概要

二重シグナル定量反転戦略は、123反転戦略とアクセラレーターオシレーター指標を組み合わせることで、トレンド反転を判断し、より正確な取引シグナルを取得します。この戦略は主に株価指数、外国為替、貴金属、エネルギー銘柄の短期および中期取引に使用されます。

戦略の仕組み

この戦略は、2つの独立したコードロジックで構成されています。

第1部は123反転戦略です。その反転シグナル判断の原理は次のとおりです。終値が2日連続で前日の終値を下回り、かつ9日STOCH指標のK線がD線を下回った場合に買いシグナルを生成します。終値が2日連続で前日の終値を上回り、かつ9日STOCH指標のK線がD線を上回った場合に売りシグナルを生成します。

第2部はアクセラレーターオシレーター指標です。この指標は、絶対価格オシレーターとその5期間移動平均線の差を計算することで、絶対価格オシレーターの変化速度を反映し、トレンド反転点を事前に判断することができます。

最後に、この戦略は2つの指標のシグナルを組み合わせます。両指標のシグナルが同方向(ダブル買いまたはダブル売り)の場合、その方向の取引シグナルを出力します。両指標のシグナルが一致しない場合は、ゼロシグナルを出力します。

優位性分析

この戦略は二重の指標判断を組み合わせることで、一定の偽シグナルをフィルタリングでき、シグナルの精度と信頼性が向上します。同時に、絶対価格オシレーターが変化の加速度を反映する特性を活かし、潜在的なトレンド反転点を事前に捉えることで、より大きな利益空間を確保できます。

リスク分析

この戦略の最大のリスクは、指標がシグナルを発する前に価格が明確に反転してしまい、最適なエントリーポイントを逃す可能性があることです。また、相場が激しく変動する場合、指標パラメータの最適化調整が必要となります。

エントリーポイントのリスクに対しては、より多くの反転指標を組み合わせてシグナルの信頼性を確保できます。パラメータ最適化の問題に対しては、動的調整メカニズムを構築してパラメータの妥当性を確保できます。

最適化の方向性

この戦略は以下の点で最適化が可能です。

-

フィルタリング条件を追加し、高ボラティリティ局面での誤シグナルを回避する

-

より多くの反転指標と組み合わせ、多重検証メカニズムを形成する

-

パラメータ適応メカニズムを構築し、指標パラメータを動的に調整する

-

ストップロス戦略を最適化し、1回の損失をコントロールする

まとめ

二重シグナル定量反転戦略は、二重検証によってシグナルの正確性を高め、市場の重要な反転ポイントを捉えるのに役立ちます。同時に、指標の遅延やパラメータの効力低下といったリスクに注意し、戦略を継続的に検証・最適化して、変化する市場環境に適応できるようにする必要があります。この戦略は、一定の定量取引経験を持つ投資家に適しています。

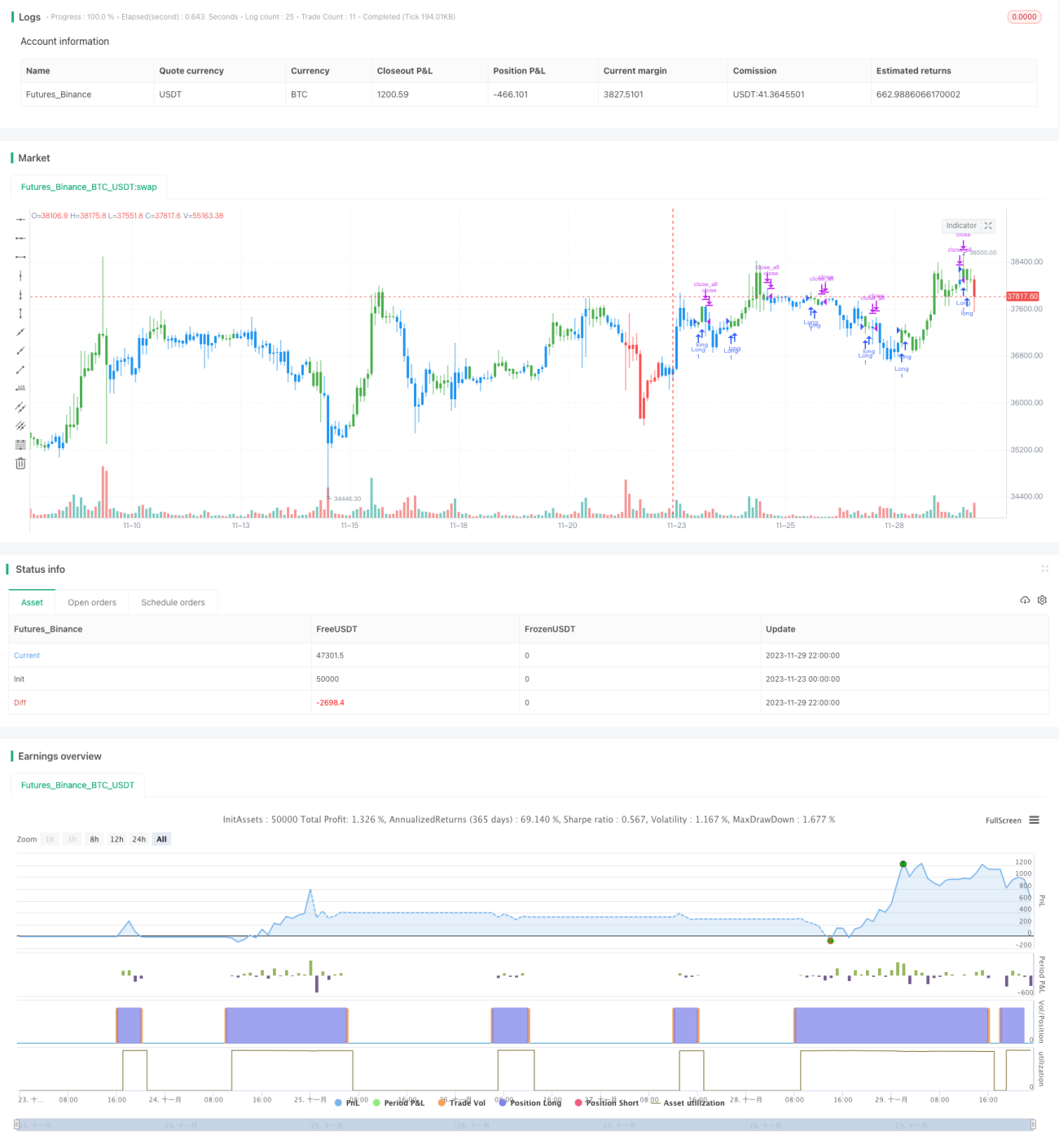

/*backtest

start: 2023-11-23 00:00:00

end: 2023-11-30 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 25/04/2019

// This is combo strategies for get - 1