抵抗線突破環状ストップロス戦略

概要

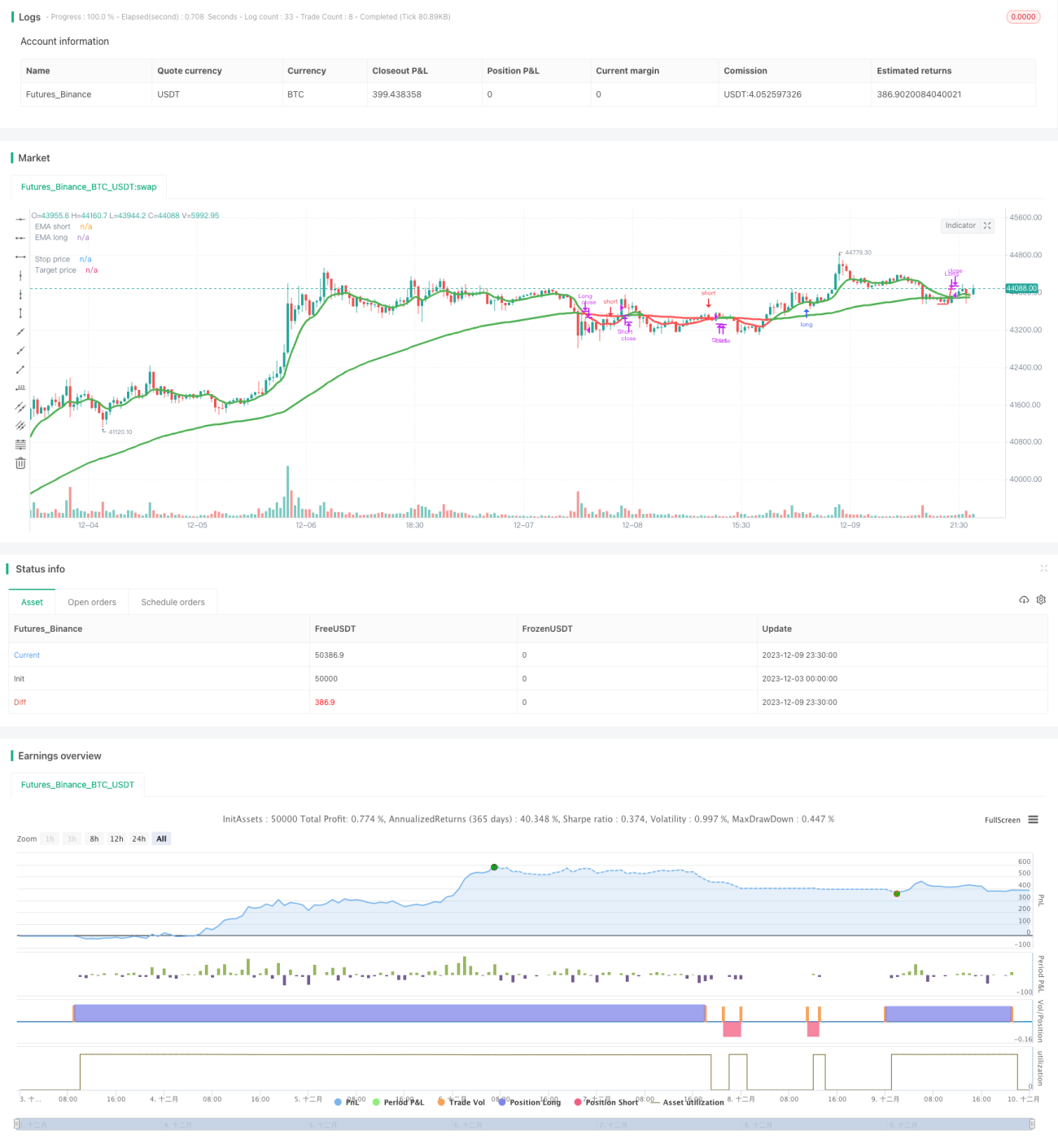

本戦略は、抵抗線突破の価格パターンシグナルと環状ストップロスのリスク管理メカニズムを活用します。抵抗線を突破した後にロングポジションを建て、支持線を突破した後にショートポジションを建てます。同時に環状ストップロスと逆指値注文を設定し、リスクを効果的に管理します。

戦略の原理

本戦略は主に以下のポイントに基づいています:

-

移動平均線を使用してトレンド方向を判断します。戦略では短期と長期の移動平均線を設定し、短期線が長期線を上抜けると長期的な上昇トレンド、下抜けると長期的な下降トレンドと見なします。

-

抵抗線突破でのロングシグナル。価格が上昇して直近の高値を突破した場合、抵抗線突破のシグナルと見なし、ロングでエントリーします。

-

支持線突破でのショートシグナル。価格が下落して直近の安値を突破した場合、支持線突破のシグナルと見なし、ショートでエントリーします。

-

環状ストップロスの設定。エントリー後に損切りラインを設定し、価格変動に応じて調整することで、損切りラインが価格を包み込むように動作させます。

-

損切りと利確によるエグジット。損切りはリスクを効果的にコントロールし、利確は利益を確定します。

具体的には、本戦略は高値と安値の平均値を価格ソースとして使用し、短期と長期のEMAを計算してトレンド方向を判断します。短期線が長期線を上抜け、かつ抵抗線突破シグナルが発生した場合にロング、短期線が長期線を下抜け、かつ支持線突破シグナルが発生した場合にショートを行います。エントリー後は一定期間の最安値を損切りラインとし、価格上昇に伴って調整し、利確ラインを設定して利益を確定します。リスクを効果的に管理しながら、トレンド内での利益を獲得します。

優位性分析

本戦略には以下の優位性があります:

-

安定した利益。トレンドに従った取引により、指数関数的な長期トレンドで利益を得ることができます。

-

良好なリスク管理。環状ストップロスと損切りを設定することで、タイムリーに損切りしてエグジットできます。

-

正確なシグナル。抵抗線突破でのロングと支持線突破でのショートは、正確で信頼性の高いシグナルです。

-

シンプルで操作が容易。インジケーターとシグナルルールはシンプルで明確であり、パラメーター設定も複雑ではありません。

-

市場への適応性。様々な銘柄やあらゆる市場状況で機能します。

リスク分析

本戦略には注意すべきリスクもいくつか存在します:

-

ブレイクアウト失敗のリスク。抵抗線・支持線突破後にプルバックや再テストが発生し、損切りに至る可能性があります。

-

パラメーター最適化のリスク。パラメーター設定が不適切だと、シグナルが頻発したり不足したりする可能性があります。最適化プロセスは慎重に行う必要があります。

-

インジケーター無効化のリスク。特殊な市場状況では、EMAインジケーターが機能しなかったり遅延したりする可能性があります。

-

トレンド反転のリスク。ロング・ショートの方向が市場と逆行した場合、損失が拡大する可能性があります。

これらのリスクは、パラメーターの最適化、適切な幅広いストップロスの設定、シグナルに厳密に従うことなどにより、大部分をコントロールし軽減できます。

最適化の方向性

本戦略は以下の点からさらに最適化できます:

-

時間周期の最適化。移動平均線や価格パターンの時間周期パラメーターを調整し、最適な組み合わせを探します。

-

銘柄適合性の最適化。銘柄ごとの特性に応じてパラメーター設定を調整します。

-

ストップロス戦略の最適化。より安定した正確なストップロス手法(トレーリングストップ、オシレーションストップなど)を採用します。

-

利確戦略の最適化。トレーリング利確や指数関数的利確を設定し、利益を最大化します。

-

フィルター条件の追加。出来高やボラティリティなどのフィルター条件を追加し、偽のブレイクアウトを排除します。

-

エントリーシグナルの強化。追加のインジケーターやパターンをエントリーシグナルの確認として組み込みます。

まとめ

本戦略は全体的に動作がスムーズで、核となるアイデアが明確であり、高い安定性と収益力を持っています。リスク管理とインジケーターの適用も適切であり、価値のあるブレイクアウト型の定量戦略です。今後、パラメーターやモジュールの最適化により、戦略をより完成度の高いものにし、より多くの銘柄や複雑な市場環境に適応させることができます。

- 1