モメンタムキャプチャチャネル戦略

1

Follow

1802

Followers

概要

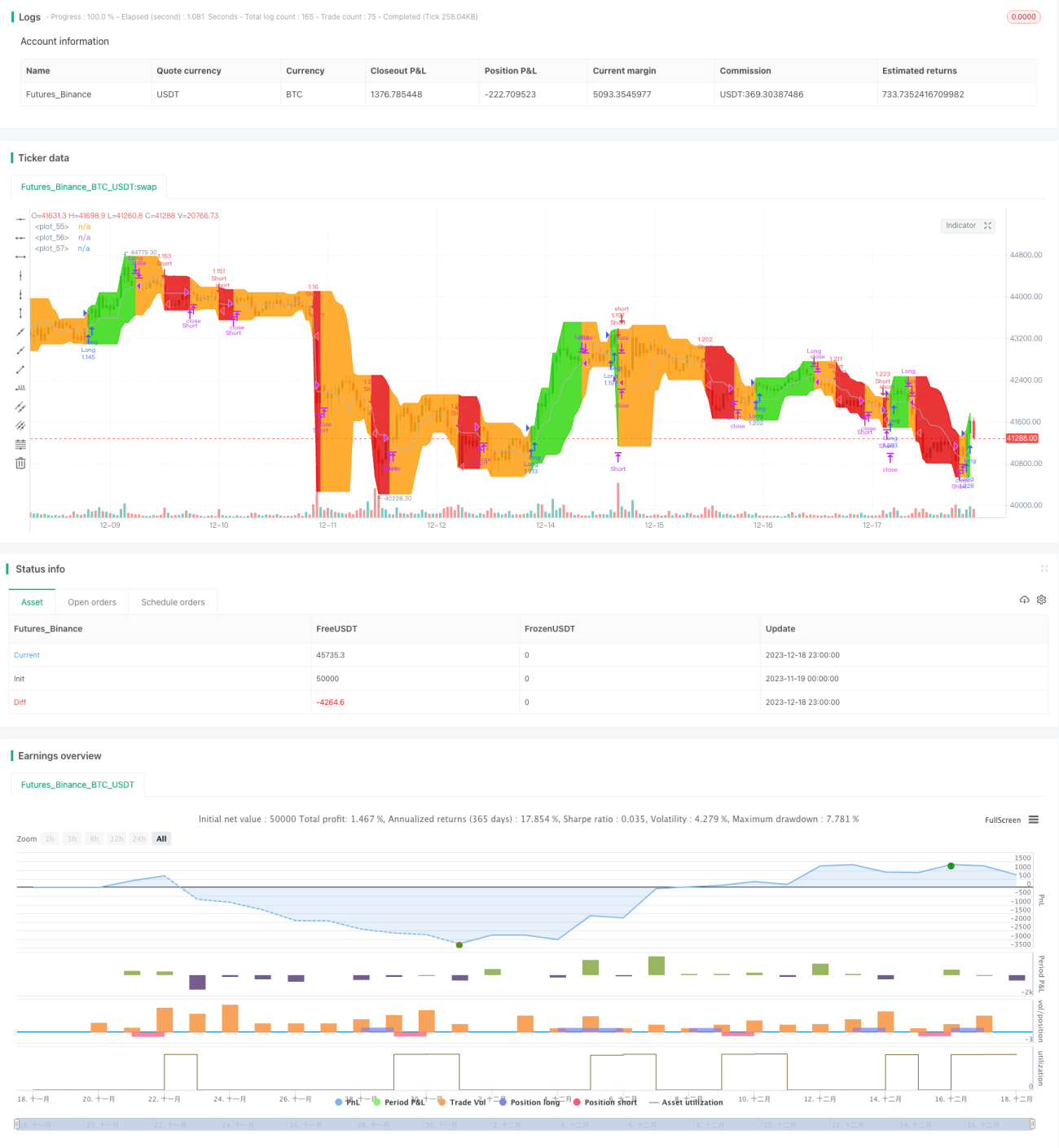

モメンタムキャプチャーチャネル戦略は、ドンチャンチャネルのバリエーションです。最高値帯、最安値帯、およびそれらの平均値であるベースラインで構成されます。この戦略は、トレンド性の高い銘柄の週足や日足の時間足で有効です。これはQuantCTアプリケーションで使用されている実装です。

操作モードは、ロング・ショート両方向またはロングのみに設定できます。

また、固定ストップロスを設定するか、それを無視して、戦略がエントリーとイグジットシグナルのみに従って動作するようにすることも可能です。

戦略の原理

この戦略の核となるロジックは、ドンチャンチャネル指標に基づいています。ドンチャンチャネルは、20日間の最高値、最安値、終値の平均で構成されます。価格がチャネルの上限・下限を突破することで、トレンド方向と反転の可能性を判断します。

本戦略はドンチャンチャネルのバリエーションです。最高値帯、最安値帯、およびそれらの平均値であるベースラインで構成されます。具体的なロジックは以下の通りです。

- 一定期間の最高値と最安値を計算し、チャネルの上限・下限とする

- 上限と下限の平均値をベースラインとして計算

- 価格が上限を突破した場合、買い

- 価格がベースラインを下回った場合、買いポジションを決済

- 価格が下限を下回った場合、売り(空売りが許可されている場合)

- 価格がベースラインを再び上回った場合、売りポジションを決済

この戦略の強みは、価格のトレンドモメンタムを効果的に捉えられる点です。価格が上限・下限を突破するのを待って真のトレンド開始を判断することで、偽のブレイクアウトによる不必要な損失を回避できます。

優位性の分析

- 価格トレンドのモメンタムを捉え、利益成長を実現

- 偽のブレイクアウトによる損失を回避し、不必要な損失を削減

- パラメータを柔軟に調整可能で、様々な銘柄に対応

- ロングのみまたは全方向の操作を選択でき、様々なニーズに対応

- ストップロスメカニズムを統合し、1回あたりの損失を効果的に抑制

リスク分析

- トレンドを捉える一方で、ブレイクアウト失敗時の損失も拡大する可能性がある

- ストップロスの設定が緩すぎると、1回の損失が拡大する恐れがある

- パラメータの設定が不適切だと頻繁な取引を招き、取引コストが増加する

- ブレイクアウトシグナルの判断に一定の遅延があり、最適なエントリーポイントを逃す可能性がある

解決方法:

- ストップロス比率は慎重に選択し、損失を抑制しつつトレンドに十分な余地を与える

- パラメータの期間を大きくし、取引頻度を低下させる

- 他の指標と組み合わせてトレンドシグナルの信頼性を判断し、より良いエントリータイミングを選ぶ

最適化の方向性

- 他の指標を統合してエントリータイミングを判断

- ストップロスの位置を動的に調整

- 銘柄特性に応じてパラメータ設定を最適化

- 機械学習を組み合わせてブレイクアウトの成功率を判断

- ポジション管理ロジックを追加

まとめ

モメンタムキャプチャーチャネル戦略は、価格トレンドを捉えることで魅力的な利益機会を提供します。同時に、一定のリスクも伴うため、適切なパラメータ調整によるリスク管理が必要です。エントリータイミングの選択とストップロスロジックを継続的に最適化することで、この戦略は非常に優れたトレンドフォローシステムになります。シンプルな取引ルールと明確なシグナル判断により、理解と実装が容易で、初心者のトレーダーにも適しています。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1