EMA線に基づく取引戦略

概要

本戦略は、異なる周期の4本のEMA移動平均線を使用し、その配列順序に基づいて取引シグナルを生成します。これは信号機の赤・黄・青の3色表示灯に似ているため、「信号機取引戦略」と名付けられました。トレンドと反転の両方の観点から市場を総合的に判断し、取引判断の精度向上を目指します。

戦略の原理

-

短期線(8期間)、中期線(14期間)、長期線(16期間)の3本のEMA移動平均線を設定し、さらに1本の長期(100期間)EMA移動平均線をフィルターとして追加します。

-

短期・中期・長期の3本の移動平均線の配列順序と、フィルターとのクロス状況を判断し、買いと売りのタイミングを決定します。

-

短期線が中期線を上抜ける、または中期線が長期線を上抜ける場合、買いシグナルと判断します。

-

中期線が短期線を下抜ける場合、買いポジションの手仕舞いシグナルと判断します。

-

短期線が中期線を下抜ける、または中期線が長期線を下抜ける場合、売りシグナルと判断します。

-

中期線が短期線を上抜ける場合、売りポジションの手仕舞いシグナルと判断します。

-

-

短期・中期・長期の3本の移動平均線の順序からトレンドの方向性と強さを判断し、移動平均線とフィルターのクロスから反転ポイントを判断することで、トレンドフォローと反転キャッチの有機的な組み合わせを実現します。

優位性分析

本戦略は、トレンドフォローと逆張り取引の長所を統合し、市場の機会をより的確に捉えることができます。主な優位性は以下の通りです。

- 複数のEMA移動平均線を使用することで、判断力が高まり、偽シグナルが減少します。

- 買い・売りの条件を柔軟に設定できるため、取引機会を逃しにくくなります。

- 長期と短期の移動平均線を立体的に使用することで、総合的な判断力が向上します。

- 利食い・損切り条件をカスタマイズできるため、リスク管理が適切に行えます。

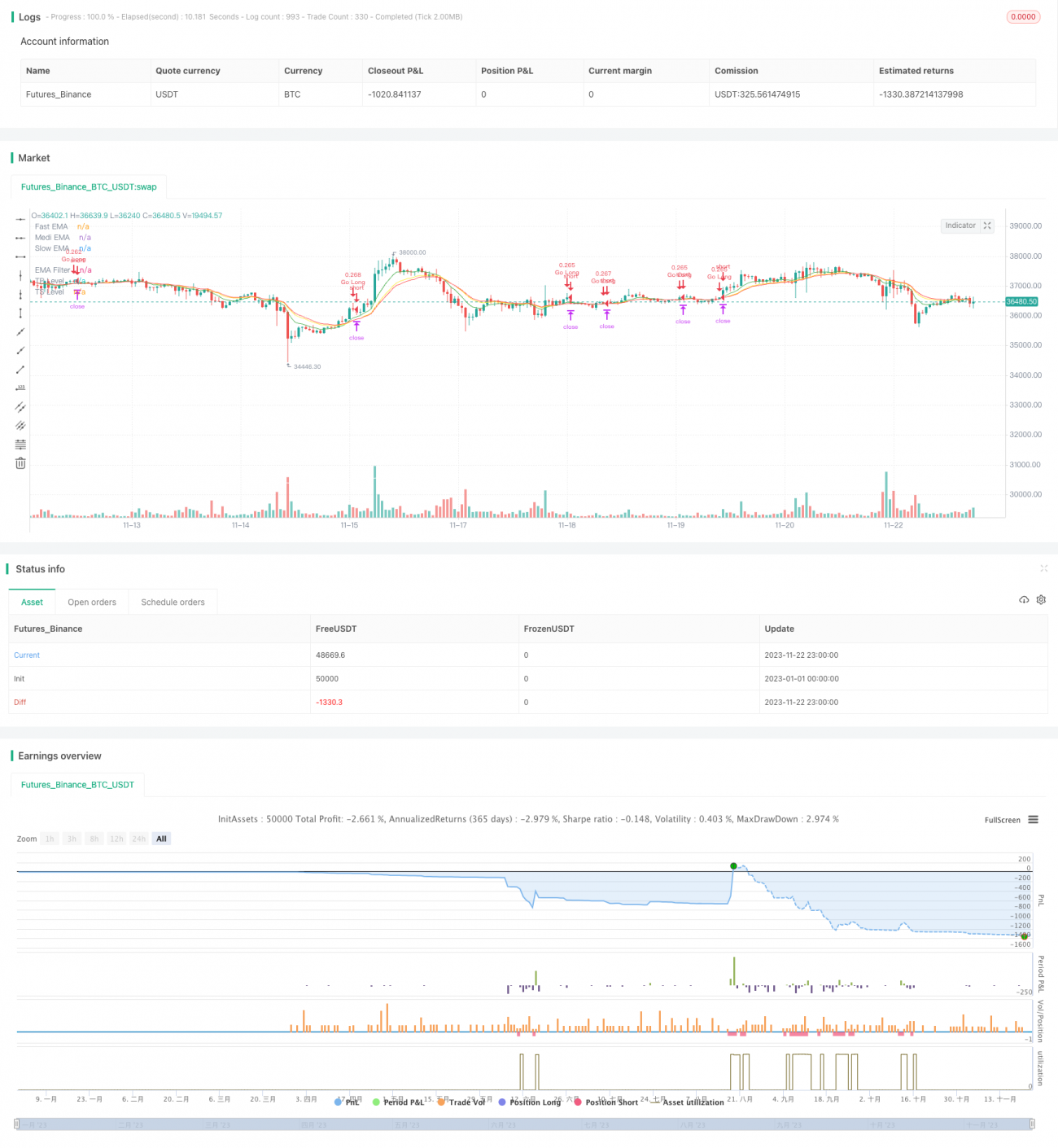

パラメータの最適化により、本戦略はより多くの銘柄に適応可能となり、バックテストにおいて高い収益性と安定性を示しています。

リスク分析

本戦略の主なリスクは以下の通りです。

- 複数のEMA移動平均線の配列順序が乱れると、判断が難しくなり、取引の躊躇が生じる可能性があります。

- 市場の異常変動による偽シグナルを効果的にフィルターできない場合、大きなレンジ相場で損失が発生する可能性があります。

- パラメータ設定が不適切な場合、利食い・損切り条件が緩すぎたり厳しすぎたりして、利益を逃したり過度な損失を被る可能性があります。

パラメータの最適化、損切り水準の設定、慎重な取引などにより、戦略の安定性をさらに高め、リスクをコントロールすることを推奨します。

最適化の方向性

本戦略の主な最適化の方向性は以下の通りです。

- EMA移動平均線の周期パラメータを調整し、より多くの銘柄に適応させる。

- MACDやボリンジャーバンドなどの他の指標を追加し、判断精度を高める。

- 利食い・損切りの比率を最適化し、リスクとリターンの最適なバランスを図る。

- ATRストップロスなどの適応型ストップロスメカニズムを追加し、下振れリスクをさらに抑制する。

多角的なパラメータ調整とリスク管理手法の導入により、戦略の安定性と収益性を継続的に向上させることができます。

まとめ

本信号機取引戦略は、トレンドフォローと反転判断を統合し、4本のEMA移動平均線を用いて取引シグナルを形成します。パラメータの最適化により多くの銘柄に適応し、バックテストにおいて高い収益性を示しています。今後、さらなるリスク管理と多様な指標の導入により、安定して効率的な定量取引戦略となることが期待されます。

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © maxits

// 4HS Crypto Market Strategy- 1