Trend Trader Bands Backtest Strategy Based on Trend Trader Moving Average

Overview

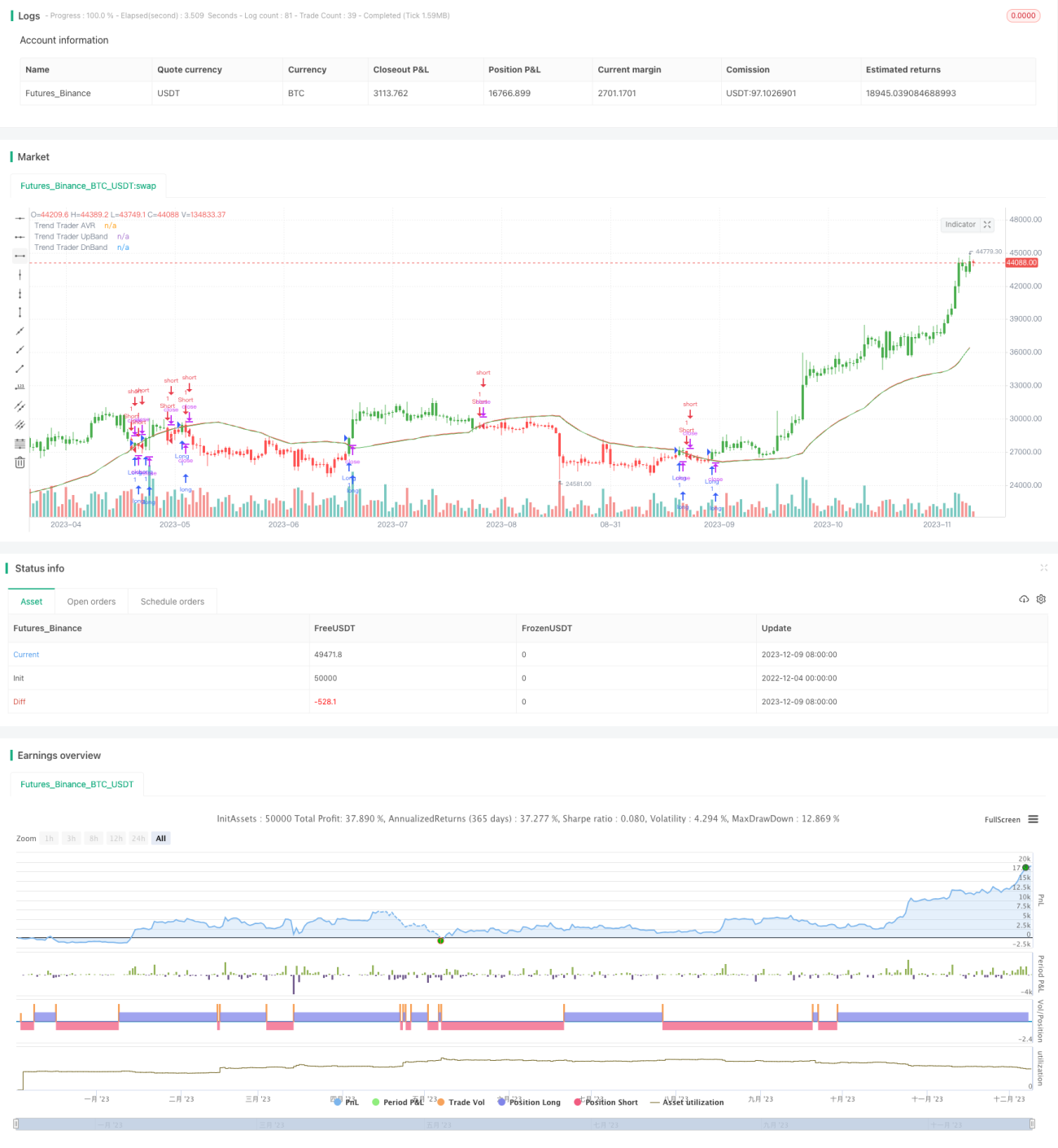

The main idea of this strategy is to judge price trends and generate trading signals using moving averages and Bollinger bands. Specifically, it first calculates the average true range (ATR) over a certain period to get volatility range, then combines highest and lowest prices to form a limiting channel. If price breaks through this channel, the close price is set to be the channel price. After that, it calculates moving average of the limited close prices, which is called Trend Trader moving average (AVR). Finally, draw Bollinger bands above and below Trend Trader moving average to form trading signals. Go long when price breaks through upper band, and go short when breaking through lower band.

Strategy Logic

The strategy first calculates ATR range and forms a limiting channel combined with highest and lowest prices. The close price will be limited to the channel price only when it breaks through the channel. After that, it calculates Trend Trader moving average of the limited close prices, which reflects mid-long term trend direction. At last, draw a upper band and a lower band parallel to the Trend Trader moving average as Bollinger bands. Breaking through upper band generates long signal and breaking through lower band generates short signal.

The core of judging trend lies in Trend Trader moving average, which embodies mid-long term trend direction. The role of Bollinger bands is to filter some false breakouts and make trading signals more reliable. The whole strategy combines trend following and breakout, forming a strong trend system.

Advantages

- ATR and price range build an adaptive channel to track market volatility

- Trend Trade AVR clearly judges mid-long term trend

- Bollinger Bands filter false breakouts and improve signal quality

- The system reflects strong trend, long holding can obtain good returns

Risks

- Long holding may suffer huge loss due to some sudden events

- Improper parameter setting may lead to over-trading, increasing transaction costs and slippage

- Performance relies heavily on parameter tuning

Solutions:

- Properly reduce holding period and set stop loss

- Optimize parameters to give signals enough buffer

- Utilize historical data and live trading for parameter tuning

Optimization Directions

- Research parameters settings on different markets and timeframes

- Test whether other indicators can filter false breakouts

- Try to incorporate stop loss to limit per trade loss

Conclusion

The strategy is overall a strong trend following system. It can judge mid-long term trend and generate trading signals combined with Bollinger bands. Through parameter optimization, it can obtain stable alpha. But risk control is also important to avoid huge losses due to some sudden events when holding for long term. Generally speaking, the strategy deserves further research and optimization for long term sustainable alpha.

/*backtest

start: 2022-12-04 00:00:00

end: 2023-12-10 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 16/10/2018

// This is plots the indicator developed by Andrew Abraham - 1