OBV指標に基づくピラミッド戦略

概要

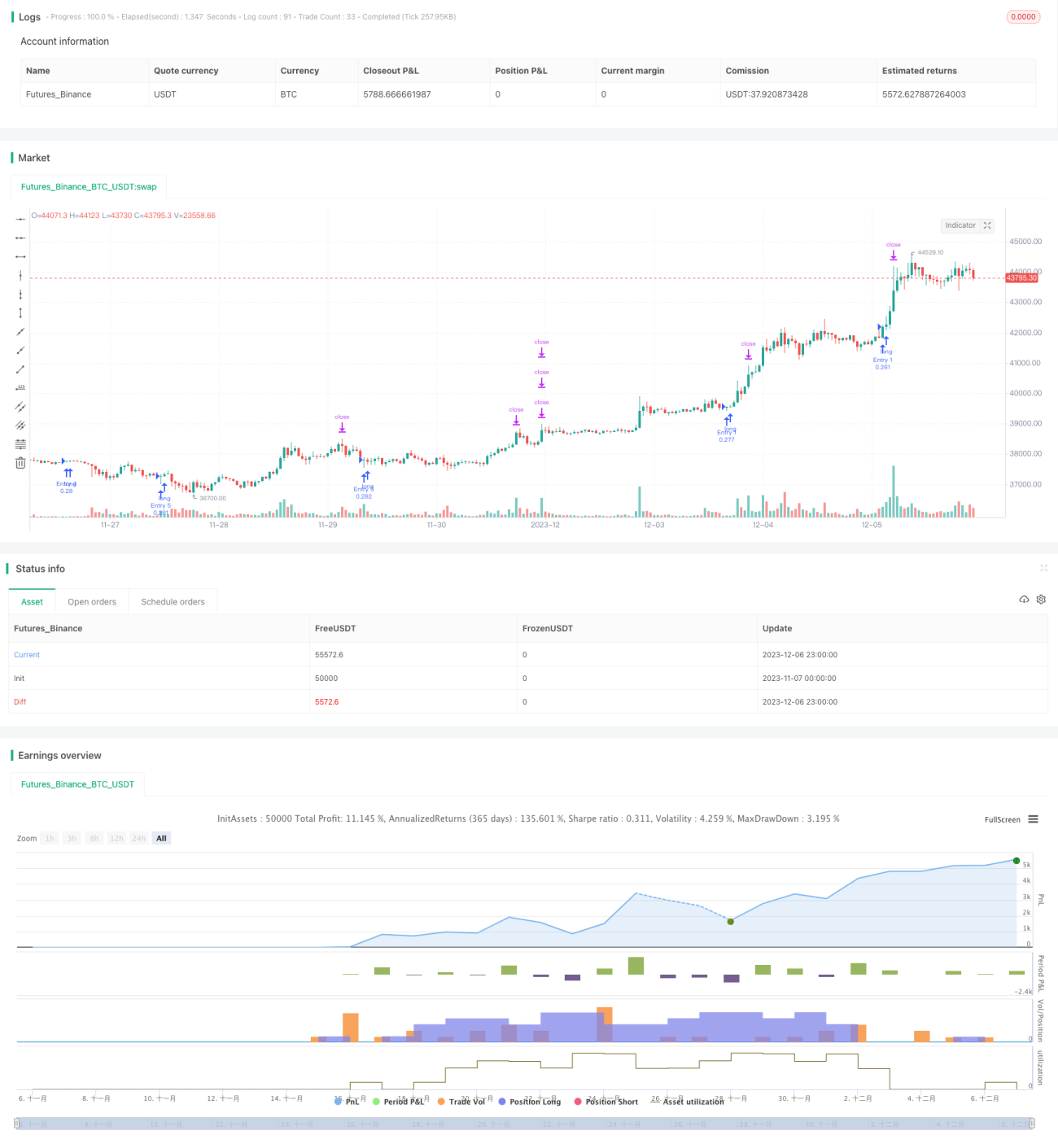

この戦略は「OBVピラミッド」と呼ばれ、OBV指標に基づいてポジションを構築し、ピラミッド型の追加手法を採用しています。トレンドが発生した後、複数回に分けてポジションを追加し、トレンドに追随して利益を獲得します。

戦略の原理

本戦略ではOBV指標を使用してトレンドの方向性を判断します。OBV指標は出来高の変化に基づいて価格トレンドを判断し、出来高の変化は市場参加者の態度を反映します。OBVが0軸を上抜けると買い圧力が強まり、上昇トレンドが形成されたことを示します。OBVが0軸を下抜けると売り圧力が強まり、下降トレンドが形成されたことを示します。

本戦略では、OBVが0軸を上抜けるかどうかを判断することで、上昇トレンドの形成を確認します。上昇トレンドが形成された場合、ピラミッド型の追加ルールを設定し、最大7回までポジションを追加できます。トレンドに追随して利益を獲得し、利益確定・損切りの仕組みを設定します。

優位性分析

本戦略の最大の優位性は、トレンドを捉えられる点です。ピラミッド型の追加方法でトレンドに追随することで、大きな利益を得る可能性があります。また、リスク管理も適切で、利益確定・損切りが設定されています。

具体的な優位性は以下の通りです:

- OBVを使用してトレンドの方向性を正確に判断できる。

- ピラミッド型の追加方法でトレンドに追随し利益を得られる。

- 利益確定・損切りの設定によりリスクをコントロールできる。

- 戦略のロジックがシンプルで分かりやすい。

リスク分析

本戦略の主なリスクは以下の2点です:

- OBVの判断ミスにより、好機を逃したり誤ったポジションを構築する可能性。

- ポジション追加が多すぎてリスクが拡大する可能性。

対応策:

- OBVのパラメータを最適化し、判断精度を確保する。

- 追加回数を適切に制御し、リスクを管理可能な範囲に保つ。

最適化の方向性

本戦略の主な最適化可能な方向性:

- OBVのパラメータ最適化により、判断精度を向上させる。

- 追加回数と金額の最適化。

- 利益確定・損切りのポイント最適化。

- 他の指標と組み合わせて判断することで、OBV単独の判断リスクを回避する。

これらを最適化することで、戦略をより安定性・コントロール性・拡張性の高いものにできる。

まとめ

本戦略は全体的に非常に実用的です。OBV指標を使用してトレンドの方向性を判断し、ピラミッド型の追加でトレンドに追随します。戦略のロジックは簡潔で分かりやすく、バックテストも容易です。実戦での活用価値があります。パラメータや利益確定・損切り、追加方法などをさらに深く最適化することで、戦略効果を一層向上させることができ、さらなる研究に値します。

- 1