古典的なゴールデンクロス移動平均線トレーディング戦略

概要

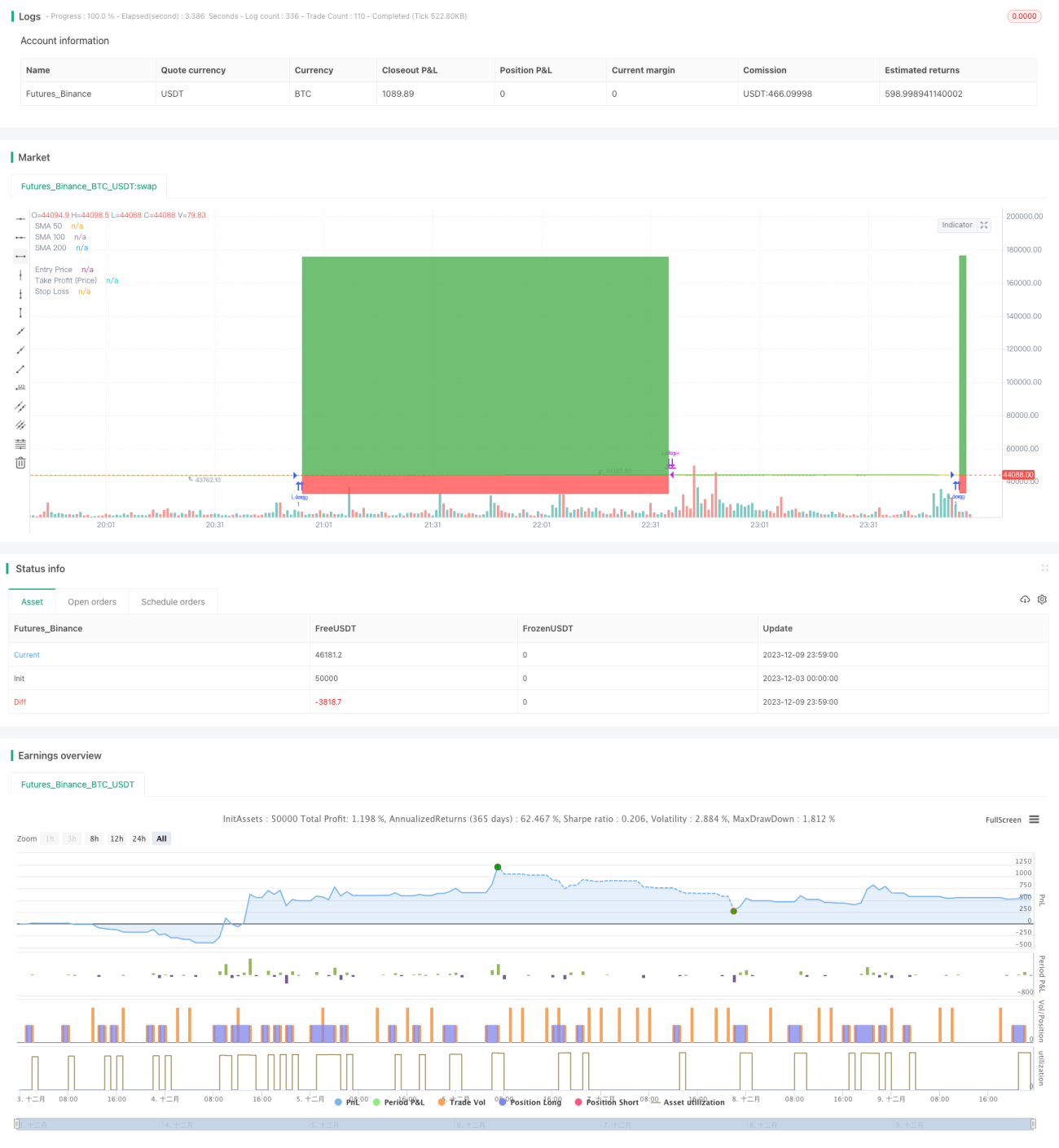

ゴールデンクロス移動平均線取引戦略(Golden Cross Moving Average Trading Strategy)は、比較的古典的な定量取引戦略です。この戦略は、異なる期間の移動平均線を用いて市場のトレンドを判断し、買いと売りを行います。短期移動平均線が長期移動平均線を上抜けた場合、買いシグナルとみなし、短期移動平均線が長期移動平均線を下抜けた場合、売りシグナルとみなします。

戦略の原理

本戦略は、3つの異なる期間の単純移動平均線(SMA):50日線、100日線、200日線に基づいています。具体的な取引ロジックは以下の通りです。

-

エントリーシグナル:50日移動平均線が100日移動平均線を上抜けた場合、買いでエントリーします。

-

エグジットシグナル:50日移動平均線が100日移動平均線を下抜けた場合、ポジションをクローズします。または、終値が100日移動平均線を下回った場合、あるいは100日移動平均線が200日移動平均線を下抜けた場合にもクローズします。

-

損切り・利確:トレーリングストップと固定ストップロスを設定します。

本戦略は、移動平均線が市場の平均価格を効果的に判断できる特性を活用しています。短期平均線が長期平均線を上抜けると、市場が上昇トレンドに入ったシグナルとみなして買いを行い、短期平均線が長期平均線を下抜けると市場が下降トレンドに入ったとみなしてポジションをクローズします。この方法により、市場のトレンドを効果的に捉えることができます。

戦略の利点

-

操作が簡単で、実装が容易です。異なる期間の3本の移動平均線を使用するだけで戦略ロジックを構築できます。

-

安定性が高いです。移動平均線自体にノイズ除去機能があり、市場のランダムな変動が取引に与える影響を効果的に除去するため、シグナルがより安定し信頼性が高まります。

-

大きなトレンドを捉えやすいです。移動平均線は市場の平均価格の変化トレンドを効果的に反映し、長期・短期線のクロスにより大きな相場変動を判断できます。

-

カスタマイズ性が高いです。移動平均線の期間の組み合わせを自由に設定でき、異なるレベルのリスク管理を実現できます。

戦略のリスク

-

多くの偽のシグナルが発生する可能性があります。短期と長期の移動平均線が非常に接近している場合、頻繁にクロスが発生し、多くの無効なシグナルが生じる可能性があります。

-

突発的なイベントに迅速に対応できません。移動平均線は価格変動に対する反応が遅いため、市場における突発的なニュースや重要イベントにリアルタイムで対応できません。

-

小規模な値動きで利益を得ることはできません。移動平均線のノイズ除去特性により、市場の小規模な変動を捉えて利益を得ることができません。

-

パラメータ設定が主観的です。移動平均線の期間の選択はやや主観的であり、市場ごとに最適なパラメータを決定する必要があります。

戦略の最適化方向

-

フィルター条件を追加し、偽のシグナルの発生を抑える。例えば、価格変動範囲をフィルターとして設定し、一定幅を超える突破があった場合のみ取引シグナルを生成する。

-

他の指標と組み合わせる。例えば、ボラティリティ指標や出来高指標などと組み合わせて使用することで、シグナルの精度を向上させることができます。

-

適応型最適化モジュールを追加する。機械学習などの技術を用いて移動平均線の期間パラメータを動的に最適化し、外部市場環境の変化に適応できるようにする。

-

深層学習モデルを組み合わせる。より高度な深層学習モデルを移動平均線の代わりに使用することで、より強力な特徴抽出とモデリング能力を得る。

まとめ

ゴールデンクロス移動平均線取引戦略は、比較的典型的なトレンドフォロー戦略です。市場価格の平均的な変化トレンドを反映し、シンプルで実用的であり、初心者の学習に適しています。同時に、本戦略にはいくつかの欠点もあり、シグナルの品質向上、他のテクニカル指標との組み合わせ、適応メカニズムの導入など、複数の側面から最適化することで、より複雑な市場環境に対応できるようになります。総じて、本戦略は非常に参考になり、学習価値の高い戦略です。

- 1