があります。

-

指標パラメータの最適化やストップロスポイントの調整などにより、リスクを低減できます。

戦略の最適化

-

異なる種類の移動平均線指標をテストし、最適なパラメータの組み合わせを探すことができます。

-

高安指標と移動平均線指標のパラメータを最適化し、シグナルをより安定かつ信頼性の高いものにできます。

-

MACDやKDなどの他の指標を組み合わせて検証し、誤信号を減らせます。

-

機械学習アルゴリズムを組み合わせて、パラメータやシグナルの重みを自動最適化できます。

-

センチメント分析などを組み合わせて市場の熱度を判断し、低熱度の銘柄の取引を避けられます。

まとめ

本戦略は高安指標と移動平均線指標によって市場のトレンドと勢力を判断し、さらにスーパートレンド指標でシグナルをフィルタリングし、買い勢力と売り勢力が拮抗しスーパートレンド指標が反転した時点でポジションを構築することで、低リスクの取引を実現します。戦略の利点は複数指標による検証とタイムリーなポジション構築にあり、リスクを効果的にコントロールできます。問題点としては、誤信号とトレンド判断ミスがあります。パラメータ最適化、ストップロス設定、シグナルフィルタリングなどの様々な方法で改善し、戦略をより堅牢で信頼性の高いものにできます。

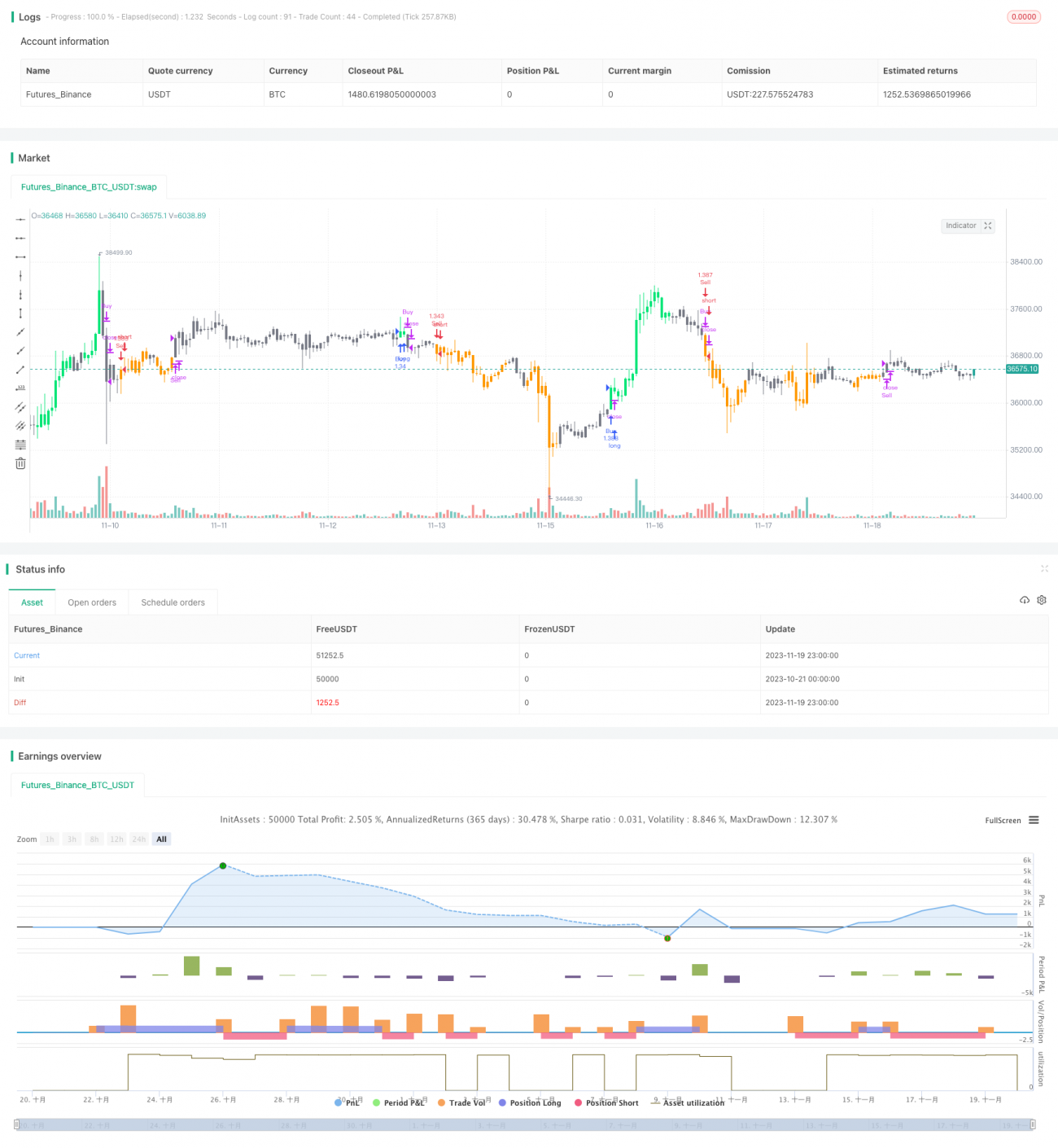

/*backtest

start: 2023-10-21 00:00:00

end: 2023-11-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © HeWhoMustNotBeNamed

//@version=4- 1