Dual-factor Cycle Trading Strategy

Overview

The dual-factor cycle trading strategy is a quantitative trading strategy. It combines two different types of technical indicators to generate trading signals and track market trends for excess returns.

The advantage of this strategy is that it can find trading opportunities by combining different factors and dual confirmation can improve signal reliability and reduce the probability of erroneous trades. At the same time, the strategy takes full advantage of cycle trading, namely timely stop loss and reverse opening positions, which can effectively control risks.

Strategy Principles

The strategy consists of two parts:

-

123 Reversal Strategy

This strategy comes from the book "How I Tripled My Money in the Futures Market" by Ulf Jensen. Its trading logic is: when the closing price is higher than the previous closing price for two consecutive days, and the 9-day slow K-line is lower than 50, go long; when the closing price is lower than the previous closing price for two consecutive days, and the 9-day fast K-line is higher than 50, go short. -

Support/Resistance Lookback Strategy

This strategy generates signals by judging whether prices break through key support or resistance levels. When the price breaks through the highest price of the previous trading day, it indicates a bullish signal; when the price breaks below the lowest price of the previous trading day, it indicates a bearish signal.

By combining the signals of the above two strategies, open positions when both signals are consistent, otherwise clear positions. A reverse opening mode is also set to stop loss and reverse trade in a timely manner when the market changes, so as to achieve a cyclic operation of funds.

Advantage Analysis

This dual-factor cycle trading strategy has the following advantages:

-

The multi-factor design ensures high signal reliability. The 123 reversal strategy and the support/resistance strategy verify each other and can reduce erroneous signals.

-

The cycling mechanism enables the strategy to adapt to market changes and effectively control one-sided losses.

-

The use of the 9-day Stochastics indicator can filter out market noise and make clearer signals.

-

It is less risky than single-factor strategies and has smaller drawdowns. Multiple factors can form a combined force to curb the impact of irrational fluctuations on the strategy.

Risk Analysis

This strategy also poses some risks:

-

It is difficult to capture trends well in sideways markets, and frequent stop losses and reverse openings will increase transaction costs. Appropiate expansion of stop loss lines can address this.

-

The parameter settings of Stochastics will affect signal quality. Improper parameters may lead to signal misplacement and quality degradation. Parameters need to be repeatedly tested and optimized.

-

Although dual-factor design improves signal quality, it also increases the impact of market "noise" on the strategy. This requires us to be more cautious when constructing and verifying strategies.

Optimization Directions

We can further optimize this strategy from the following aspects:

-

Test Stochastics of different cycle lengths to find the optimal parameter combination to eliminate market noise

-

Add a trend filter to filter out sideways markets and only open positions in clear trends

-

Optimize the stop loss line setting algorithm to reduce transaction costs while ensuring effective stop loss

-

Test different combinations of factors to find factor combinations with clearer trading signals and more stable strategies

Summary

Through dual-factor design, this strategy has obtained higher signal quality and risk-adjusted returns. At the same time, the use of cycle trading effectively controls the losses in unilateral market. The strategy has struck a good balance between risk and return. More in-depth research is still needed on parameter optimization, risk control settings, etc. to achieve better strategy performance.

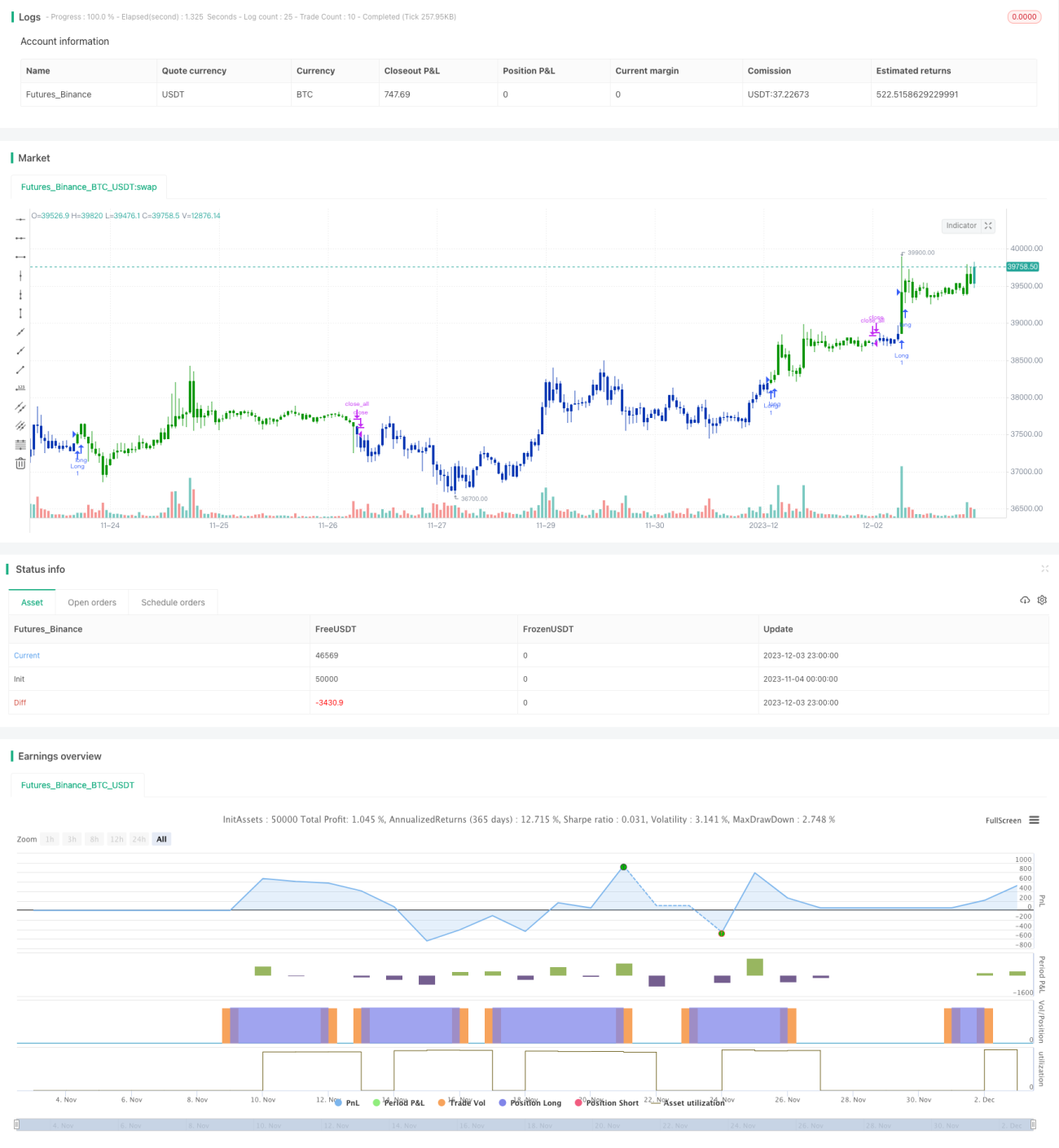

/*backtest

start: 2023-11-04 00:00:00

end: 2023-12-04 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 13/11/2019

// This is combo strategies for get a cumulative signal. - 1