ダブル移動平均線クロスオーバー戦略

概要

ダブル移動平均線クロストレンド戦略は、移動平均線に基づく取引戦略です。高速線EMAと低速線SMAのクロスを買いシグナルおよび売りシグナルとして使用し、MACDインジケーターのダイバージェンスを組み合わせてシグナルをフィルタリングします。本戦略は価格、トレンド、モメンタムなど複数の要素を考慮し、比較的完成度の高い取引システムを形成しています。

戦略の原理

本戦略ではEMAとSMAの2本の移動平均線を使用します。EMAの期間は200日、SMAの期間は100日です。価格が上昇して両方の移動平均線を突破したときに買いシグナルが発生し、価格が下落して両方の移動平均線を突破したときに売りシグナルが発生します。これにより、もみ合い相場や短期調整を効果的にフィルタリングできます。

シグナルの信頼性をさらに高めるため、MACDインジケーターも導入しています。価格がEMAとSMAを突破してシグナルが形成された際、MACDの高速線が低速線を下から上に抜け、かつMACDの棒グラフが0軸より上にある場合にのみ、真の買いシグナルがトリガーされます。逆に、MACDの高速線が低速線を上から下に抜け、かつMACDの棒グラフが0軸より下にある場合にのみ、真の売りシグナルがトリガーされます。

さらに、ストップロスと利確も設定されています。ポジションをオープンした後、ユーザーが設定した比率に基づいてストップロスと利確ポイントが計算・設定されます。これにより、1回の取引におけるリスクを効果的に管理できます。

総じて、本戦略は複数のインジケーターを総合的に考慮し、売買シグナルに厳格なフィルター条件を設定し、ストップロス・利確によるリスク管理を採用することで、比較的厳格で完成度の高い取引システムを構築しています。

優位性分析

ダブル移動平均線クロストレンド戦略には以下のような利点があります。

-

複数のインジケーターを組み合わせ、価格・トレンド・モメンタムを総合的に評価し、シグナルに厳格なフィルターを設定することで、偽シグナルを効果的に回避し、シグナルの信頼性を高めます。

-

異なるパラメーターの2本の移動平均線を使用することで、市場トレンドをより適切に識別し、もみ合い相場をフィルタリングできます。高速なEMAラインは価格変動に迅速に追随し、低速なSMAラインは長期的なトレンドを判断します。2本の移動平均線の組み合わせにより、より効果的な使用が可能です。

-

MACDインジケーターの各パラメーターは市場の特性に応じて調整可能であり、柔軟性が高いです。MACDの設定により、取引シグナルが価格・トレンド・モメンタムのすべてのサポートを得られることが保証され、高い実用価値を持ちます。

-

ストップロスと利確ポイントを設定することで、1回の取引の損失を最大限に抑え、過大な損失のリスクを回避します。適切な比率での利確設定により、利益を確定し、利益確定後に市場リスクへのエクスポージャーを低減できます。

-

本戦略のパラメーターは柔軟に設定可能であり、最適化結果に基づいて調整できるため、実用性が非常に高いです。さまざまな市場やパラメーターのテストによる最適化の余地が大きくあります。

リスク分析

ダブル移動平均線クロストレンド戦略には以下のようなリスクも存在します。

-

株価が激しく変動する局面では、EMAとSMAが誤ったクロスを複数回発生させ、取引シグナルが頻繁に開閉する可能性があります。これにより、取引頻度と手数料が増加します。

-

MACDインジケーターは、特に方向感が不明瞭なもみ合い相場において、偽のブレイクアウトを発生させる可能性があります。このような場合、シグナルは信頼できず、不要な損失を生む可能性があります。

-

ストップロスの位置と比率の設定は損益結果に大きく影響します。ストップロスが小さすぎると、ポジションが拘束されるリスクがあり、大きすぎると1回の損失が過大になる可能性があります。最適なパラメーターを見つけるには十分なテストが必要です。

-

移動平均線はトレンドフォローインジケーターであり、価格が急反転した場合、その指示効力は低下します。戦略がストップロスを実行する前に価格反転に遭い、大きな損失を被る可能性があります。

対応する解決策は以下のとおりです。

-

激しいもみ合い相場に対しては、移動平均線のパラメーターを適宜調整し、より低い期間のEMAとSMAを使用することでクロス回数を減らします。

-

MACDのゼロ軸を上下にブレイクするフィルター条件を追加することで、偽のブレイクアウトをある程度削減できます。また、KDJやボリンジャーバンドなどの他のインジケーターを追加で組み合わせることも検討できます。

-

ストップロスの位置と比率の設定は、十分なバックテストと最適化を行い、最適なパラメーターを見つける必要があります。その上で、継続的な監視と動的調整も考慮します。

-

価格の急反転を識別するメカニズムを設定できます。異常な反転が検出された場合、ポジションを縮小するか、戦略を一時停止するなどの緊急措置を講じてリスクエクスポージャーを抑制します。

最適化の方向性

ダブル移動平均線クロストレンド戦略には、さらなる最適化の余地があり、主に以下の点が考えられます。

-

より多くのインジケーターとの組み合わせをテストし、優れたパラメーターを探求します。例えば、ボリンジャーバンドを導入し、ボラティリティの影響を考慮するなど。

-

移動平均線の期間パラメーターを最適化し、異なる市場条件下での最適なパラメーター組み合わせを見つけます。パラメーターのローリング最適化も選択肢の一つです。

-

より科学的で合理的な利確・ストップロス戦略を設定します。例えば、トレーリングストップロスを導入したり、過去の統計結果に基づいて動的なリスクリワード比を設定するなど。これにより戦略の安定性をさらに向上させることができます。

-

価格の異常反転を自動的に識別し、緊急対応する仕組みを構築します。極端な相場では積極的にポジションを縮小するか戦略を一時停止し、巨額の損失を回避します。

-

取引対象を拡大します。例えば、為替や暗号通貨などの他の資産クラスに適用します。異なる銘柄でのパラメーターの頑健性をテストし、戦略の適用範囲を広げます。

-

資金管理戦略の最適化。例えば、定額取引や固定比率ポジションなど。1回の取引のリスクを制御し、全体の資金曲線をより安定させます。

まとめ

ダブル移動平均線クロストレンド戦略は、複数の要素を総合的に考慮し、取引シグナルを発する際に価格・トレンド・モメンタムの各インジケーターのサポートを必要とすることで、シグナルの信頼性を確保しています。また、トレーリングストップロス・利確を採用し、1回の取引のリスクを効果的に管理します。パラメーターの設定が柔軟で実用性が高く、自動取引に適しています。

しかし、どの戦略も完璧ではありません。本戦略の適用においても、頻繁な取引、偽のブレイクアウト、ストップロス位置の設定などの課題に直面します。これらに対処するためには、パラメーターの組み合わせの最適化、新しいテクニカルインジケーターの導入、ストップロスメカニズムの改善など、多角的なアプローチが必要であり、戦略の堅牢性と収益性をさらに高めることが求められます。

総じて、ダブル移動平均線クロストレンド戦略は、比較的完成度の高い厳格な取引システムを形成しています。今後の研究と応用において、継続的な最適化と改良を通じて、本戦略はさらに実戦的な価値を発揮することが期待されます。

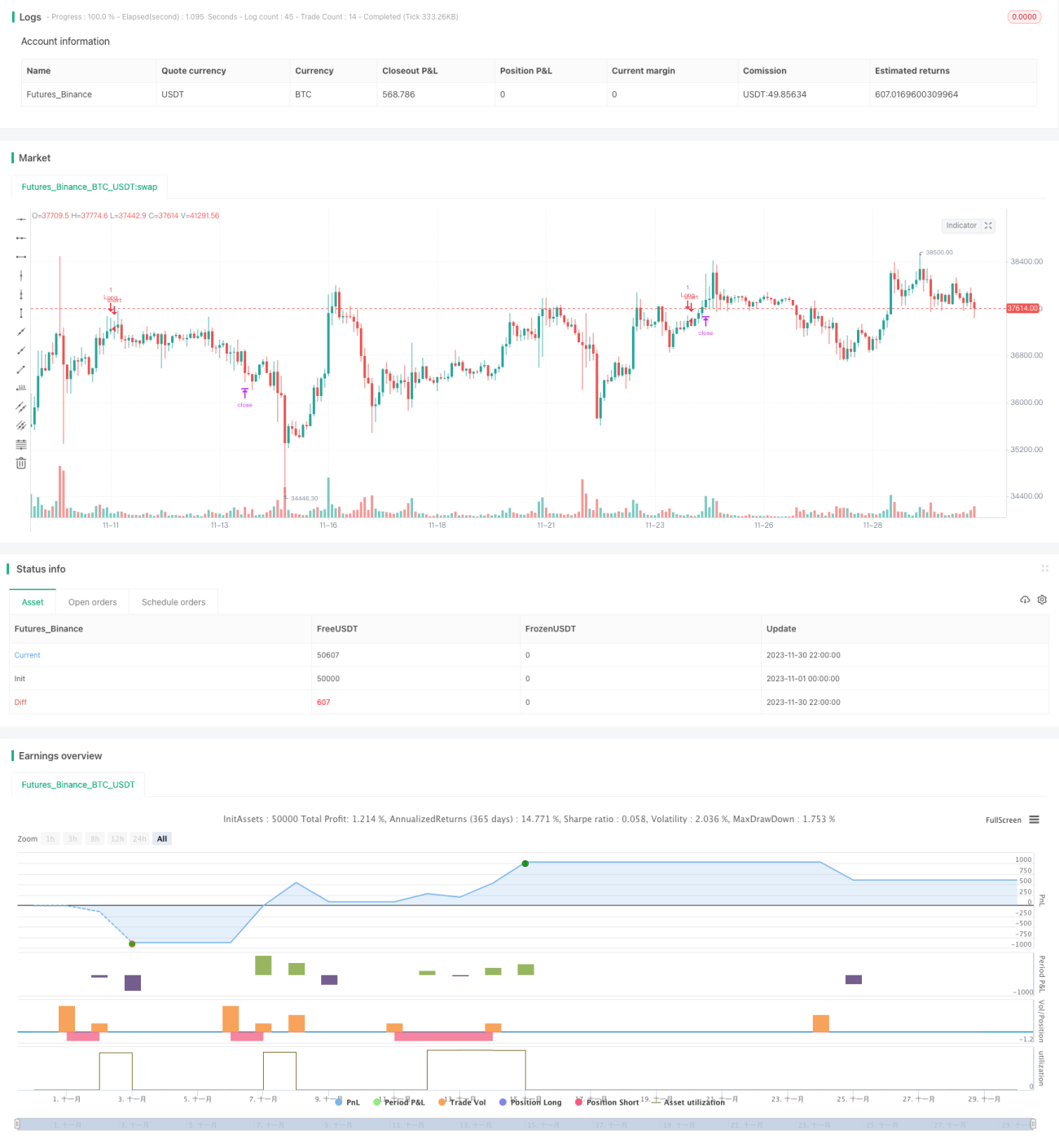

/*backtest

start: 2023-11-01 00:00:00

end: 2023-11-30 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// Hi,

// This is my first strategy made by myself(except for the MACD indicator). I'm publishing this to get myself out there and for some newer people to see how a basic strategy works. All credits go to Zen&TheArtofTrading, for teaching me almost everything I know about Pinescript

// The strategy is basically an MACD crossover trend strategy. If the MACD line crosses the signal line upward, above the zero point of the histogram, while the price is above 200 EMA and 100 SMA it's a buy signal- 1