動的ボラティリティキャプチャRSI-ボリンジャーバンド戦略

概要

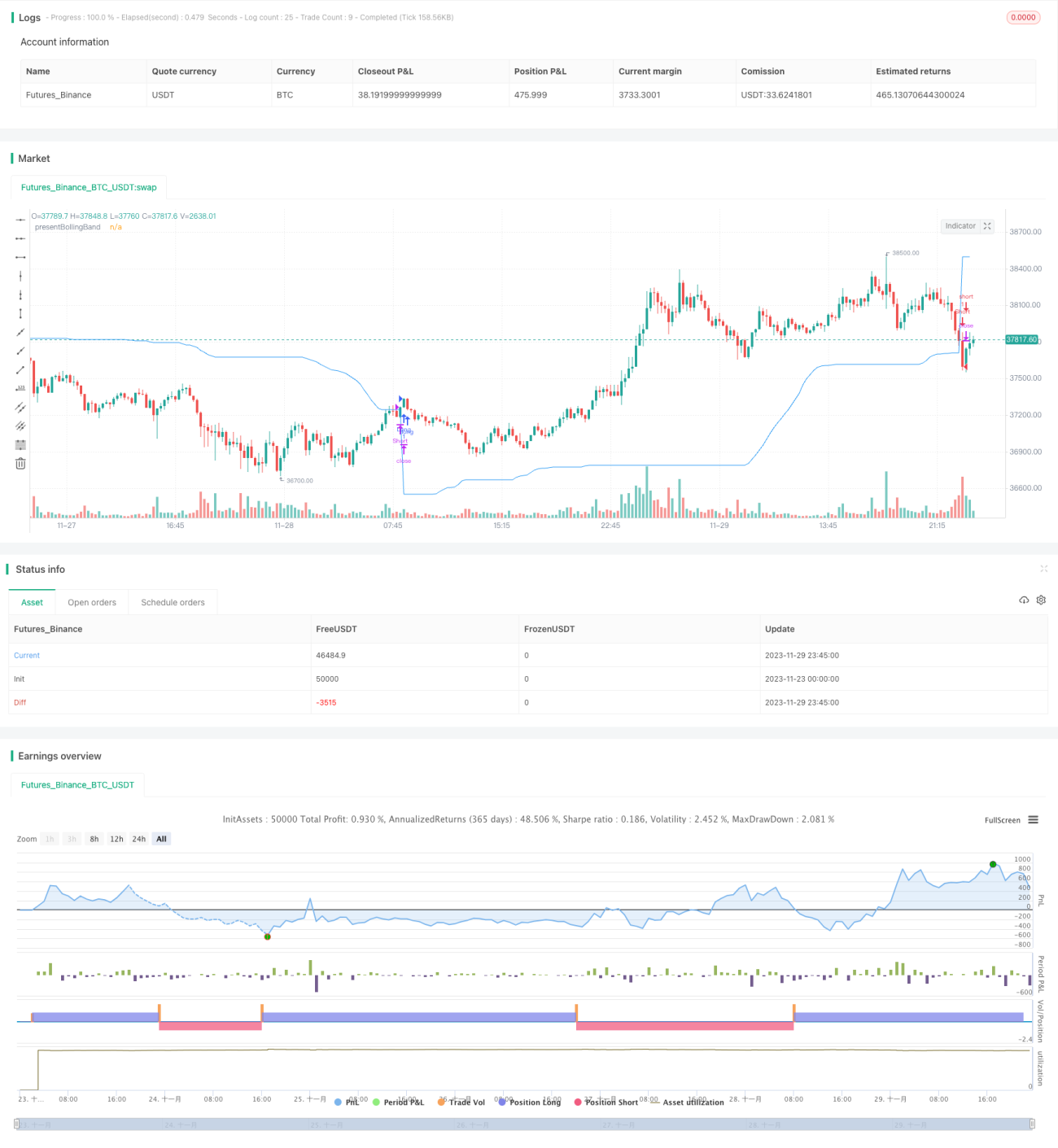

ダイナミック・ボラティリティ・キャプチャRSI-ボリンジャーバンド戦略は、ボリンジャーバンド(BB)、相対力指数(RSI)、および単純移動平均線(SMA)の概念を統合した取引戦略です。この戦略のユニークな点は、終値がアッパーバンドとロワーバンドの間で計算される動的水準に基づいていることです。この独自の機能により、戦略は市場のボラティリティと価格変動に適応できます。

仮想通貨市場や株式市場はボラティリティが非常に高いため、ボリンジャーバンド戦略に適しています。RSIは、しばしば投機的となるこの市場の買われ過ぎ・売られ過ぎの状況を特定するのに役立ちます。

戦略の仕組み

ダイナミック・ボリンジャーバンド: まず、ユーザーが定義した期間と乗数に基づいて、アッパーバンドとロワーバンドのボリンジャーバンドを計算します。次に、ボリンジャーバンドと終値を組み合わせて、presentBollingBandの値を動的に調整します。最後に、価格が present BollingBand を上抜けたときにロングシグナルが発生し、価格が present BollingBand を下抜けたときにショートシグナルが発生します。

RSI: ユーザーがRSIを使用してシグナルを生成することを選択した場合、戦略はRSIとそのSMAも計算し、それらを使用して追加のロングおよびショートシグナルを生成します。「RSIを使用してシグナルを生成」オプションがtrueに設定されている場合のみ、RSIベースのシグナルが使用されます。

次に、戦略は選択された取引方向を確認し、それに応じてロングまたはショートポジションをエントリーします。取引方向が「両方向」に設定されている場合、戦略はロングポジションとショートポジションの両方を同時に保有できます。

最後に、終値が present BollingBand を上抜けたときにロングポジションをクローズし、終値が present BollingBand を下抜けたときにショートポジションをクローズします。

優位性分析

この戦略は、ボリンジャーバンド、RSI、SMAインジケーターの利点を組み合わせることで、市場のボラティリティに適応し、変動を動的に捉え、買われ過ぎ・売られ過ぎの状況で取引シグナルを生成します。

RSIインジケーターはボリンジャーバンドの取引シグナルを補完し、レンジ相場での誤エントリーを回避します。ロング専用、ショート専用、または両方向の取引を選択でき、様々な市場環境に適応します。

パラメータはカスタマイズ可能で、個人のリスク許容度に合わせて調整できます。

リスク分析

この戦略はテクニカル指標に依存しており、ファンダメンタルズによる大きな転換には対応できません。

ボリンジャーバンドのパラメータ設定が適切でない場合、取引シグナルが過剰またはまばらに発生する可能性があります。

両方向取引はリスクが高まるため、逆方向のショートでの損失に注意が必要です。

リスク管理のためにストップロスを併用することを推奨します。

最適化の方向性

-

他の指標(例:MACD)と組み合わせてシグナルをフィルタリングする。

-

ストップロス戦略を追加する。

-

ボリンジャーバンドとRSIのパラメータを最適化する。

-

異なる取引銘柄や時間足に応じてパラメータを調整する。

-

実運用での最適化を行い、実際の状況に合わせてパラメータを調整する。

まとめ

ダイナミック・ボラティリティ・キャプチャRSI-ボリンジャーバンド戦略は、テクニカル指標主導の戦略であり、ボリンジャーバンド、RSI、SMAインジケーターの利点を組み合わせ、ボリンジャーバンドを動的に調整することで市場の変動を捉えます。この戦略はカスタマイズと最適化の余地が大きい一方で、ファンダメンタルズの変化を予測することはできません。実運用で効果を検証し、必要に応じてパラメータを調整したり、他の指標を追加して併用することでリスクを低減することを推奨します。

- 1