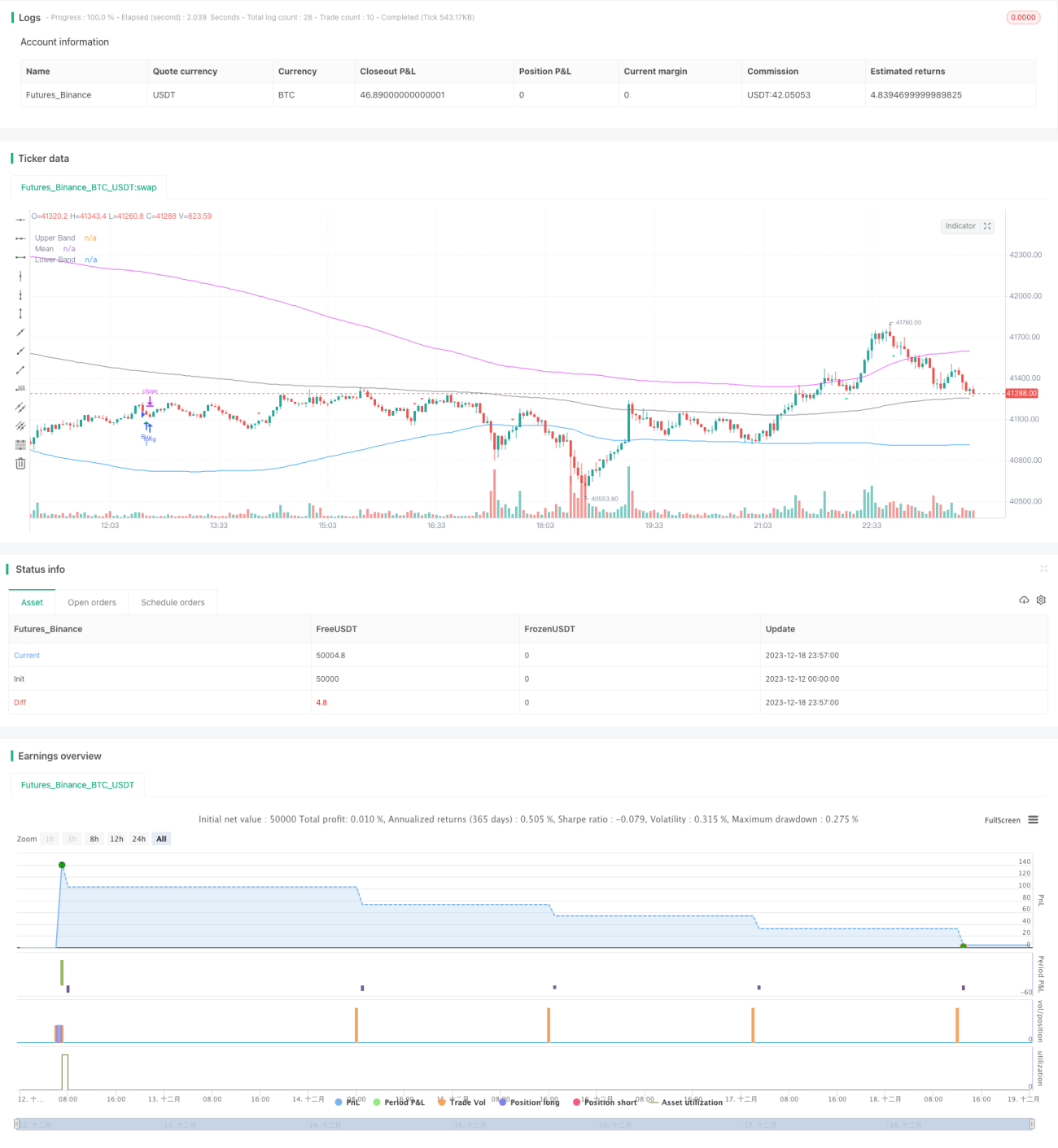

逆転平均ブレイクアウト戦略

1

Follow

1802

Followers

概要

逆転平均値ブレイクアウト戦略は、マルチファクターを組み合わせたトレンド反転戦略です。移動平均線、ボリンジャーバンド、CCI指標、RSI指標など複数のテクニカル指標を組み合わせ、価格が買われすぎ・売られすぎゾーンから反転するタイミングを捉えることを目的としています。さらに、正則ダイバージェンス分析を組み合わせることで、現在のトレンドが過去と一致しているかを検出し、偽のブレイクアウトを回避します。

戦略の原理

本戦略の核となるロジックは、価格が買われすぎ・売られすぎゾーンから反転した際に、適切な売買(ショート・ロング)を行うことです。具体的には、以下の4つの観点から反転の機会を判断します。

- CCI指標またはモメンタム指標がゴールデンクロス・デッドクロスを発し、買われすぎ・売られすぎを判断します。

- RSI指標を用いて、買われすぎ・売られすぎゾーンにあるかどうかを判断します。具体的には、RSIが65を超えると買われすぎ、35を下回ると売られすぎとします。

- ボリンジャーバンドの上限・下限ラインを利用して、価格が通常の範囲から逸脱しているかどうかを判断します。価格が再び通常ゾーンに戻る際に反転の可能性があります。

- RSI指標の正則ダイバージェンスを検出し、偽のブレイクアウトを回避します。

上記の条件が満たされた場合、戦略は逆方向のエントリーを行います。また、ストップロスを設定してリスクを管理します。

戦略の利点

本戦略の最大の利点は、複数の指標を組み合わせて反転の機会を判断するため、勝率が平均的に高いことです。具体的には以下の点が挙げられます。

- マルチファクターによる判断で信頼性が高い。単一の指標だけに依存せず、誤判定の確率を低減します。

- 反転トレードは勝率が高い。トレンド反転は比較的信頼性の高いトレード手法です。

- ダイバージェンスを検出することで、偽のブレイクアウトを追いかけることを防ぎ、システムリスクを低減します。

- ストップロスによるリスク管理により、1回の損失が過大になるのを最大限防ぎます。

リスクとその対策

本戦略には以下のようなリスクも存在します。

- 反転のタイミングを正確に判断できない。その結果、ストップロスが発動される可能性があります。ストップロス範囲を適宜拡大することで対策できます。

- ボリンジャーバンドのパラメータ設定が不適切な場合、正常な価格を異常と判断してしまう。市場のボラティリティに合わせてパラメータを設定する必要があります。

- 取引回数が多くなる可能性がある。CCIなどの判断パラメータ範囲を適宜拡大し、取引頻度を減らします。

- ロングとショートのバランスに大きな差が生じる可能性がある。過去のデータに基づいて指標パラメータが妥当かどうかを判断する必要があります。

最適化の方向性

本戦略は以下の方向から最適化が可能です。

- 機械学習アルゴリズムを利用して、指標パラメータを自動最適化する。人間の経験による誤差を回避できます。

- 頁岩指標や振幅指標などを追加し、買われすぎ・売られすぎの強度を判断する。

- 出来高指標(取引量、建玉など)を追加し、反転の信頼性を判断する。

- ブロックチェーンデータを組み合わせて市場のセンチメントを判断し、戦略の適応性を高める。

- 適応型ストップロス機構を導入する。市場のボラティリティ変化に応じてストップロス水準を調整します。

まとめ

逆転平均値ブレイクアウト戦略は、複数の指標を総合的に活用して反転の機会を判断します。リスクを制御した上で、勝率が比較的高い戦略です。本戦略は実用性が高く、さらなる最適化の余地もあります。適切にパラメータ設定を行えば、理想的な結果を得られる可能性があります。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1